Highlights:

- OPEC leader states that demand is “resilient” and low investment could result in sustained high oil prices.

- The United Auto Workers union has reached a tentative deal regarding a contract with Mack Trucks.

- An investor survey indicates that the US office market is facing a potential crash.

- Office attendance in major cities remains at only half of pre-pandemic levels.

- US construction spending increased for the eighth consecutive month in August.

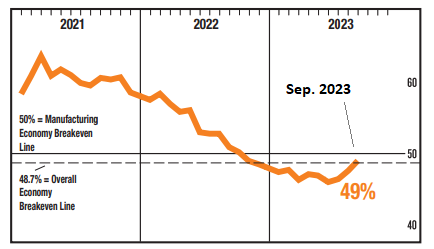

- The US ISM Manufacturing Index showed an uptick in September, nearing neutral.

In September, commodities and cash continued to lead performance among major asset classes. For the second consecutive month, widespread losses were noted elsewhere in global markets, as indicated by various ETF proxies.

Key Updates:

- The AI boom is projected to “dramatically increase” energy consumption.

- Weak demand in China and globally has led the World Bank to revise its growth outlook for Asia.

- China’s commodity demand is reported as growing robustly, according to Goldman Sachs.

- The US 10-year Treasury yield approaches a 15-year high.

- China’s factory recovery has slowed in September.

- The UAW strike has expanded to affect 17% of UAW members at the Big Three automakers.

- The Fed’s preferred inflation measure rose less than expected in August.

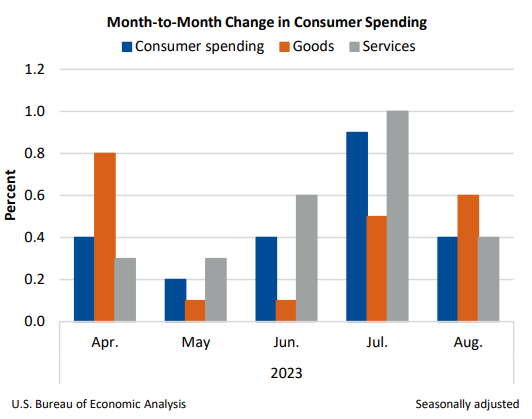

- US consumer spending has shown an increase for the fifth straight month in August.

● Blood in the Machine: The Origins of the Rebellion Against Big Tech

Brian Merchant

Review via San Francisco Chronicle

In our technology-driven age, the Luddites—19th-century British workers famed for opposing machinery that replaced their jobs—are often dismissed as outdated and anti-progress. However, Brian Merchant, a tech columnist for the Los Angeles Times, debunks this misconception in his captivating new book, “Blood in the Machine: The Origins of the Rebellion Against Big Tech.” He reveals that these machine-smashing rebels were far from ignorant; they confronted the very same challenges regarding automation and labor that we face today.

Although we may seem to be navigating the post-truth era, CapitalSpectator.com remains committed to relying on solid data rather than succumbing to an increasing trend of reframing facts for creative purposes.

Updates:

- A government shutdown is increasingly likely as the September 30 deadline approaches.

- Pending home sales in the US continued to decline in August.

- The slowdown in US housing sales is expected to persist for a “long time,” according to Redfin’s CEO .

- A significant strike among US healthcare workers is expected next week.

- Credit card data indicates US consumer spending slowed in September.

- BlackRock CEO Larry Fink predicts that the US 10-year Treasury yield will surpass 5%.

- Revised US GDP data for Q2 has remained unchanged with a growth rate of 2.1%.

