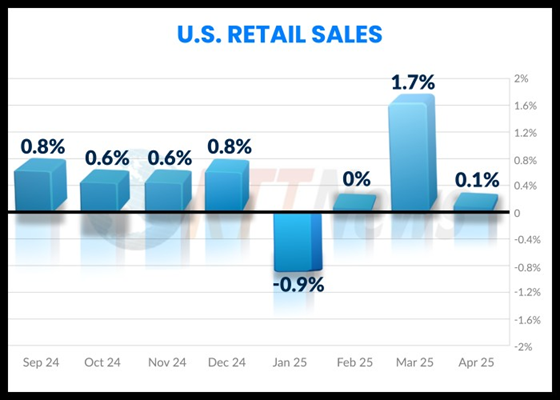

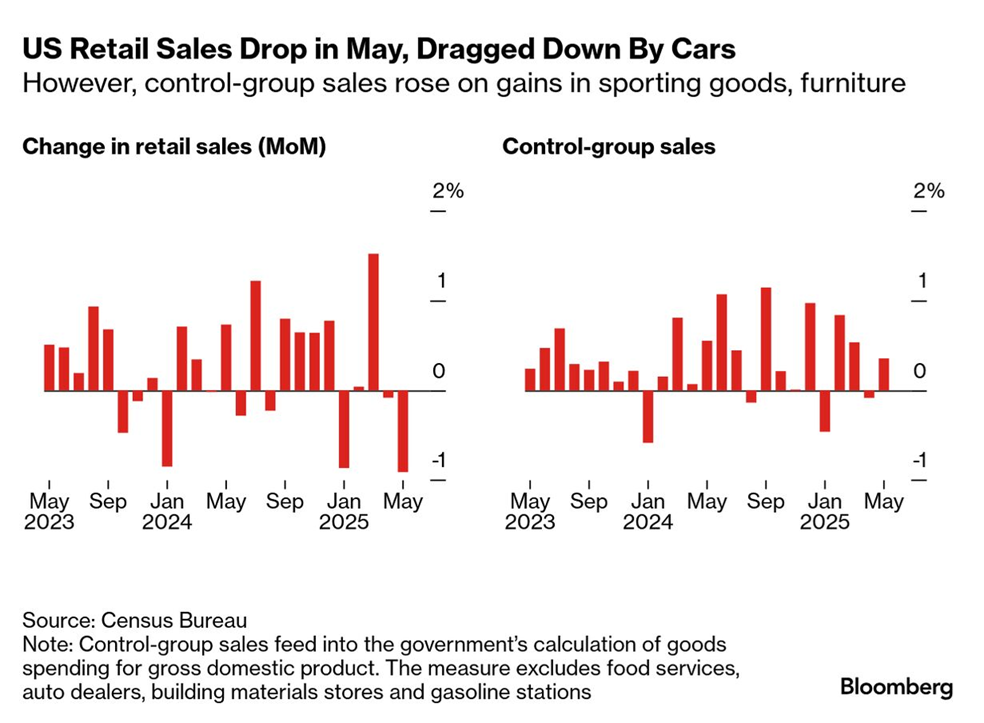

Retail sales in the US experienced their largest decline in four months this May, falling more than anticipated. Michael Pearce, the deputy chief economist at Oxford Economics, stated, “Tariff announcements clearly influenced the timing of significant purchases, particularly in the automotive sector. However, there are currently few indicators suggesting that tariffs are causing a broader reduction in consumer spending. We anticipate a more noticeable slowdown in the latter half of the year, as tariffs begin to impact real disposable incomes.”

Amid a year filled with shocks, turmoil, and tariffs, the sentiment among investors has been fluctuating as they attempt to gauge the future of risk and reward. However, as we approach the midpoint of 2025, stocks within the industrial sector are gaining stability and have emerged as the top performers, based on a selection of ETFs as of the market close on June 16.

Fed funds futures indicate a strong likelihood that the Federal Reserve will maintain its target interest rate during the policy announcement scheduled for 2:00 PM Eastern Time today. The key attention will be on the remarks made by Fed Chair Jerome Powell during the press conference beginning at 2:30 PM. Investors will closely watch for any indications regarding ongoing inflation concerns, the future of rate cuts, and general economic projections. Additionally, revised economic forecasts will be released today by the Fed.

The ongoing conflict between Israel and Iran continued into its fourth day as both nations launched attacks on Monday. This ongoing violence threatens to elevate oil prices over a prolonged period and could usher in a new wave of instability in a global economy still grappling with heightened tariff risks.

