In this issue:

- Global markets recover

- Impressive week for portfolio-strategy benchmarks

- Risk-on strategy pays dividends for one of our managed-risk approaches

February Resurgence: The late-January downturn was merely a temporary setback for risk assets, which surged back this week. Equities across various sectors experienced gains, with African stocks leading the charge, outperforming the other funds in our global asset class proxies. (For a comprehensive overview of the risk metrics presented in the table below, along with detailed profiles of the strategies and benchmarks mentioned, refer to this summary.)

The Treasury market is currently reflecting an increased expectation of reflation, with the Federal Reserve showing a preference for allowing economic growth to continue for an extended period without significant monetary intervention in response to early signs of pricing pressure. This sets the stage for the possibility of higher inflation. Nonetheless, the current data does not provide substantial evidence in support of this. Could 2021 mark a significant shift towards inflation?

* Biden terminates U.S. support for Saudi Arabia’s military actions in Yemen

* J&J requests approval from U.S. regulators for its Covid-19 vaccine

* The House removes Marjorie Taylor Greene from her committee roles

* The Senate rejected the proposed minimum wage increase in Biden’s relief package

* An EU diplomat informed Russia that ties are strained due to the situation involving Kremlin critic Navalny

* A U.S. warship sailed close to the Chinese-controlled Paracel Islands

* The Bank of England indicated that negative interest rates may be a possibility soon

* U.S. job cuts rose to their highest January levels since 2009

* U.S. factory orders increased in December, marking the eighth consecutive month of gains

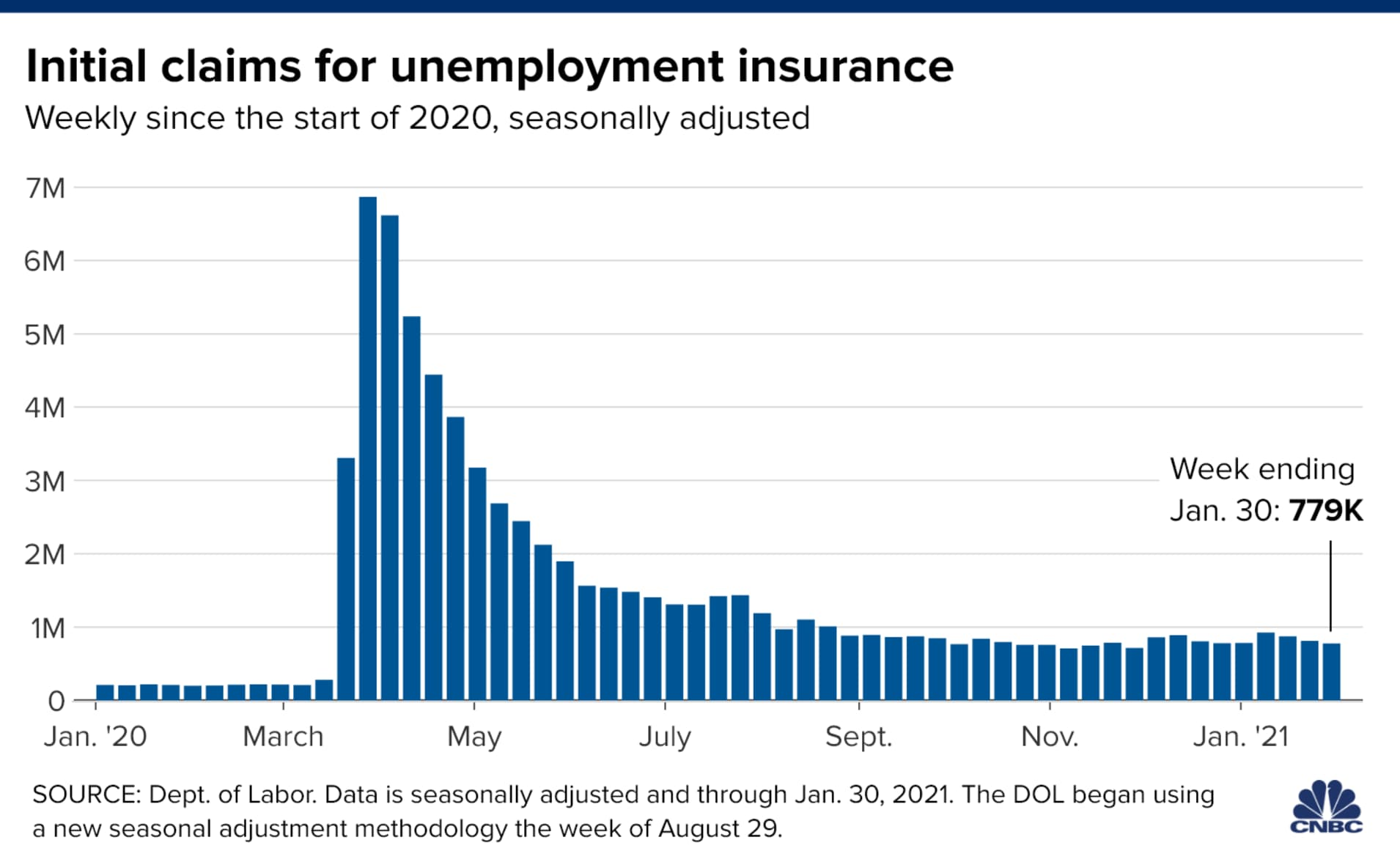

* U.S. jobless claims dropped to a two-month low last week:

The year has just begun, yet emerging trends could shape 2021 for both leaders and laggards in the U.S. and global equity markets. Analyzing a range of exchange-traded funds reveals three significant trends worth observing: leadership in energy stocks, growth in small-cap shares, and opportunities within Asian markets excluding Japan.

