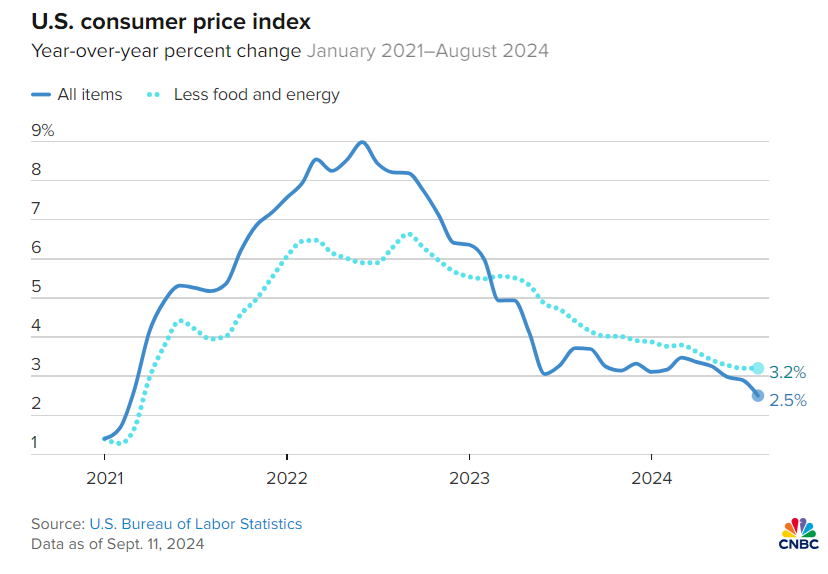

In August, US consumer price inflation slowed to a year-over-year rate of 2.5%, the lowest level in over three years. However, the core Consumer Price Index (CPI) stubbornly held at 3.2%, unchanged from the previous month. “This report isn’t what the market anticipated. With core inflation exceeding expectations, the Federal Reserve’s plan for a 50 basis point rate cut has become more complex,” comments Seema Shah, chief global strategist at Principal Asset Management. Sarah House, a senior economist at Wells Fargo, explains: “While inflation is generally decreasing, the effects of the pandemic are taking longer to fully resolve.”

Market sentiment has shifted recently towards more defensive equity sectors. This change has resulted in utility shares outperforming other sectors, making them the top performers based on various sector ETFs through the close on September 10.

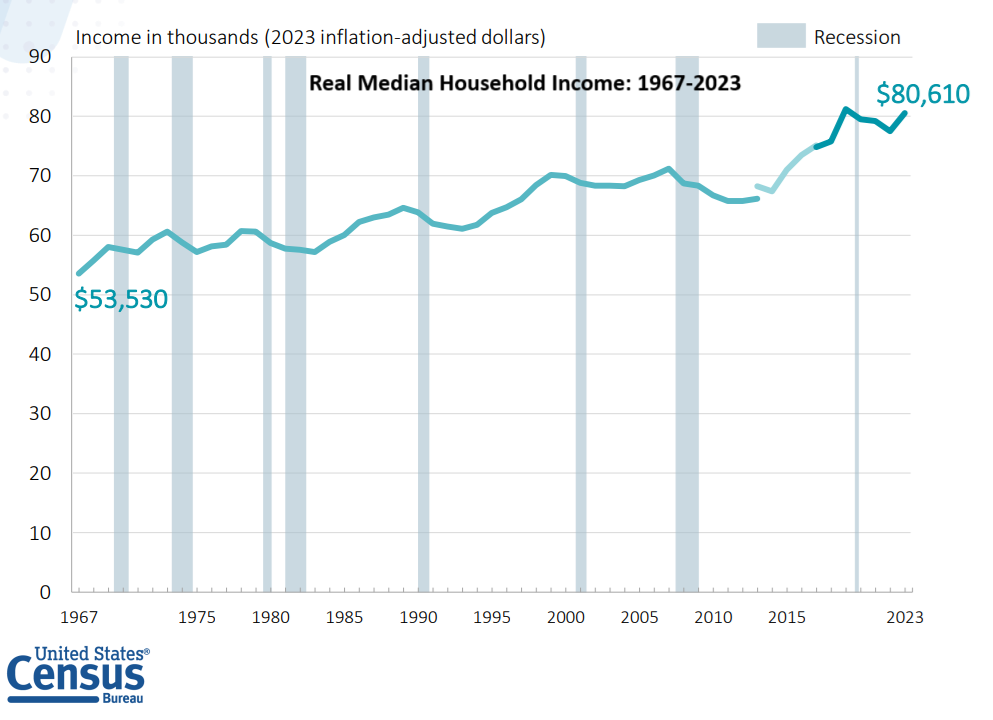

US household income saw a significant rebound in 2023, marking the first annual increase since the pandemic, according to new data released by the Census Bureau. The inflation-adjusted median household income rose by 4% to $80,610 in 2023, up from $77,540 in 2022. However, Beth Ann Bovino, chief economist at US Bank, remarks, “Many households still do not feel the improvement,” highlighting the lingering effects of the high inflation rates that peaked in 2022 but have since been declining. Despite the rise in income for 2023, the poverty rate also increased, marking a second consecutive rise due to the expiration of pandemic-related government aid. The percentage of Americans living in poverty (as defined by the Census Bureau) rose to 12.9% in the previous year from 12.4% in 2022.

