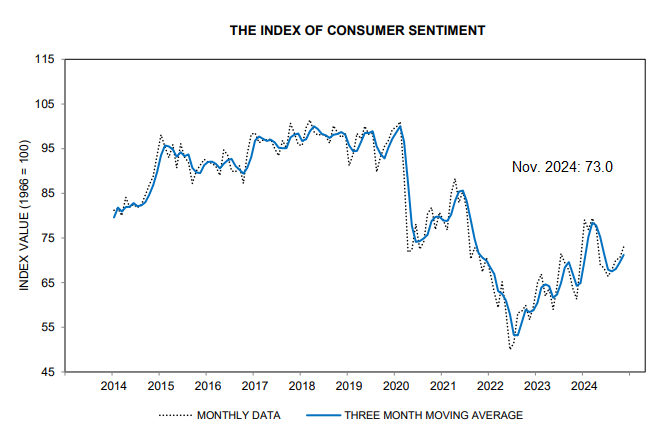

Consumer sentiment in the United States showed noteworthy improvement in early November, marking a rise for the fourth consecutive month and reaching its highest level in six months. “Although current conditions remained largely unchanged, the expectations index experienced a significant surge across the board, achieving its highest point since July 2021,” says Joanne Hsu, the director of surveys of consumers at the University of Michigan, which compiles and releases this data. These findings reflect public sentiment ahead of the November 5 election.

● Is the Chinese Economy a Miracle or a Bubble?

● Is the Chinese Economy a Miracle or a Bubble?

Lawrence J. Lau

Summary via publisher (The Chinese University of Hong Kong Press)

Since China initiated economic reform and opened its markets in the late 1970s, it has experienced an extraordinary growth rate averaging over 9 percent annually for more than four decades. This level of growth is unparalleled in recorded history. This raises critical questions: Is the Chinese economy a miracle, or merely a bubble? Will it stagnate like Japan’s did in the 1990s, or even decline? Can it avoid the so-called “middle-income trap”? If it is not truly a miracle, could China’s model of development be replicated elsewhere?

Climate Risk and Predictability of Global Stock Market Volatility

Mingtao Zhou and Yong Ma (Hunan University)

March 2024

This study explores how climate risk enhances the ability to predict global stock market volatility. By analyzing composite components derived from four individual climate risk proxies identified by Faccini et al. (2023), we find that aggregate climate risk significantly predicts stock volatility across 32 international markets. This predictability holds, even in out-of-sample tests, and is not overshadowed by other economic and financial uncertainty metrics. However, the ability of aggregate climate risk to predict volatility varies over time and across different regions; its significance diminishes during economic downturns but strengthens in areas with advanced financial markets, high energy dependence, and robust climate change preparedness. Additionally, our analysis shows that physical risks, particularly those stemming from natural disasters, yield a much stronger predictive capacity than transition risks.

