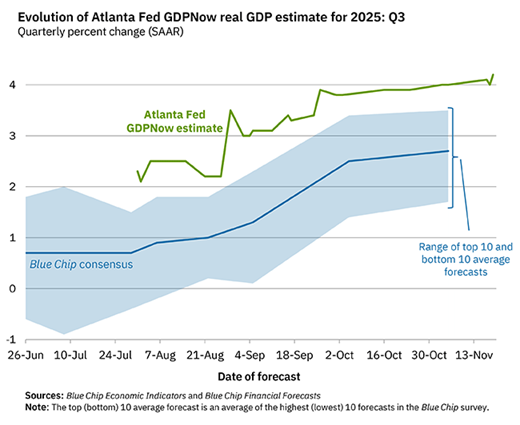

The Atlanta Fed’s GDPNow model anticipates a robust increase in US economic activity for the third quarter. Q3 output is predicted to rise by 4.2% from July to September, slightly surpassing Q2’s impressive 3.8% growth. Although the official report for Q3 is expected, its release has been postponed due to the government shutdown.

The government has reopened, allowing for the recovery of missing economic data. Initial indicators show that hiring has slowed in October. In addition, the Labor Department will release its postponed payroll report for September tomorrow.

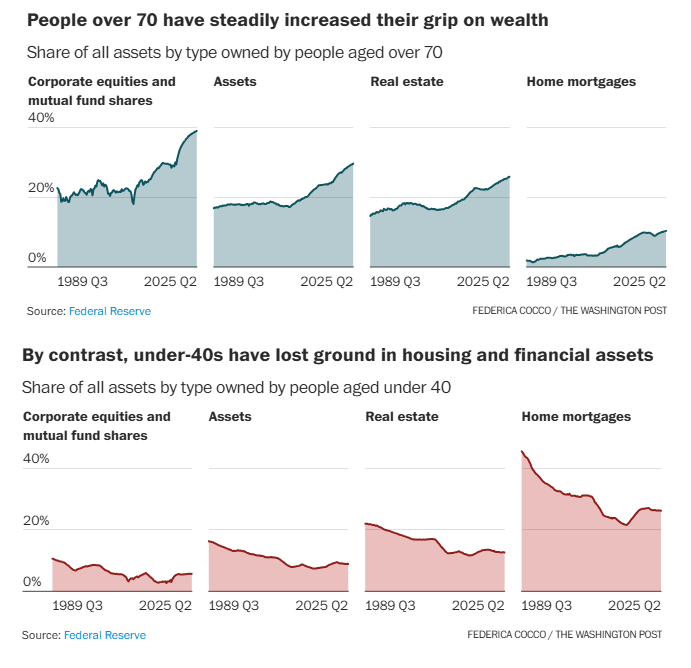

The baby boomer generation possesses over $85 trillion in assets, a feat that younger generations like Gen X and millennials may find difficult to replicate. “It’s remarkable how their relative wealth has surged over the past 30-plus years,” said Edward Wolff, an economics professor at New York University, as reported by The Washington Post. “In 1983, many were among the lowest wealth groups.” His working paper for the National Bureau of Economic Research examines data from 1983 to 2022, revealing that older boomers have seen significant wealth increases while their younger counterparts have experienced relative declines.

In 2025, technology stocks, followed closely by utility sector stocks, are leading the US stock market, as observed through a range of ETFs up to the market close on November 17.

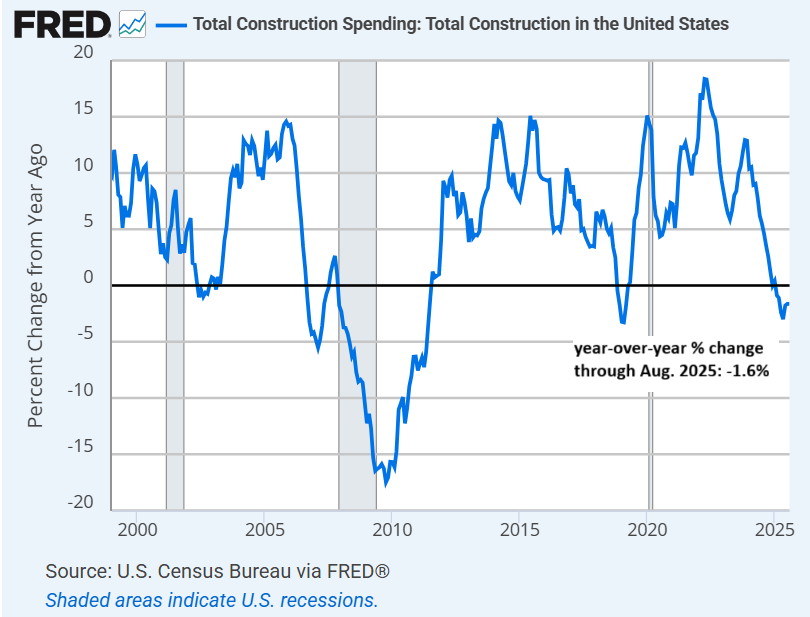

Year-over-year US construction spending continues to decline, falling 1.6% in August compared to the same month last year. This decline has persisted since February.