Tomorrow’s report on US consumer inflation for August is not anticipated to disrupt forecasts that the Federal Reserve will lower interest rates next week; however, recent disinflation trends seem poised to stall. This projection comes from CapitalSpectator.com’s ensemble model assessing the year-over-year change in core CPI.

The risk of a US government shutdown on September 30 has become a pressing concern following House Republicans’ presentation of a spending plan that is likely to be rejected by Democrats. Even if the bill passes the House, its survival in the Democratic-controlled Senate seems bleak. Current odds of the House approving the legislation seem to be uncertain.

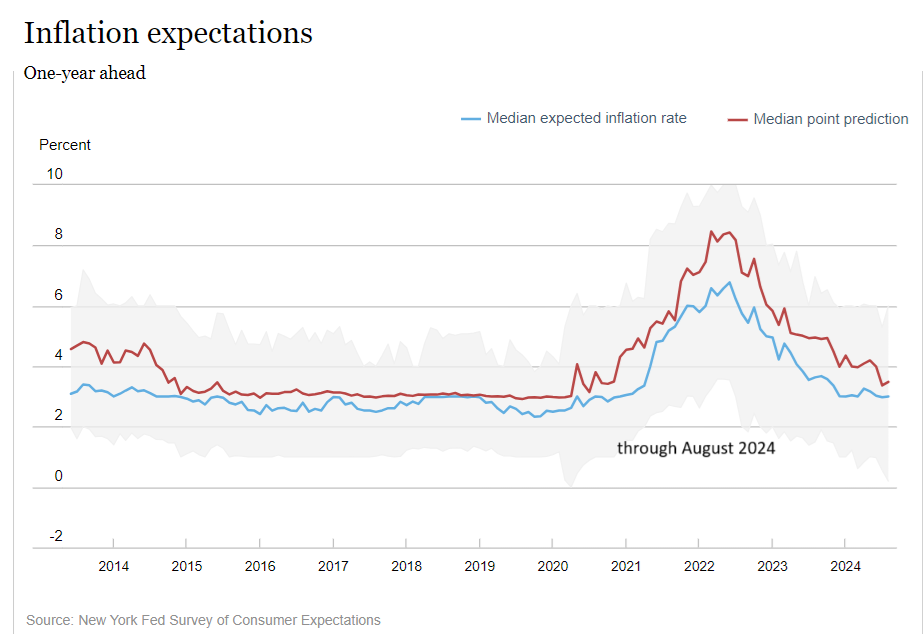

Meanwhile, consumer inflation expectations are reported to be “largely stable” in August, according to the New York Federal Reserve. The median inflation outlook for the next year remains unchanged at 3.0%, as per the latest survey conducted by the regional Fed bank.

US shares experienced their largest weekly decline in over a year last week, but this setback did not hinder US stocks from being recognized as the world’s top-performing asset class in 2024. According to a range of ETFs tracking the major asset classes as of Friday’s close (September 6), US equities continue to lead significantly.

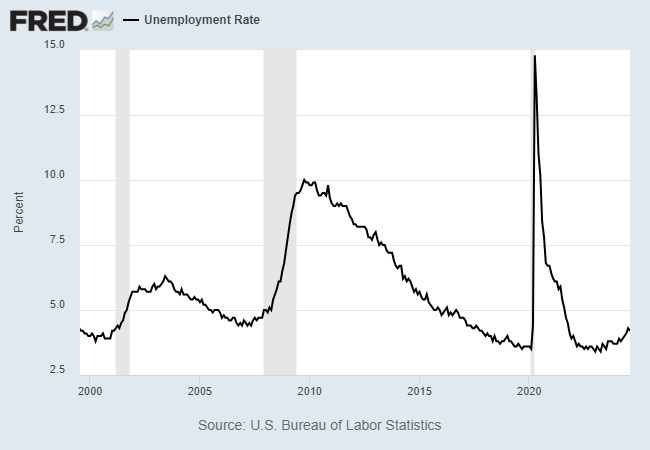

US payrolls showed a rebound in August; however, the addition of 142,000 new jobs fell short of expectations. “The labor market is gradually cooling,” states Jeffrey Roach, chief economist at LPL Financial. “While businesses are still hiring, they are doing so with more caution. The Fed is likely to implement a 25 basis point cut while leaving the option open for more aggressive measures in the last two meetings of the year.” The unemployment rate decreased slightly to 4.2% from the previous 4.3%. Although this shift is modest in historical terms, it has raised concerns about a potential recession among some analysts, who note, “The rise in the unemployment rate falls within a historical range typically associated with recessions,” says economist Claudia Sahm. “However, based on historical performances, we are not currently in a recession, though a weakening labor market is evident.”