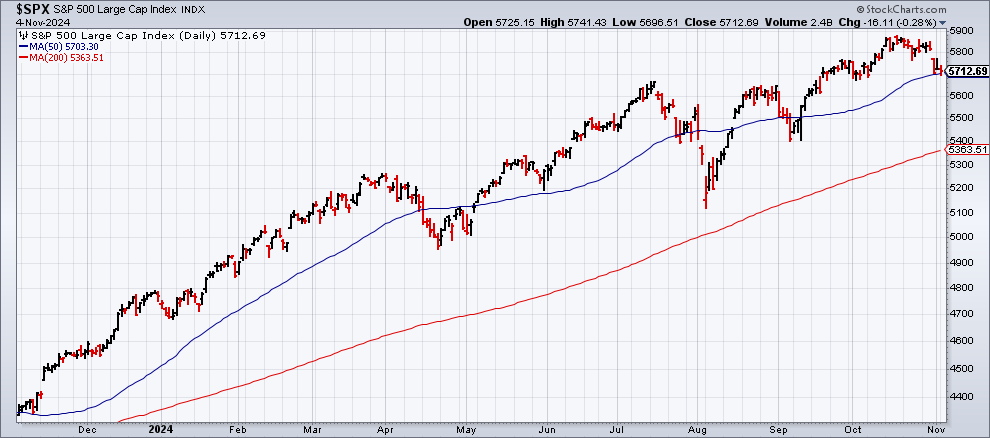

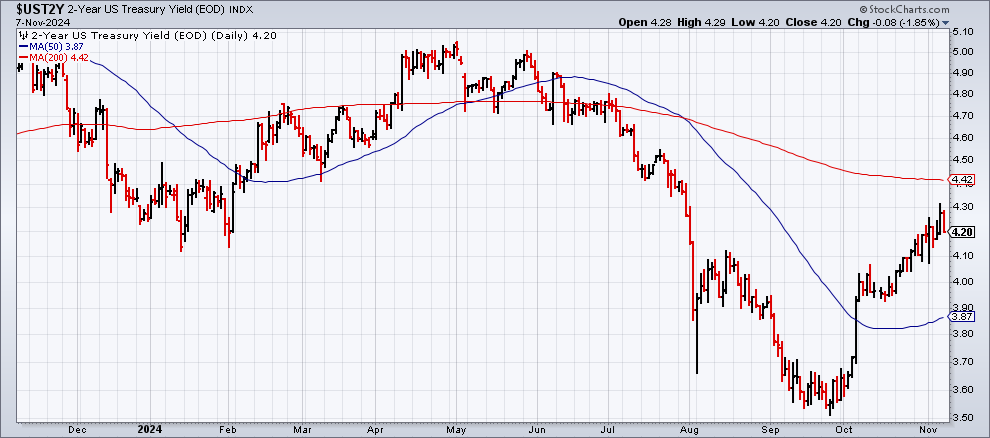

On Wednesday, the policy-sensitive US 2-year Treasury yield experienced a decline following the Federal Reserve’s announcement of a widely anticipated 1/4-point reduction in its target rate. Despite this decrease, it remains uncertain whether the upward trend will be interrupted or reversed. The 2-year yield is closely monitored as an indicator of near-term policy expectations. As of yesterday’s market close, the 2-year yield stood at 4.20%, slightly below the 4.50%-4.75% range, suggesting further rate reductions may be in the forecast. According to the Fed funds futures, there is a 71% probability of another 1/4 point rate cut in the upcoming FOMC meeting.

While the appetite for US equity risk has been teetering in recent months, it experienced a resurgence on the trading day following Trump’s electoral victory. Several indicators, based on various sets of ETF pairs through Wednesday’s close (November 6), showed a bullish shift. The notable exception remains the bond market, which is facing new weaknesses.

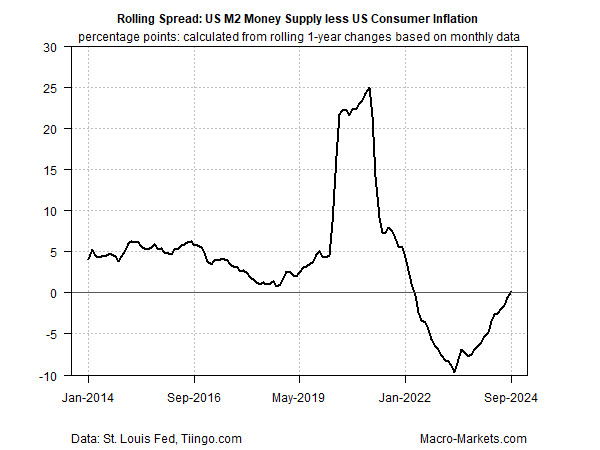

Today, the Federal Reserve is expected to announce a reduction in its target rate, although the implications of such cuts are under scrutiny in light of Tuesday’s election results. A research note from TMC Research suggests that the central bank should refrain from further cuts until the potential inflationary effects of Donald Trump’s policy agenda become clearer. The report indicates, “Donald Trump’s election win seems to have shifted the prudential assumptions surrounding monetary policy in the near term.” While the overarching themes of the president-elect’s agenda are somewhat understood, there’s ambiguity regarding the specifics and the extent to which he will pursue his proposed policies on taxes, tariffs, and immigration, among other macroeconomic issues. Additionally, it is worth noting that the broadly defined money supply (M2) has resumed real growth after having contracted for 2.5 years. This trend suggests a return of an inflationary bias in policy, albeit modestly up to September. However, as the Fed continues to ease its stance, it may encounter challenges in the first half of next year should fiscal policy changes create stronger inflationary pressures.

The consequences of elections are significant, and Donald Trump’s return to the White House as the 47th president is set to alter the political landscape. The policy differences between the incoming Republican administration and the Biden administration are pronounced across several sectors, suggesting that the upcoming four years will introduce considerable changes in trade, taxation, and other areas under federal jurisdiction. This impact may be magnified, given that Republicans have regained control of the Senate, although the status of the House is still uncertain at the time of writing.

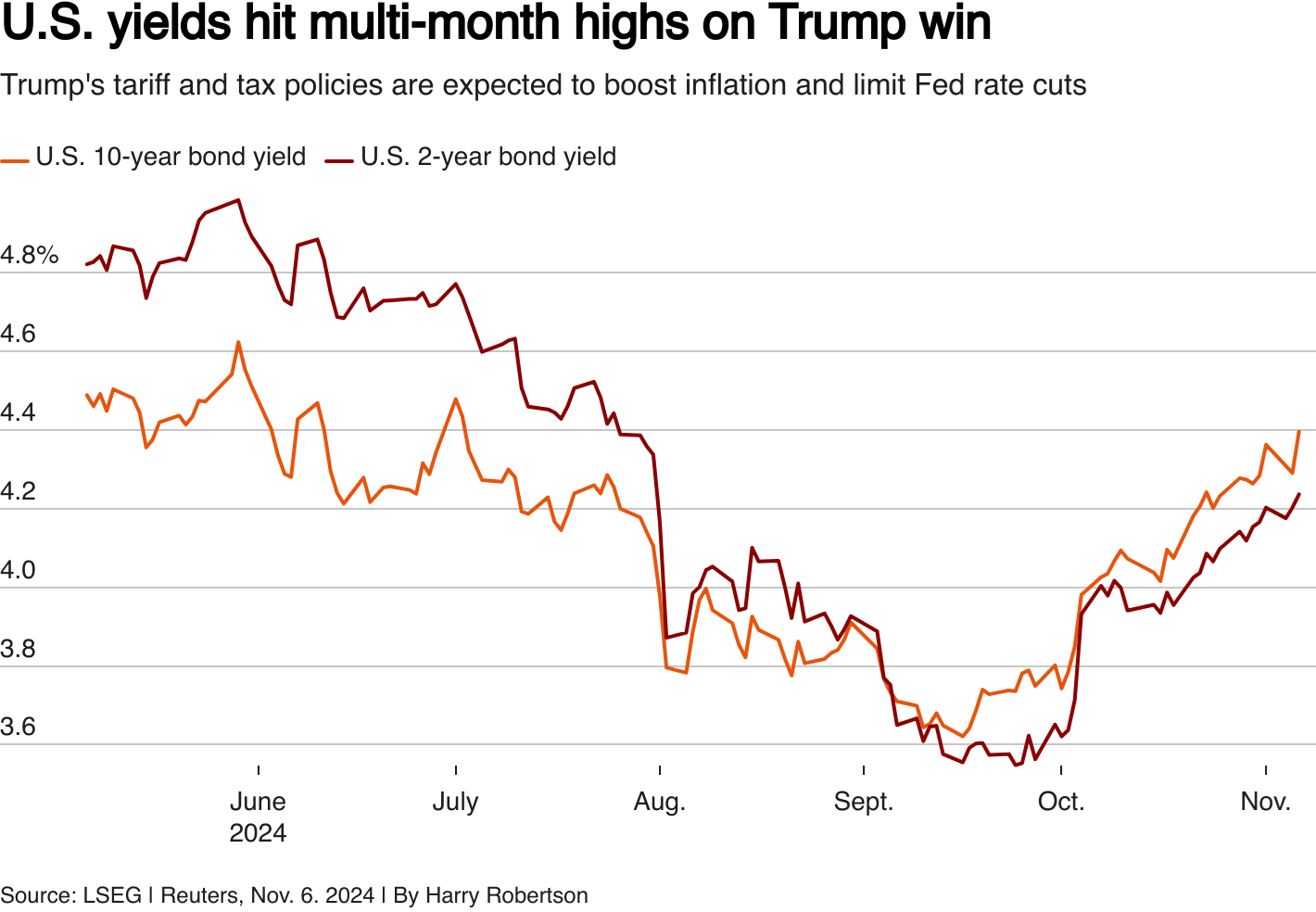

Trump’s election victory is reshaping expectations for the US economy. The incoming Republican president’s stances on various macroeconomic issues sharply contrast with the Biden administration’s priorities, including trade policies, sustainability efforts, taxation, and more. The growing federal budget deficit, which received scant attention during the campaign, will also play a pivotal role in the coming year. Mohamed El-Erian, president of Queens’ College, Cambridge, and a consultant to Allianz and Gramercy, notes, “It was once unimaginable for the US to maintain an unemployment rate around or below 4% for almost three years while running budget deficits of 6-8% of GDP.” He cautions that the bond market may exert pressure on the new administration to address the deficit, as Treasury yields increased to multi-month highs this morning. “We need to monitor the bond yields closely, as there could be a critical moment if US bond yields keep rising,” warns Seema Shah, chief global strategist for Principal Asset Management.

Historically, modeling the gold market was relatively straightforward; however, recent years have introduced complexities that complicate the key factors influencing gold price trends.

Can the stock market predict the outcome of elections? For those who subscribe to this theory, the “Presidential Predictor” is often cited, claiming an impressive track record of forecasting 21 out of the last 24 elections, including Joe Biden’s victory in 2020. Current indicators suggest a potential win for the Democratic Party and Kamala Harris, based on whether the S&P 500 Index has increased in the three months leading up to the election, a signal that the incumbent party is likely to remain in power. However, the general upward trend of the market leaves plenty of room for skepticism. “There’s no simple or even complex economic model that accurately predicts whether the incumbent party will prevail in a presidential election,” says Jay Ritter, a finance professor at the University of Florida’s Warrington College of Business. “In the context of presidential elections, I would argue the stock market has marginal predictive ability—better than random but not significantly more reliable.”