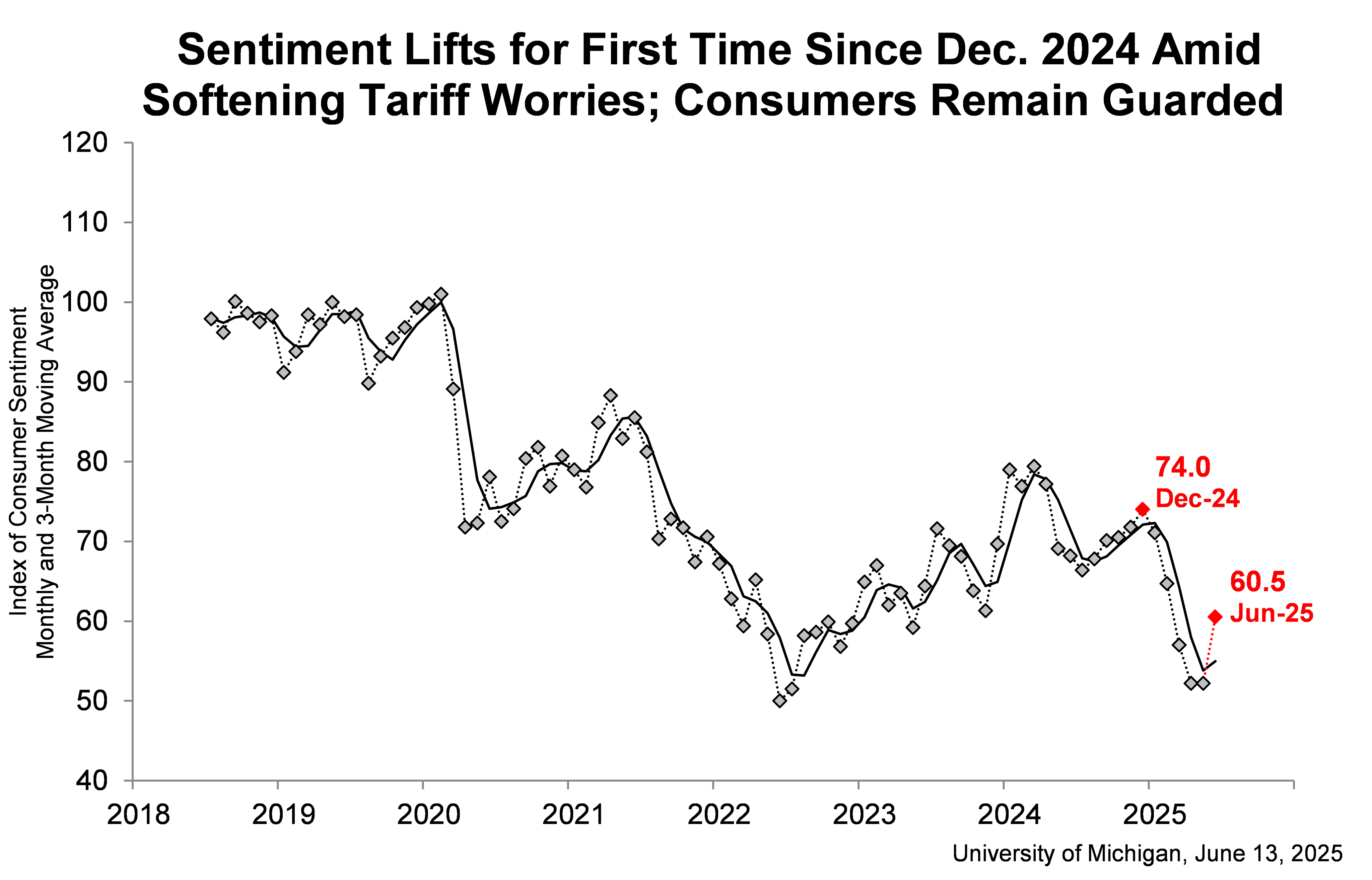

In June, US consumer sentiment made a modest improvement for the first time this year. Despite the uptick, the University of Michigan’s index remains approximately 20% below the level seen in December 2024, which marked a post-election spike. Joanne Hsu, the survey director, noted, “Consumers seem to have somewhat stabilized from the shock caused by the exceptionally high tariffs introduced in April and the ensuing policy volatility. However, they still perceive a wide array of economic risks.”