● The Greatest of All Plagues: How Economic Inequality Shaped Political Thought from Plato to Marx

● The Greatest of All Plagues: How Economic Inequality Shaped Political Thought from Plato to Marx

David Lay Williams

Summary via publisher (Princeton U. Press)

Economic inequality remains one of the foremost challenges of our time, with public debates often questioning whether it is an inevitable result of economic systems and what can be done to address it. But why should this inequality concern us? The Greatest of All Plagues illustrates that this fundamental question has captivated some of the most notable political thinkers throughout Western intellectual history.

Semivolatility-managed portfolios

Daniel Batista da Silva (U. of Geneva) and M. Fernandes (Getulio Vargas Fund)

July 2024

Numerous studies have shown that managing volatility can enhance the risk-adjusted performance of momentum portfolios. However, its effectiveness for other factors and anomalies is less certain. This research illustrates that regulating both the upside and downside of volatility leads to more stable risk-adjusted returns across a variety of factors, anomalies, and exchange-traded funds. Particularly, the introduction of semivolatility-managed portfolios, which not only reduce leverage in times of high downside volatility but also capitalize on periods of favorable volatility, has proven successful. Our findings indicate that these semivolatility-managed portfolios surpass both standard portfolios and other existing volatility management strategies.

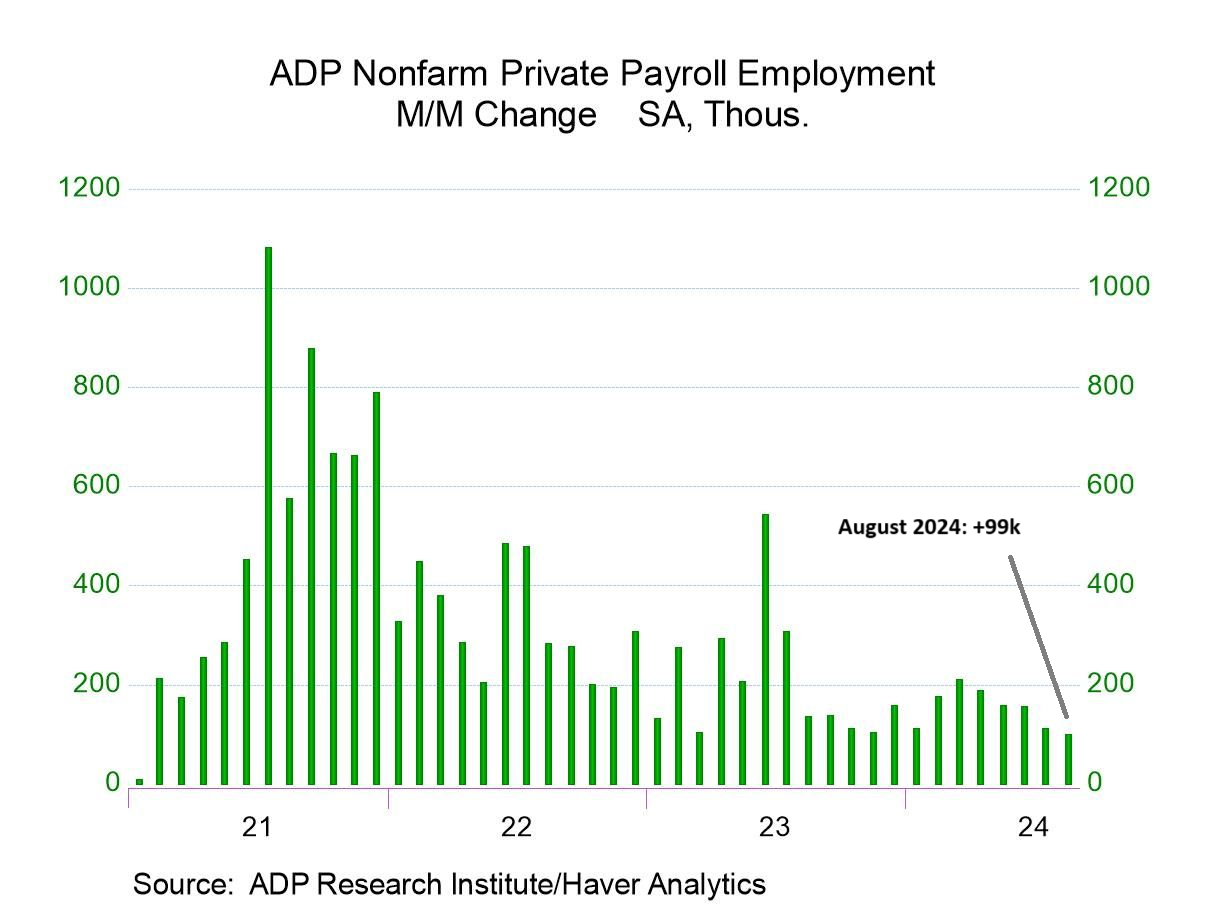

US hiring at companies slowed again in August, with a net increase of 99,000 jobs reported in the ADP Employment Report. This marks the lowest growth rate since January 2021. “The gradual decline in the job market has brought hiring down to slower-than-usual levels following two years of exceptional growth,” states Nela Richardson, chief economist at ADP. “Wage growth will be the next key indicator to monitor as it appears to be stabilizing after a significant slowdown post-pandemic.”