Yves here. It is unusual for the Federal Reserve or other central banks to closely monitor potential asset bubbles, as these bubbles often appear to enhance wealth for investors and onlookers until they eventually burst. In 2007, we referenced an insightful op-ed in the Sydney Morning Herald from former Reserve Bank of Australia governor Ian Macfarlane that delved into this topic. Key excerpts include:

The foremost challenge begins with acknowledging that, as an economy matures, its financial sector tends to expand at a significantly faster rate than its real economy. Consequently, economic outcomes increasingly hinge on fluctuations in asset markets rather than real sector activities, such as those in goods and labor markets. Should a considerable financial shock—notably a significant decline in share or property prices—occur, its impact on the economy would likely be more pronounced than before.

The central inquiry revolves around the future frequency of booms and busts in asset markets.

If the likelihood of asset price volatility is expected to be at least as prevalent as in the preceding two decades—and if such fluctuations are predicted to have a greater economic impact—what measures can be taken by monetary policy?

In light of the absence of protective measures offered by low inflation, what should a central bank do if it detects that an unsustainable asset price boom, particularly one financed by debt, is taking shape?

Many have pointed out that identifying a bubble in its infancy is challenging. This holds true; however, even when recognizing an emerging bubble, it remains exceedingly difficult for a central bank to respond effectively for two main reasons.

Firstly, monetary policy is a blunt instrument. Raising interest rates to combat price surges in one sector—like housing—affects the entire economy. Initially, if confidence remains high in the sector experiencing the boom, it may not be significantly impacted by increased rates, while the rest of the economy could suffer.

Secondly, there is a more critical issue regarding the central bank’s mandate. There is a prevailing consensus that central banks should aim to prevent a resurgence in inflation; however, they do not appear to have been entrusted with the responsibility of curbing substantial asset price increases, which many view as a sign of increased societal wealth. Thus, should they attempt to take on this additional role, convincing the public of its necessity would prove to be a formidable challenge.

Even if a central bank confidently identifies a destabilizing bubble and anticipates that its collapse could have severe repercussions, the public may not recognize this threat; they might only comprehend it after the situation has fully unfolded. If the central bank opts to raise interest rates, it risks being accused of inciting a recession to avert a concern that the public does not share. In a best-case scenario, if the bank raises rates modestly and curbs the bubble before it endangers the economy, it’s unlikely to receive any credit; the situation would more likely be labeled a failure in monetary policy since the potential negative outcomes cannot be observed.

Therefore, Wolf’s choice of the term “fret” is indeed appropriate. Currently, a significant proportion of lending occurs outside traditional banks, making it challenging for regulators to implement credit controls or to signal heightened scrutiny on lending within specific sectors.

By Wolf Richter, editor at Wolf Street. Originally published at Wolf Street

In the recent Federal Open Market Committee (FOMC) meeting held on June 16-17, “AI” was mentioned 21 times in the minutes released today—an increase from 8 mentions in the previous FOMC meeting in April. These references appeared in various forms:

- “AI buildout” (4 times) and “AI infrastructure” (2 times)

- “AI-related investments” (3 times), “AI business investment,” “AI investment,” “AI-related capital spending,” “AI-related expenditures”

- “AI adoption” (2 times)

- “AI implications for corporate profitability”

- “AI-related price pressures”

- “AI-related demand”

- “Optimism about AI.”

Additionally:

Some participants expressed concerns that AI could eventually influence employment prospects for certain job categories.

Strong corporate earnings along with ongoing investor enthusiasm for AI have contributed to increases in foreign equity prices.

The mania surrounding AI investments is currently a prominent driver of demand, leading to increased consumer prices across various sectors, including electricity and technology products. This phenomenon is unfolding right now.

However, the anticipated productivity gains and deflationary effects from AI are viewed as uncertain and more of a future promise:

Some participants noted that productivity advancements linked to AI adoption would, over time, lower production costs and boost overall supply, likely applying downward pressure on inflation—albeit this effect may take considerable time to manifest.

Moreover:

Certain participants suggested that these AI investments would probably enhance productivity growth and potential output in the coming years. Yet, they acknowledged significant uncertainties concerning both the timing and extent of any potential productivity gains, which were anticipated to lag behind the immediate effects of AI adoption on demand.

