In recent news, significant developments are unfolding in the financial realm:

- * The Federal Reserve is anticipated to raise interest rates during today’s policy meeting.

- * A former Fed vice chair advocates for pausing rate hikes after this week.

- * Despite the rescue of First Republic, shares of regional US banks are falling sharply.

- * House Democrats have unveiled a strategy to force a vote on raising the US debt limit.

- * Leaders from top AI firms are set to meet at the White House today.

- * The price of gold has rebounded past $2000 per ounce.

- * US factory orders showed recovery in March, driven by aircraft bookings.

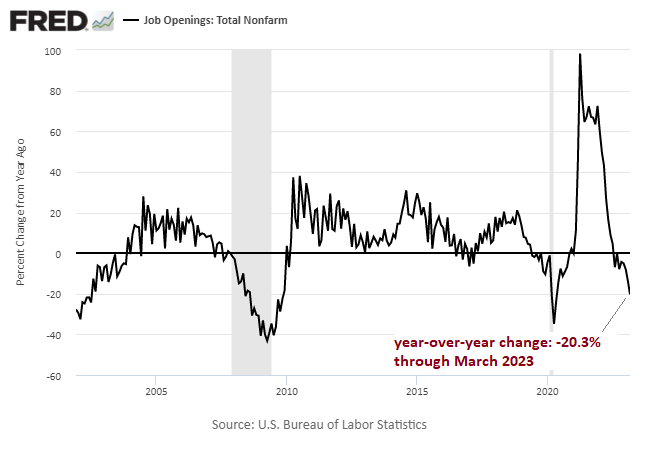

- * US job openings declined again in March, reflecting a deeper annual contraction.

In April, the anticipated long-term return for the Global Market Index (GMI) slightly decreased to a 5.9% annualized rate, marginally lower than the previous month’s estimate, which can be found here. This forecast, derived from the average estimates of three models (details below), is located near the lower end of historically realized performance over the past decade.

* US government may run out of cash by early June, according to advisors Yellen and the CBO.

- * The IMF has raised its growth forecast for Asia, attributing it to a recovery in China.

- * Eurozone manufacturing activity declined in April; marking the first drop since January.

- * Year-on-year inflation in the Eurozone has increased in April for the first time in six months.

- * Actively managed ETFs are a small sector but are rapidly expanding.

- * US construction spending rose in March, marking the first increase in four months.

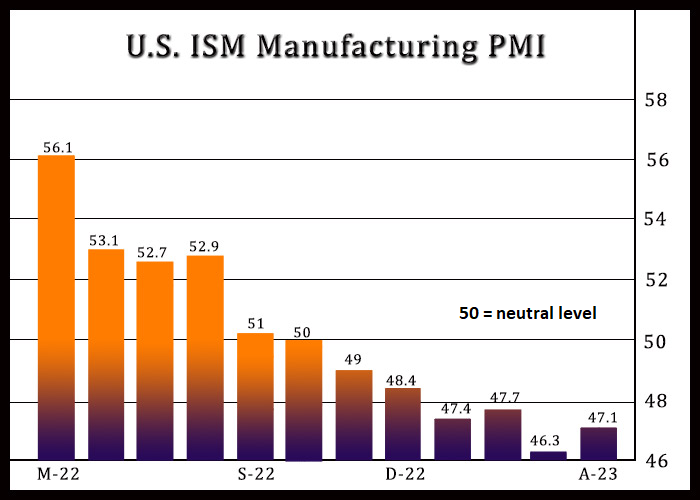

- * The US ISM Manufacturing Index slightly improved, indicating that the recession in this sector may be easing.

In April, most major asset classes staged a recovery, notably led by property shares outside the US, based on a collection of ETF proxies. However, certain sectors experienced downturns, particularly foreign government bonds in developed markets, emerging market stocks, and commodities.

* JPMorgan has acquired the defunct First Republic Bank.

- * A Federal Reserve report criticized its supervision following the collapse of Silicon Valley Bank.

- * China’s manufacturing unexpectedly contracted in April.

- * South Korea has witnessed a seventh consecutive month of falling exports in April.

- * A report predicts significant job turnover in the upcoming five years due to automation.

- * Charlie Munger has shared concerns regarding the US commercial property market.

- * US consumer spending remained flat in March, indicating a slowing economy.

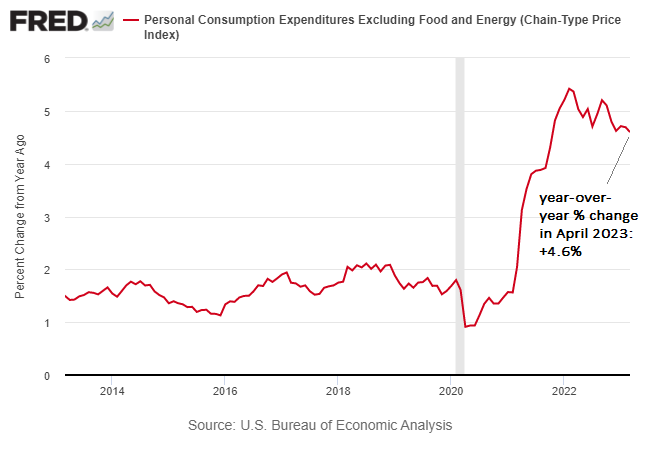

- * The Fed’s preferred inflation measure showed a slight slowdown in April, but only marginally:

● These Are the Plunderers: How Private Equity Runs―and Wrecks―America

Gretchen Morgenson and Joshua Rosner

Review via Business Insider

The authors argue that private equity firms often “acquire companies and burden them with debt while depleting their assets and profits,” only to sell them at a significant profit within a few years. However, on the surface, the concept of regularly flipping unprofitable businesses stripped of productive assets for considerable gains is difficult to believe. While there might be individual success stories, can this really serve as a viable strategy for allocating trillions of dollars in capital? It seems highly unlikely.

According to certain forecasts, the US economy grew at a significantly slower rate than anticipated in the first quarter, raising concerns about a potential recession. While it may be premature to dismiss this threat entirely in the current environment, there is also a valid argument for suggesting that the economy may continue to perform modestly despite sluggish growth.

* US officials are collaborating with private sector leaders to rescue First Republic Bank.

- * The Eurozone economy continued to stagnate in the first quarter.

- * China has increased pressure on foreign companies, presenting fresh risks for Western businesses.

- * Pending US home sales dropped in March, experiencing their first decline since November.

- * US jobless claims fell last week, remaining low despite a downturn in economic growth.

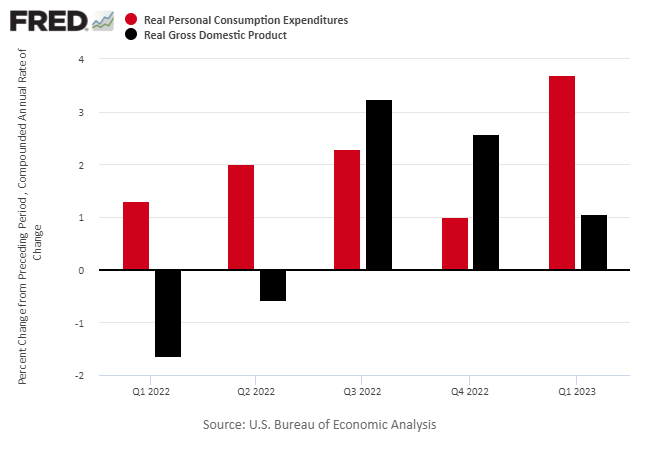

- * Economic growth in the US slowed more than expected in the first quarter, even amidst rising consumer spending:

While there are many concerns on the horizon, the year-to-date returns for key equity sectors tell a different tale. Technology and communication services are still leading the charge this year, vastly outperforming the broader stock market based on a review of ETFs up to yesterday’s close (April 26).

* House Republicans have passed a debt-ceiling and spending-cuts proposal, yet…

- * The GOP’s debt ceiling bill is likely to be dismissed in the Senate.

- * Weak tax collections indicate that the US could default on its obligations by early June.

- * The US and South Korea have announced a historic deal aimed at countering North Korea’s nuclear threat.

- * The risks associated with ‘shadow banks’ have increased after the collapse of SVB.

- * US durable goods orders have rebounded significantly, but business investment has decreased once again.

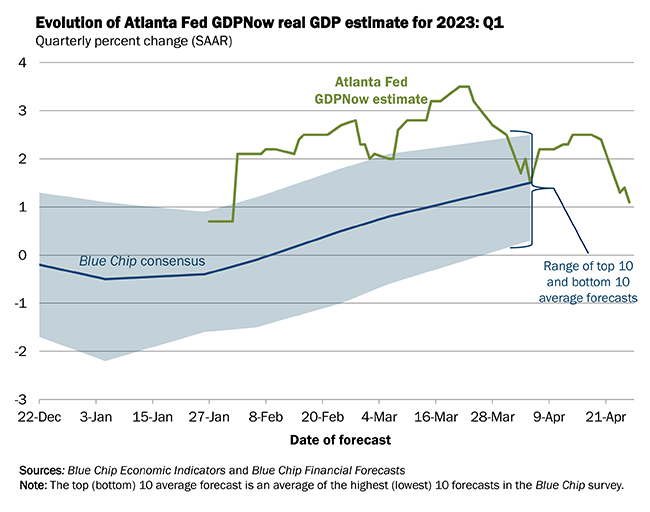

- * The Atlanta Fed’s GDPNow model has sharply reduced its Q1 growth estimate:

In this rewritten version, the content maintains its original HTML structure while enhancing clarity and flow for a better reading experience. Key updates include improved sentence structure, substitution of indirect phrases with direct ones, and overall refined language. The result is a comprehensive summary of recent economic developments and analysis, concluding notes on market conditions and forecasts.