As November began, markets exhibited moderate confidence that a slowing labor market would lead the Federal Reserve to reduce interest rates for the third time at the upcoming December 10 policy meeting. However, this confidence is waning as concerns about inflation reemerge.

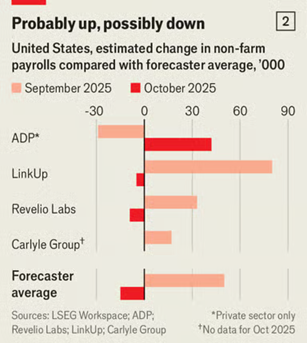

The US Labor Department has announced the upcoming release of the delayed payroll report for September this Thursday, November 20. “The lack of timely data created uncertainty in the markets and for the Fed, which had to rely on alternative sources to assess the economic outlook,” stated Bank of America economist Shruti Mishra in a note. “Now that the shutdown is resolved, all attention will be on the incoming data.” According to The Economist, “ADP indicates a decline in September, while Revelio Labs suggests an increase, highlighting a potential rebound in October.”

The US Labor Department has announced the upcoming release of the delayed payroll report for September this Thursday, November 20. “The lack of timely data created uncertainty in the markets and for the Fed, which had to rely on alternative sources to assess the economic outlook,” stated Bank of America economist Shruti Mishra in a note. “Now that the shutdown is resolved, all attention will be on the incoming data.” According to The Economist, “ADP indicates a decline in September, while Revelio Labs suggests an increase, highlighting a potential rebound in October.”

● The History of Money: A Story of Humanity

● The History of Money: A Story of Humanity

David McWilliams

Review via New York Post

This insightful narrative examines various historical moments, revealing a troubling trend: humanity repeatedly makes similar money-related errors because the fundamental nature of money remains unchanged. It’s always about trust, pricing time and risk, and has the power to build or destroy empires. “Money can wield more influence than religion, ideology, or armies,” McWilliams notes. “Disturbing the financial system affects far more than just prices and economics — it influences people’s minds.”

Bubble Beliefs

Christian Stolborg (Copenhagen Bus. School) and Robin Greenwood (Harvard)

October 2025

This study explores expert beliefs surrounding boom-bust cycles in which highly valued individual US stocks undergo dramatic price increases followed by crashes. During these price surges, analysts forecast remarkable earnings growth and high near-term returns. Short interest remains low, and media coverage rarely refers to a “bubble,” even during crashes. Optimism often predicts crashes: the most optimistic forecasts indicate the highest crash risks. These findings align with theories of bubbles fueled by overly positive expectations about fundamentals and future prices, with limited recognition of the bubble from skeptics, unless the share lending market provides signals.

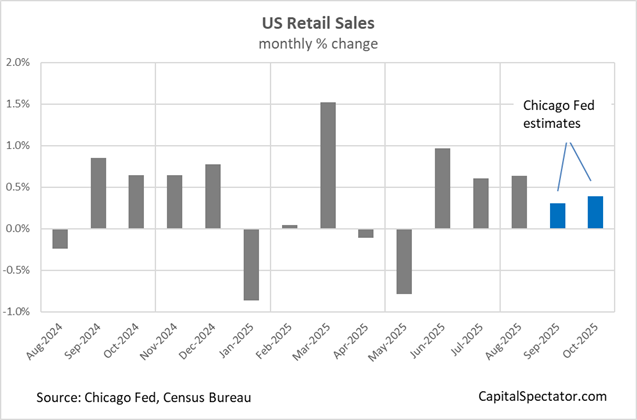

According to data from the Chicago Federal Reserve, US retail spending increased for the fifth consecutive month in October. The estimate, which tracks sales in retail and food services excluding motor vehicles and parts, shows a 0.4% rise for last month, slightly up from 0.3% in September. These more recent gains are also more modest compared to the retail sales data published by the Census Bureau, which was last updated before the government shutdown.

The current economic landscape continues to evolve with various indicators showcasing a mix of optimism and caution. As data begins to flow following the government reopening, attention will be focused on upcoming reports that could further inform our understanding of the economic environment.

In conclusion, tracking these developments will be crucial as they will shape both market reactions and policy decisions in the coming months. Remaining informed is essential for navigating this dynamic economic climate.