* Researchers investigate mixed vaccine doses in response to the surge of COVID-19 variants

* The House GOP upholds Liz Cheney in leadership, countering Trump loyalists

* The Treasury yield curve has reached its steepest point since 2017

* Biden presses forward with his proposed $1,400 stimulus checks

* Survey indicates nearly 70% of Americans favor Biden’s $1.9 trillion relief package

* Global economic recovery slowed for a third consecutive month in January

* Is tightening liquidity in China a potential global challenge?

* Sen. Klobuchar (D-Minn.) proposes comprehensive antitrust reform legislation

* A passive investment strategy has proven a successful approach

* U.S. Services PMI shows a “sharp upturn in business activity” for January

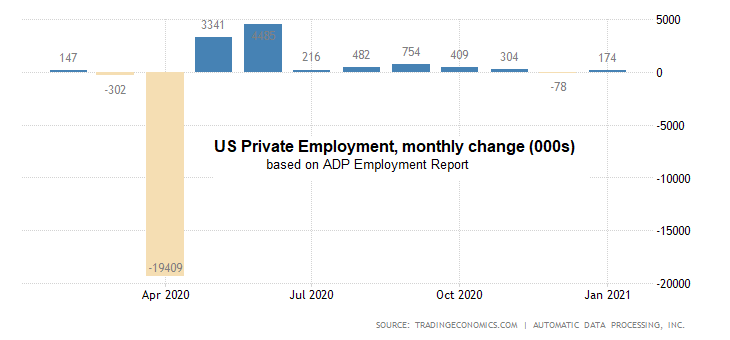

* U.S. private payrolls grew modestly in January after a decline in December:

There’s a compelling argument gaining traction that the recent superior performance of technology stocks relative to the broader market warrants treating this sector as a distinct asset class.

* Senate Democrats might advance Biden’s relief package without Republican backing

* Today’s ADP report on U.S. payrolls for January is expected to show a slight increase

* Jeff Bezos will resign as Amazon’s CEO

* Eurozone consumer inflation rose significantly more than anticipated in January

* Europe’s economy continued to shrink in January amid a subdued services sector

* China’s service sector expansion slowed in January due to a resurgence of the coronavirus

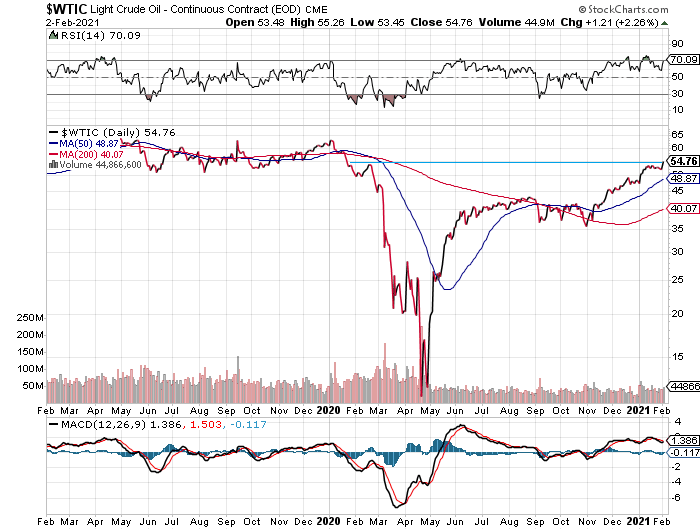

* U.S. crude oil prices (West Texas Intermediate) surged to nearly $55 per barrel, hitting a one-year high:

The anticipated risk premium for the Global Market Index (GMI) remains steady in the mid-5% range. In the latest update, the long-term projection adjusted slightly downwards to 5.4% for January, marginally below last month’s estimate of 5.5%. This forecast offers a long-term perspective on the index’s expected performance over the “risk-free” rate through a risk-based model (more details below).

* Republicans encourage Biden to consider a smaller relief package

* China’s top diplomat cautions the U.S. against crossing ‘red lines’ concerning human rights issues

* The Myanmar coup complicates Biden’s approach to Asia

* The CBO forecasts continued economic expansion in the U.S. for 2021

* U.S. construction spending increased for the third consecutive month in December

* Eurozone’s economy contracted by 0.7% in the last quarter of 2020

* The U.S. Manufacturing PMI reached a record high in January

* The U.S. ISM Manufacturing Index showed that sector growth slowed in January:

Stocks in emerging markets continued to outperform other major asset classes throughout January, marking them as the top performers for the month.

Continue reading