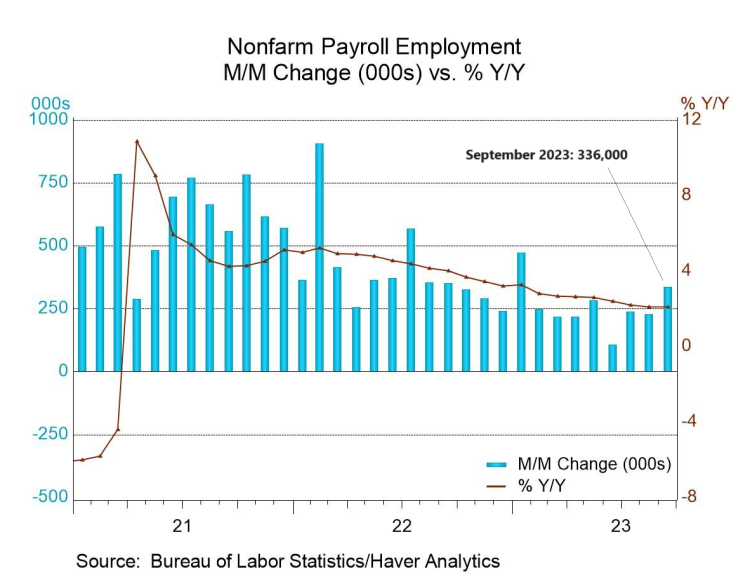

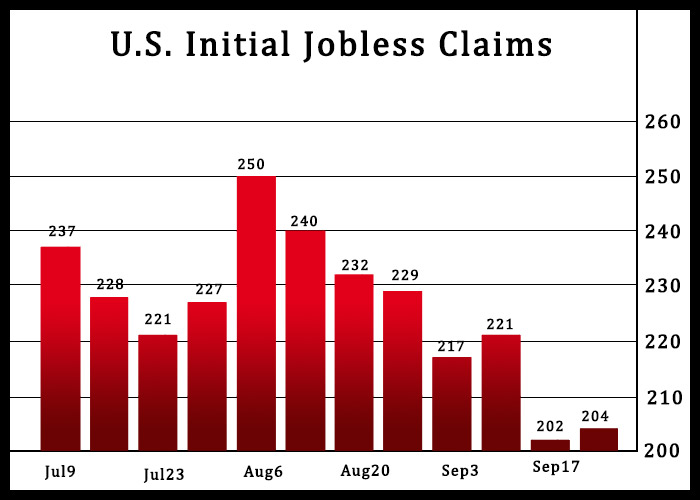

- US jobless claims remain low, indicating ongoing labor market strength.

A combination of factors may be leading to a perfect storm for the bond market, driving yields higher.

Latest Developments:

- The likelihood of a government shutdown increases as the September 30 deadline approaches.

- The workers union is threatening to escalate strikes at major Detroit automakers.

- Shares of Evergrande, a troubled Chinese property developer, have been suspended.

- Oil futures have reached their highest levels this year.

- US durable goods orders have unexpectedly risen in August.

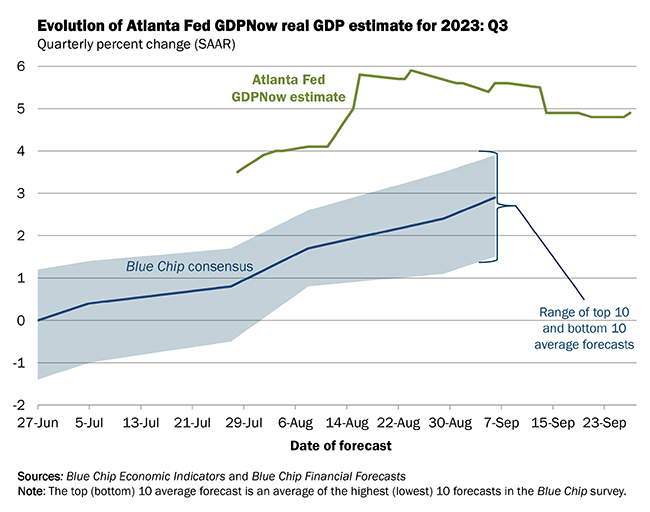

- Current estimates for Q3 US GDP continue to indicate a strong growth acceleration compared to Q2.

Earlier this month, I noted that there was still room for debate regarding whether a broad risk-off signal was in the works. Now, however, as of September 26, the opportunity for open-mindedness is diminishing, given data from several sets of ETF pairs analyzing market conditions.

Government Shutdown News:

- The Senate has passed a spending bill to prevent a government shutdown, but…

- The House may reject the Senate’s temporary bill.

- The FTC, along with 17 states, has filed an antitrust lawsuit against Amazon.

- A strong US dollar is presenting a potential headwind for stocks.

- Evergrande, China’s struggling property developer, has missed another bond payment.

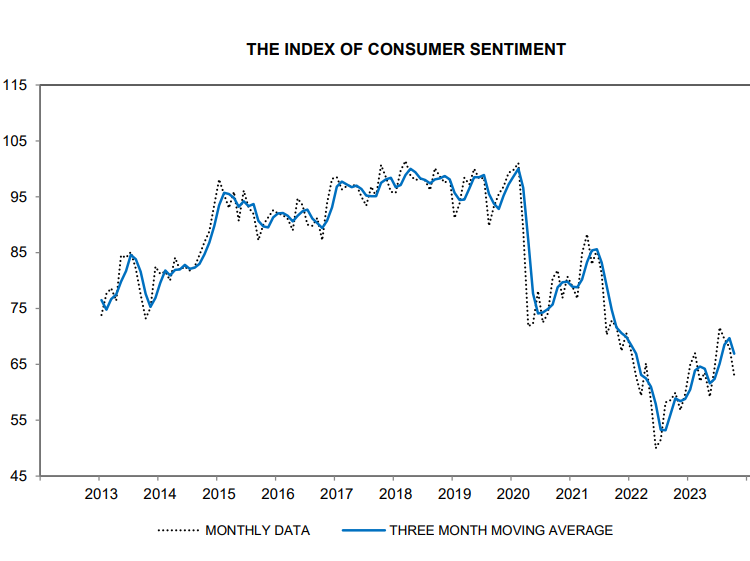

- Consumer confidence in the US has declined for the second consecutive month in September.

