Greetings, readers. Today, I feel the need to address the ongoing discussions surrounding the conflict in Iran, particularly in relation to recent developments in the Strait of Hormuz. While I had initially planned to refrain from commenting, I believe some clarification is necessary concerning the U.S. stance and the broader implications of recent events.

It appears perplexing that U.S. officials are so unfazed by the ramifications of the ongoing blockage of the Strait of Hormuz. Their lack of concern seems evident in their disregard for the Memorandum of Understanding (MOU) outside of measures aimed at increasing oil supplies, even if the source is Iranian. Furthermore, the U.S. is reportedly being unyielding regarding its interpretation of the restrictions on the $6 billion in frozen Iranian assets as part of a 2023 agreement with the Biden administration. This inflexibility is coupled with increased military presence near Iran, which has been a point of contention for Iran, as highlighted in its recent complaints to Qatar, rather than mere social media speculation.

This situation led me to ponder what unseen factors might be influencing the U.S. approach. I had hypothesized that even with reduced energy flows, which are substantially lower compared to historical averages, there might still be a glimmer of hope for the U.S. in terms of oil supply. However, Philip Pilkington thoroughly counters this notion, shedding light on the disconnection between paper oil prices and real-world supply and demand dynamics. Pilkington delves into algorithmic trading and how it reacts to overly optimistic narratives from the business media—particularly calling out Bloomberg. He explains that these algorithms prioritize initial positions at the start of the week, allowing traders to manipulate markets effectively, and how this momentum-based trading impacts overall market behavior.

For those interested in a deeper dive into this topic, I highly recommend watching a segment featuring Mario Nawfal. If you prefer reading over watching videos or listening to podcasts, you can find a machine-generated transcript here.

Long-time readers may recall that we previously showcased Philip’s insights. He contributed regularly to Naked Capitalism from 2012 to 2014 before joining the esteemed fund GMO. His work often focused on critiquing flawed mainstream economic theories and the resulting misguided policies, frequently using Paul Krugman and Thomas Piketty as examples.