● The Haves and Have-Yachts: Dispatches on the Ultrarich

● The Haves and Have-Yachts: Dispatches on the Ultrarich

Evan Osnos

Interview with author via Marketplace.org

There are over 3,000 billionaires globally, with nearly a third residing in the U.S. Between President Trump’s first and second inaugurations, wealth held by America’s billionaires more than doubled.

Yet, the lifestyles and values of these ultra-wealthy individuals are often a mystery to the general public. While people may recognize a few names such as Jeff Bezos, Mark Zuckerberg, or Warren Buffet, their behaviors and priorities tend to elude many.

Throughout that period, Evan Osnos, a staff writer for The New Yorker, conducted an in-depth exploration of this demographic, compiling essays resulting in his new book, “The Haves and the Have-Yachts: Dispatches on the Ultrarich.”

Stock-Bond Return Correlation: Understanding the Changing Behaviour

David G. McMillan (University of Stirling)

March 2025

The relationship between stock and bond returns remains a critical area of focus due to its implications for portfolio performance. Previous evidence, primarily from the United States, indicates variable switching behaviour, suggesting that bonds alternate between acting as a diversifier and a hedge. This paper investigates the time-sensitive nature of the stock-bond correlation across G7 markets, its economic drivers, and whether these drivers themselves show variability over time. An analysis of monthly data from 1980 to 2023 reveals that the correlation shifted from positive to negative around 2000 for six of the seven markets, with Japan experiencing a change in the early 1990s.

Israel unleashed an attack on Iran’s capital early Friday, focusing on the nation’s nuclear initiatives. This assault also claimed the lives of two high-ranking military officials. Iran has vowed a “severe” retaliation. President Trump has stated that “subsequent attacks” could be “even more brutal,” warning Tehran that they “must reach an agreement before facing dire consequences.”

The market premium for the U.S. Treasury yield remained relatively stable in May compared to its “fair value” estimate. The 10-year yield traded within a narrow range during the month, and with minimal changes noted in model-based assessments of its fair value, this update for May aligns with the previous month’s analysis.

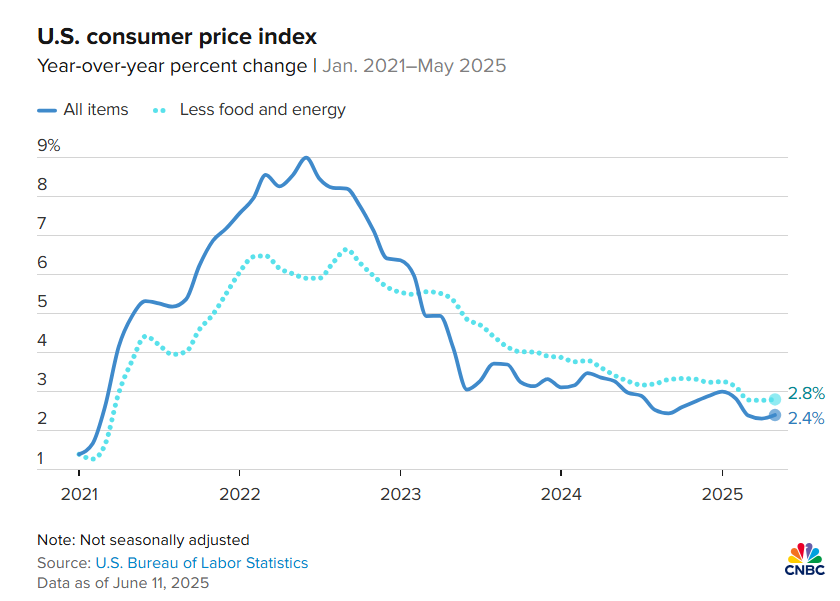

US consumer inflation has remained subdued in May, with the year-over-year change in headline CPI decreasing to 2.4%. Core CPI, which serves as a more reliable measure of trend, remained stable, suggesting that price pressures may persist at a “sticky” level as tariffs begin to influence prices. Mark Zandi, chief economist at Moody’s, remarked, “This is a very positive report. Essentially, it indicates that inflation has finally returned to the Federal Reserve’s annual target.” He also noted, “This could be the calm before an inflation storm. This [report] still reflects the disinflation trend that began a few years ago and continued throughout May.”

In the articles above, a range of economic updates and developments highlight significant trends in US retail sales, consumer sentiment, inflation, and international conflicts. These factors shape the current economic landscape, emphasizing the complexities investors face as they navigate through rising uncertainties. As we continue to monitor these evolving situations, insights into market behaviors and strategic adjustments will be crucial for financial decision-making.