In recent headlines:

- Biden invites Republican senators to the White House to discuss relief efforts.

- Myanmar’s military takes control and detains civilian leader Aung San Suu Kyi.

- Thousands are arrested in Russia amid protests demanding the release of opposition leader Navalny.

- Investor enthusiasm on Reddit shifts focus to precious metals.

- China’s economy is projected to surpass the US earlier than previously expected.

- Manufacturing growth in China slowed and reached a seven-month low in January.

- Eurozone manufacturing continued to show “resilience” in January, remaining steady.

- The UK manufacturing sector declined to a three-month low in January.

- US Consumer Sentiment Index stabilized in January with a slight decrease.

- Factory activity in the Chicago region continued to grow at a strong pace in January.

- Potential changes in US cryptocurrency regulation are anticipated under Biden’s administration.

- Pending home sales in the US declined in December for the fourth consecutive month.

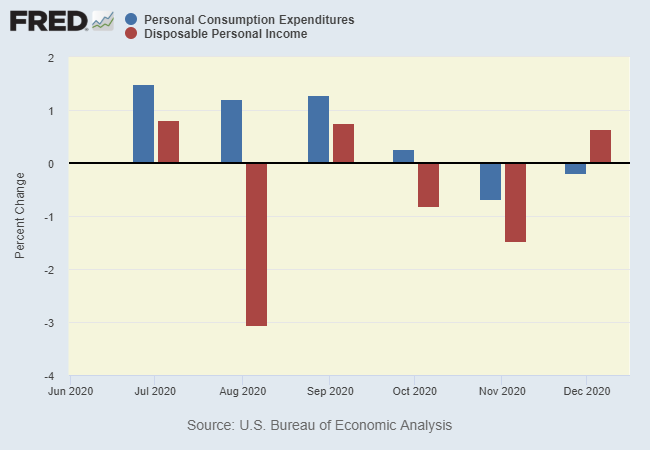

- Consumer spending in the US fell in December for the second month in a row:

This week’s focus:

- Risk aversion returns to global markets

- No safe havens are evident in strategy benchmarks

- Managed-risk strategies also faced challenges

January ends on a rough note: Global markets took a hit this week. While commodities and Treasuries saw slight increases, our ETF proxies for the major asset classes were predominantly in the red.

Modern finance hinges on the idea that beta (market) risk is the leading factor influencing performance. However, various empirical analyses of the capital asset pricing model (CAPM) over time suggest otherwise. While multiple efforts have been made to recalibrate CAPM for a more accurate mapping of risk and return, results have been inconsistent. Recent research papers aim to bring us closer to redefining a CAPM-based approach to asset pricing, aligning theoretical ideals of risk and return with practical outcomes in investment management.

Key developments include:

- Democrats plan to take significant action on the COVID-19 rescue plan, with or without Republican support.

- The Novavax vaccine is reported to be 90% effective, although less effective against certain variants of COVID-19.

- Consumer income in the US likely increased, while spending saw a decline in December’s report.

- Speculation arises about a potential currency war with Treasury Secretary Janet Yellen.

- General Motors announces its goal to sell only zero-emission vehicles by 2035.

- The US economy is projected to have grown at an annualized rate of 4.0% in the fourth quarter, slightly below expectations.

- The US Leading Economic Index increased in December, albeit at a slower rate than in November.

- Germany’s economy managed a slight gain in the fourth quarter of last year.

- New home sales in the US rose in December, marking the first increase since July.

- The US trade deficit narrowed in December.

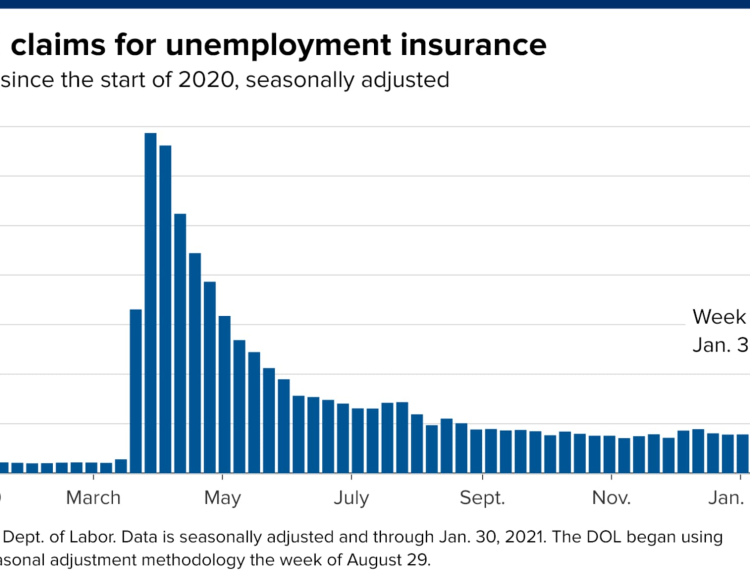

- Jobless claims in the US have increased, though less than anticipated and remain uncomfortably high:

The energy sector faced significant challenges in 2020, but it has experienced a notable rebound in 2021, as evidenced by various exchange-traded funds. While this recovery is promising, it is doubtful that traditional energy stocks will embark on a sustained bull market.

Recent significant developments include:

- Biden halts oil drilling on federal lands as part of climate change initiatives.

- China issues warnings regarding Taiwan with an increasingly aggressive stance.

- Secretary of State Antony Blinken criticizes Russia’s actions against Alexei Navalny.

- The Biden administration is reviewing US weapon sales to Gulf Arab countries.

- The fourth quarter US growth rate is expected to exceed 4% annually, according to the upcoming GDP report.

- A research group anticipates a wave of US retail store closures in 2021 due to COVID-19 impacts, projecting over 10,000 closures.

- Research indicates that while vaccines may help, they might not completely eradicate coronavirus.

- The Federal Reserve maintained low rates and noted a slowdown in economic growth.

- US core capital goods orders increased for the eighth consecutive month in December:

The US Treasury market is displaying signs of confusion. While nominal yields have recently been on the rise, real (inflation-adjusted) rates are continuing to decline, dipping deeper into negative territory. One of these trends will eventually stabilize in alignment with the other. The outcome likely depends on how inflation data unfolds in the upcoming months.

Recent political developments include:

- Senate votes indicating that Trump is unlikely to be convicted in the impeachment trial.

- A surge in household savings may contribute to a robust economic recovery this year.

- Pfizer is developing a booster shot for COVID-19 variants.

- Biden raises the issue of election interference in a conversation with Russia’s Putin.

- The Federal Reserve is expected to maintain its aggressive stimulus measures during today’s FOMC meeting.

- US Consumer Confidence Index saw a modest increase in January.

- German consumer confidence deteriorated amid ongoing COVID-19 restrictions.

- Manufacturing growth in the Mid-Atlantic region slowed down in January.

- US home prices increased by 9.5% year-over-year in November, marking the highest growth rate in seven years:

The government’s preliminary estimate for fourth-quarter economic activity is anticipated to confirm a continuing recovery following the sharp recession triggered by the coronavirus. While this week’s data is expected to show a considerable slowdown in growth compared to the unusually high increase in the third quarter, the release from the Bureau of Economic Analysis on January 28 is set to offer positive insights.

In summary, recent developments across various sectors highlight a mixture of optimism and caution as economic indicators evolve. The interaction of political actions, market movements, and consumer behavior will continue to shape the landscape. As we move forward, it remains crucial to monitor these trends to gain a clearer understanding of the trajectory ahead.