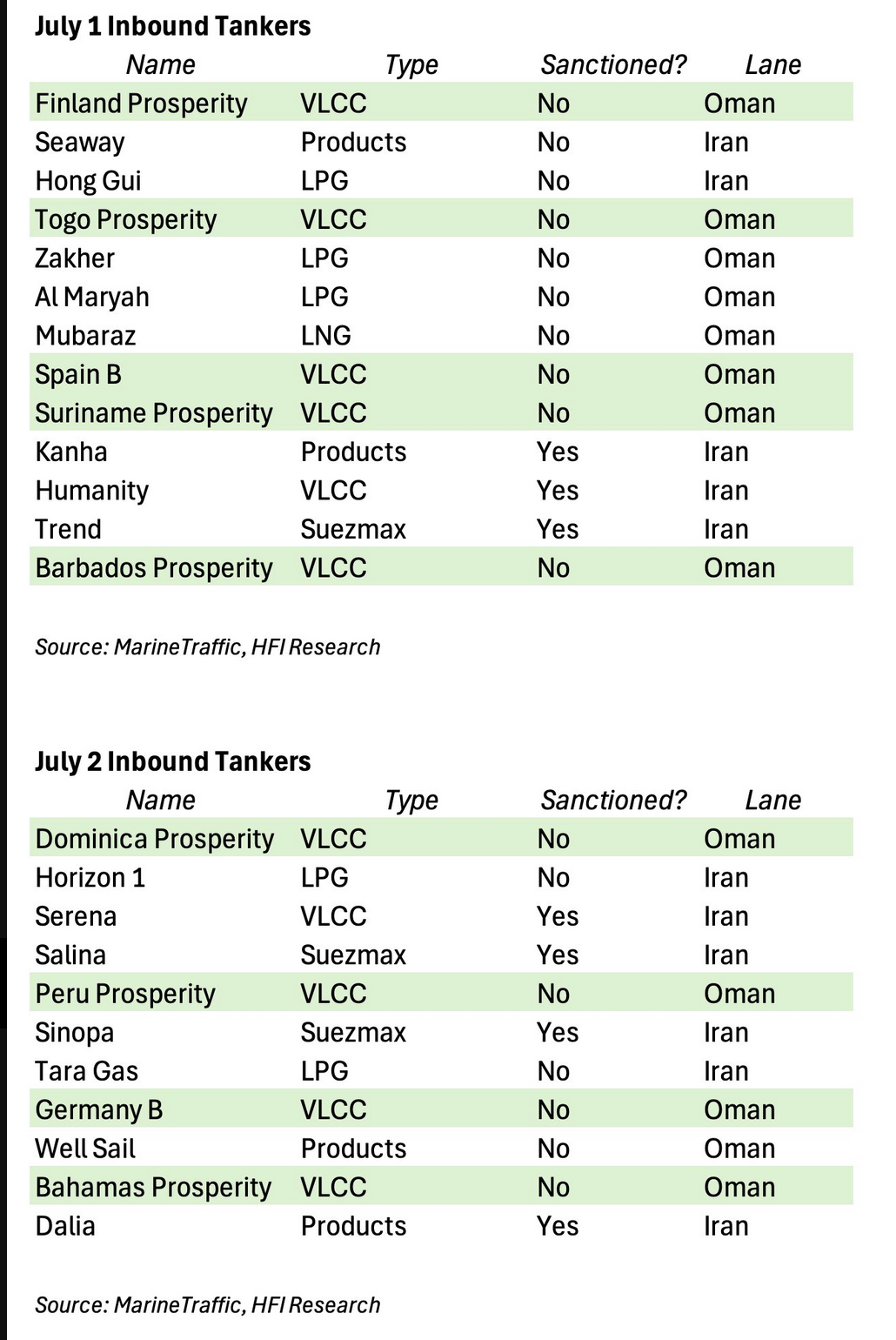

Reader DD GE recently highlighted an important post by Nate Wade that we had overlooked: Better Flows Were Clearing a Backlog, Not a Recovery. This piece directly addresses whether the influx of tankers into the Gulf for loading oil, as opposed to previously trapped full tankers, is significant enough to provide meaningful relief. Wade’s analysis indicates it is not, relying on both transit data and a realistic assessment of the current situation and forecasts. Here are some key excerpts:

The ceasefire holds, but the underlying deal has stalled on the points that determine whether reopening is sustainable.

Iran is cementing its control over the strait using mechanisms such as mines and fees that will persist beyond any ceasefire.

Iran’s institutions are experiencing internal discord; even a signed agreement may not compel the IRGC, meaning the anticipated reopening of the market is not occurring according to the MOU’s timetable.

Meanwhile, three factors are suppressing prices—released barrels previously trapped in the Gulf, strategic petroleum reserve (SPR) drawdowns, and Chinese reserves which seem to be on the decline. These sources are finite, indicating that the mispricing mentioned in the “Two Spikes Coming” article remains unresolved.

Recent evidence, including inbound tanker counts and floating storage records, corroborates the physical state of the market rather than the price trends.

However, despite Iran’s frequent assertions of its dominion over the Strait of Hormuz—with claims that Oman-side transit is increasingly unreliable—there have been significant activities on the Oman side:

The tankers are smart; they’re utilizing the funeral to navigate back via the Oman route. https://t.co/XGG0sxf1I5 pic.twitter.com/82RCvD3GSC

— HFI Research (@HFI_Research) July 3, 2026

Delving further into Wade’s analysis:

Approximately 170 million barrels of crude oil that were stuck in the Gulf have been released to the market after the MOU permitted it. The SPR is being drawn down at a rate that may allow for only three to six weeks of supplies. Since March, Chinese crude imports have decreased by around 5 million barrels per day, but their visible commercial stocks haven’t changed much, suggesting such shortages are being filled from reserves not reported in public data. Cushing has also seen a decline to 18.96 million barrels, the lowest since October 2014 and nearing the 20 million barrels traders deem necessary for operations. A partial reopening of the strait alone will not resolve these issues.

It’s worth noting that Cushing has seen a slight recovery to 19.666 million barrels; however, there are no compelling indicators that this upward trend will persist.

Another crucial aspect raised by Wade involves the $12 billion in frozen Iranian assets that Pezeshkian has claimed might have been released to Iran. As we’ve discussed extensively, this is not the case: negotiations over the aforementioned $6 billion are still ongoing and the larger issue remains unresolved.

Additionally, the U.S. has acknowledged facing some fertilizer challenges:

DECLARATION OF EMERGENCY AND AUTHORIZATION FOR TEMPORARY DUTY-FREE IMPORTATION OF PHOSPHATE FERTILIZER FROM MOROCCO https://t.co/fouqFzMcFv

— U.S. State Dept – Near Eastern Affairs (@StateDept_NEA) June 30, 2026

This emergency declaration may seem overstated, especially since it currently only concerns Morocco, but it’s not us who used the term “emergency.”

As we look towards the weekend, let’s hope for a peaceful and uneventful few days. Until next week!