In contrast, the other two central concerns for the Fed—“energy” stemming from the conflict in Iran and “tariffs”—were referred to 13 and 7 times, respectively, in the minutes.

“Electricity” was mentioned once, specifically regarding how AI is exacerbating electricity prices alongside tech product costs, thereby elevating inflation:

Many participants observed that sustained demand for AI infrastructure would likely keep upward pressure on prices for technological products and electricity.

Furthermore, here are some additional mentions:

Many participants pointed out that the ongoing robust demand for AI infrastructure would likely maintain upward pressure on prices for technology products and electricity.

Nonetheless, most participants also highlighted scenarios whereby, in light of stable labor market conditions, inflation would continue to remain elevated due to heightened AI-related demand, the Middle East conflict, or the implications of tariffs.

Many participants noted that economic growth exceeding potential output—partly due to strong AI business investment—could lead to more persistent inflationary trends.

Some members acknowledged that broad financial conditions were bolstering demand, pointing specifically to inflated equity prices which have been propelled by robust corporate earnings and optimism regarding AI.

Participants generally anticipate solid real GDP growth to persist throughout the year, driven by factors such as ongoing AI-related investments, household expenditures, and fiscal policies.

The fervor surrounding AI investments—encompassing hundreds of billions of dollars being allocated—has begun to permeate the economy, giving rise to demands and inflationary pressures. The Fed is now beginning to express concern over these effects.

It’s encouraging to see the Fed acknowledging the potential threat to price stability rather than dismissing these pressures arising from the AI investment frenzy, assuming they will resolve themselves while possibly fueling the next inflation wave.

Consequently, there was a noticeable shift in sentiment during the June FOMC meeting, as indicated by the minutes: discussions centered around whether to raise rates, with “a few” participants even acknowledging that “there was a case” for a hike in June.

Conversely, discussions during meetings last year and earlier this year revolved around the possibility of cutting rates, a course they followed three times last fall.

It is rare for the Fed to make a single rate hike. Typically, such an increase signifies the onset of a new hiking cycle aimed at controlling inflation.

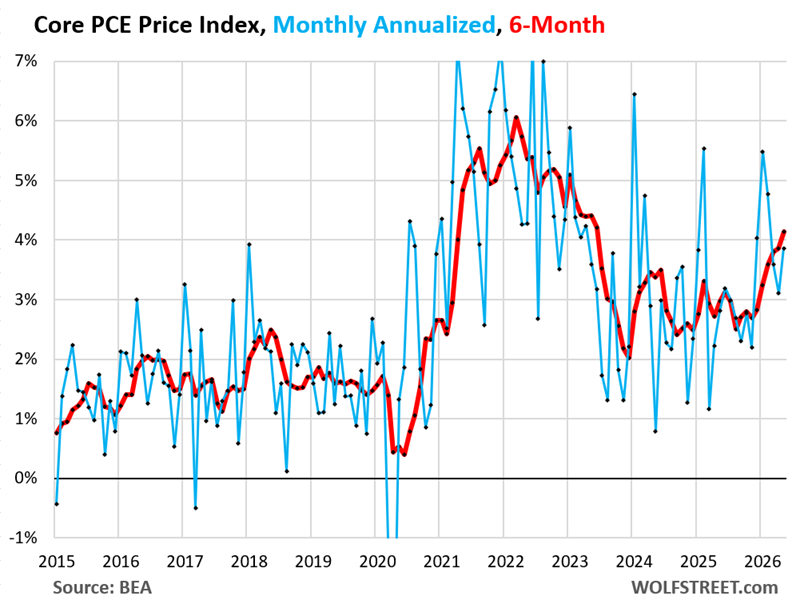

Core inflation and overall inflation metrics have exceeded the Fed’s target for over five years. The core Personal Consumption Expenditures (PCE) price index, which excludes energy and food, has been rising sharply since mid-2025, reaching 3.4% in May. The PCE price index was published two weeks following the Fed meeting, so participants only had estimates, not the actual data.

The six-month core PCE price index, indicative of current trends, rose to an annualized 4.1%, the worst figure in three years, not factoring in the surging energy prices. Major contributors include non-housing core services, electricity, and technology products.

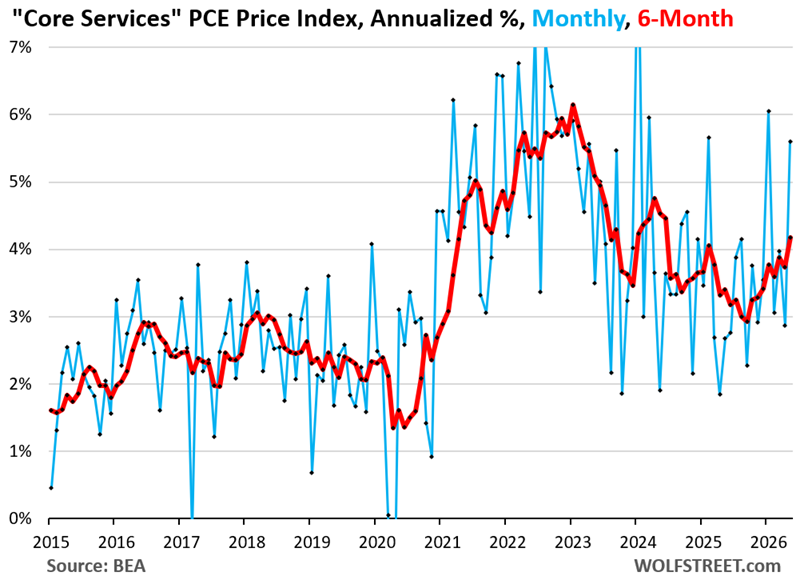

The six-month core services PCE price index, a major driver of the overall core PCE price index, has been escalating since mid-2025, reaching 4.2% in May. Core services are a primary component of consumer spending. Furthermore, if electricity prices were included in core services, the situation would appear even more dire:

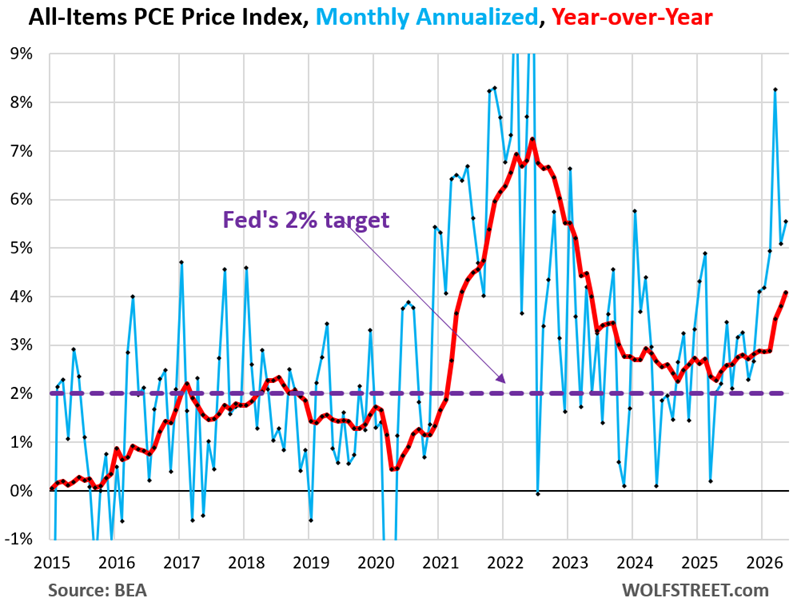

The all-items PCE price index, which the Fed’s 2% target is based on, has been above this mark since March 2020, continually surpassing the target for over five years. A growing sentiment suggests that the Fed’s effective target has shifted to a range of 3-4%, reducing 2% to mere rhetoric.

If the Fed aspires to dispel this notion, immediate action is necessary. Delaying further and ignoring this inflation would likely confirm that the Fed effectively moved its target to the 3-4% range, prompting calls for transparency about its target level while risking long-term Treasury yields and mortgage rates, which still cling to the illusion of 2%.

In case you missed it: Consumers Are Already Getting the Drift, “Inflation Expectations” Throw the Fed Another Curveball.