- New US home sales dropped in July to their lowest level since March.

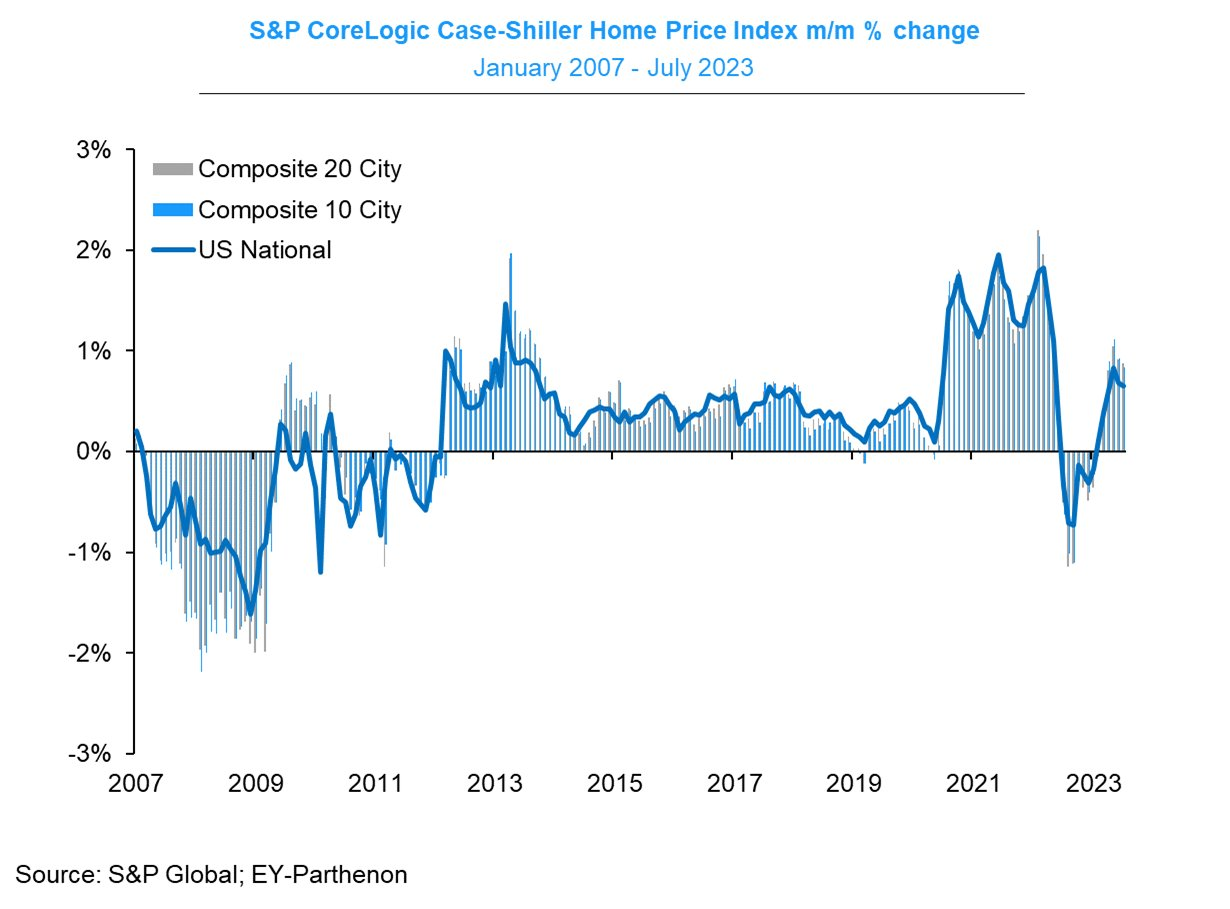

- Meanwhile, US home prices have risen for the sixth month in a row, achieving a new high in July.

In this revision, an engaging introduction sets the stage for the updates on economic indicators and market trends. Likewise, a succinct conclusion ties together the insights presented throughout the article, emphasizing the current state of the market landscape.