Last week, our three proprietary strategies had varied performance compared to the benchmark (G.B16), which decreased by 1.5% amid a widespread selloff in global markets.

Mark Spitznagel

Essay by the author via Financial Times

In the realm of investment, the pursuit of safety can often be more expensive than the risks it aims to mitigate. The real cost may not be immediately apparent, manifesting as missed opportunities rather than observed mistakes. Investors frequently attempt to mitigate risks through various strategies, yet these can inadvertently harm their portfolios and contradict their initial intentions. Most conventional risk mitigation techniques often culminate in underperformance, all in an effort to avoid losses in bearish markets.

- The safe-haven Treasuries trade continues as most risk assets decline this week

- Strategy benchmarks experienced losses across the board

A challenging week for (most) markets: Negative movements were evident almost universally, except for Treasuries and investment-grade US corporates. Our 16-ETF opportunity set leaned heavily toward declining prices for the trading week ending Friday, August 20.

Risk manifests in various forms, making it no surprise that there are countless risk metrics to consider. In a new series of posts, CapitalSpectator.com will spotlight some lesser-known indicators and discuss their applications. We’ll begin with capture ratios.

* The Delta coronavirus variant is a risk factor affecting stocks and the economy.

* Rising Delta cases could delay or reverse plans to return workers to offices.

* Researchers criticize the US’s plan for Covid-19 vaccine booster shots next month as premature.

* China has approved a sweeping privacy law to limit data collection by tech companies.

* The US Philly Fed Manufacturing Index indicates slower growth in August.

* The US Leading Economic Index reported ‘another substantial gain in July.’

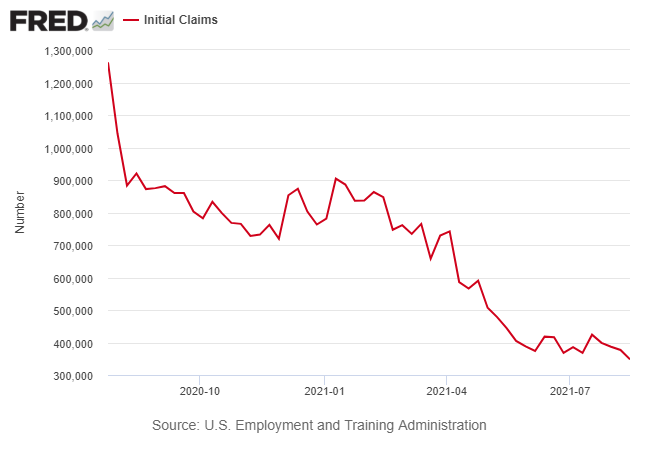

* US jobless claims fell to a pandemic low last week.

As of August 18, financials and real estate investment trusts (REITs) have eclipsed energy stocks as the top-performing sectors in US equities for the year, according to a suite of exchange-traded funds.

* Republican governors prefer Covid treatments over mask mandates as cases spike.

* US troops may remain in Afghanistan beyond the deadline, Biden states.

* There are reports of resistance to Taliban rule emerging in multiple Afghan cities.

* The Federal Reserve is preparing to taper bond purchases later this year, according to minutes released.

* A Fed official warns that extensive bond purchases may not suit the US economy.

* The 30-year to 5-year Treasury spread indicates confidence in the Fed’s policy outlook.

* The Taliban now controls $1 trillion worth of Afghanistan’s mineral resources.

* China’s tech giants are facing further challenges due to a new set of proposed regulations.

* A federal judge reverses the Trump administration’s approval of an Alaskan drilling project.

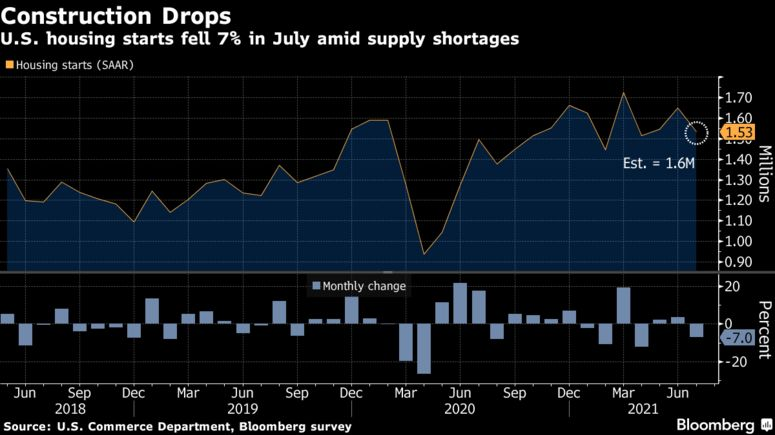

* US housing starts decreased more than predicted in July.

Starting this month, The ETF Portfolio Strategist will release monthly total return forecasts for the major asset classes, developed from a series of models. This initiative aims to average several model outputs to achieve slightly more dependable forecasts than those based on a single model.

The quest for the ultimate diversification strategy is continual, yet it rarely yields new insights beyond what is already common knowledge. Nevertheless, keeping track of various aspects of diversification remains valuable and sometimes necessary, including monitoring return distributions, which are constantly evolving.

* Uncertainty persists following the Taliban takeover of Afghanistan.

* US investors reduced their stakes in Chinese investments as Beijing escalates its tech crackdown.

* Revised inflation rates for the Eurozone confirm an annual increase of 2.2%, the highest in three years.

* UK inflation slowed more than anticipated in July.

* Homebuilder sentiment in the US continued to slide, reaching a one-year low.

* US industrial output rebounded in July, continuing its recovery.

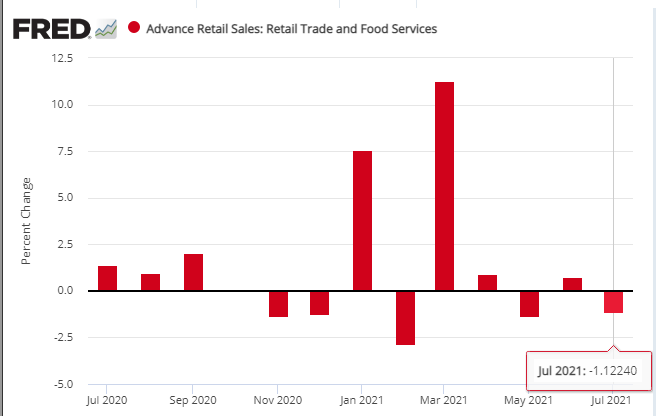

* Consumer spending in the US during July reflects a shift toward services.

* However, US retail sales fell more than expected in July: