The age-old saying that markets can ascend a wall of worry remains relevant today. Despite numerous warnings from analysts predicting potential downturns, trend profiles suggest a lack of apprehension. This is illustrated through various ETF proxies that reflect the current risk appetite, based on prices as of yesterday’s close (May 22).

* China conducts military drills around Taiwan following the inauguration of its new president.

* Federal Reserve minutes express concerns about insufficient progress on inflation.

* The Eurozone’s economic recovery strengthens for the third consecutive month in May.

* China might increase tariffs on vehicle imports by up to 25%.

* Business inflation expectations remain unchanged at 2.4% in May, according to the Atlanta Fed.

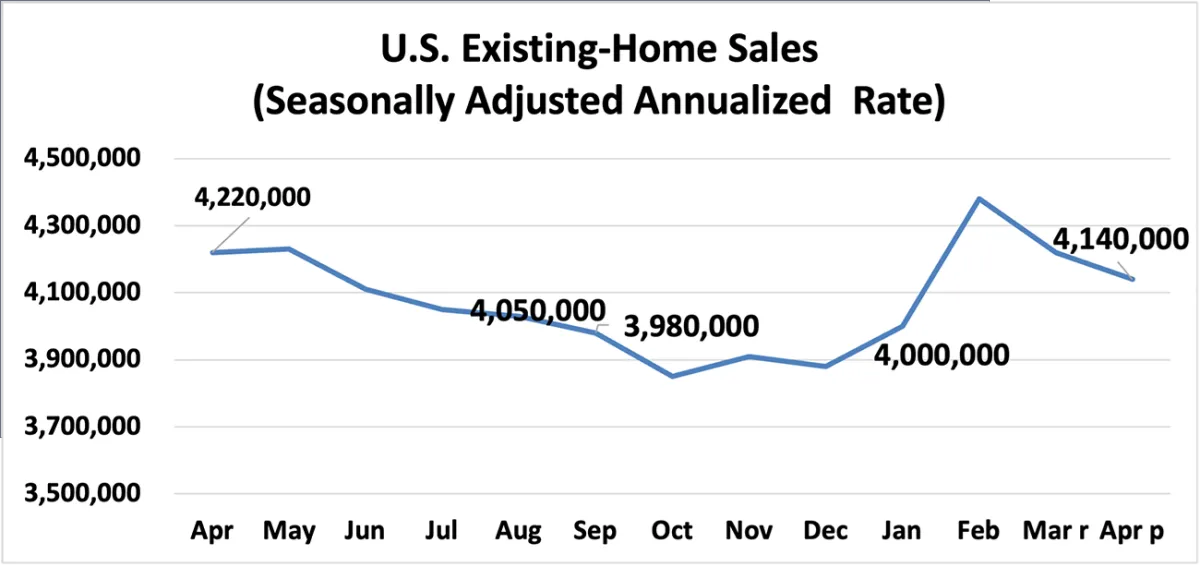

* US existing home sales decline for the second consecutive month in April.

The US economy is projected to exhibit a slight uptick in activity for the second quarter. This forecast is based on the median estimates derived from a collection of nowcasts compiled by CapitalSpectator.com. Although more than half of the relevant data for the quarter is still pending, initial indicators are leaning positively.

* Fed’s Waller calls for ‘several months’ of strong inflation data before considering rate cuts.

* Biden plans to release 1 million barrels of gasoline from reserves to lower prices.

* Overall US single-family rent increased in March compared to a year earlier.

* AI is expected to be a positive driver for stocks over the next decade, according to the former CEO of Cisco.

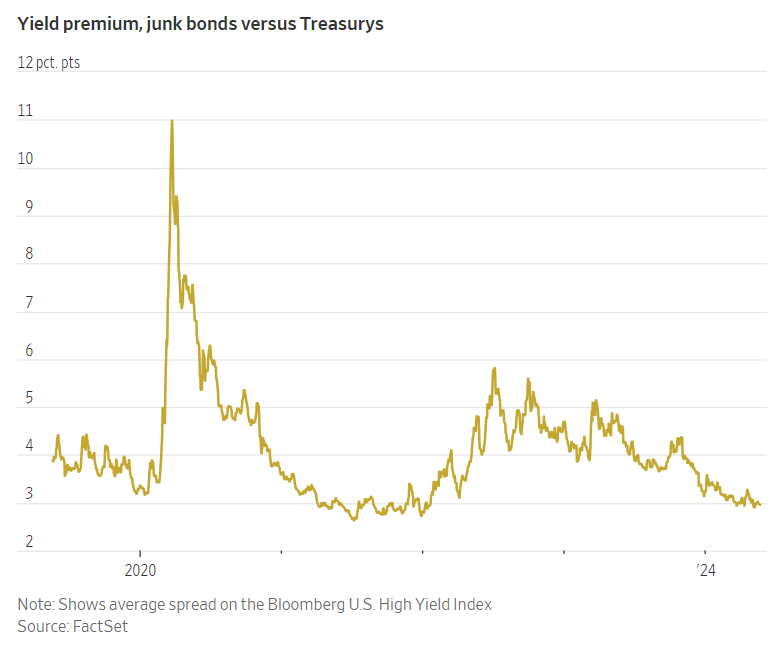

* The rally in junk bonds reflects optimism regarding a soft landing for the US economy.

When the US Treasury yield curve inverts (where short-term rates exceed long-term rates), it is commonly perceived as a strong indicator of an impending recession. However, the current situation appears to be unique. The yield curve has remained inverted since July 2022, marking the longest inversion on record, yet a recession has not materialized.

* The US should collaborate with Europe to address the issue of cheap Chinese exports, stated Yellen.

* Target announces price reductions on 5,000 products.

* The electricity grid is under pressure due to the rising use of AI.

* There is no immediate need to adjust interest rates, claims SF Fed president.

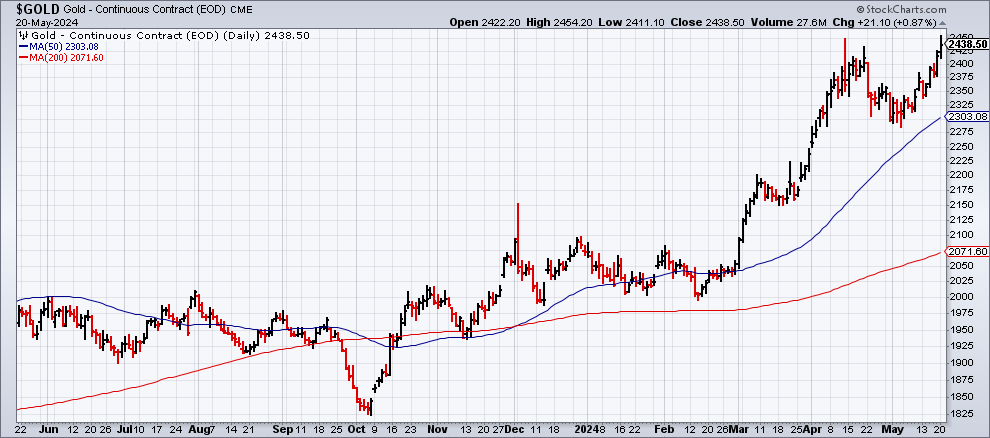

* China plays a significant role in the rally observed in gold prices.

Last week’s noteworthy surge in commodities has widened the performance gap for this asset class compared to other global markets, as indicated by a selection of ETFs through the closing of Friday (May 17).

* Iran’s president dies in a helicopter crash.

* Gold reaches an all-time high during early Monday trading.

* Copper achieves record levels amid expectations of ongoing supply shortages.

* Could the new tariffs imposed by Biden signal the end of inexpensive Chinese goods in the US?

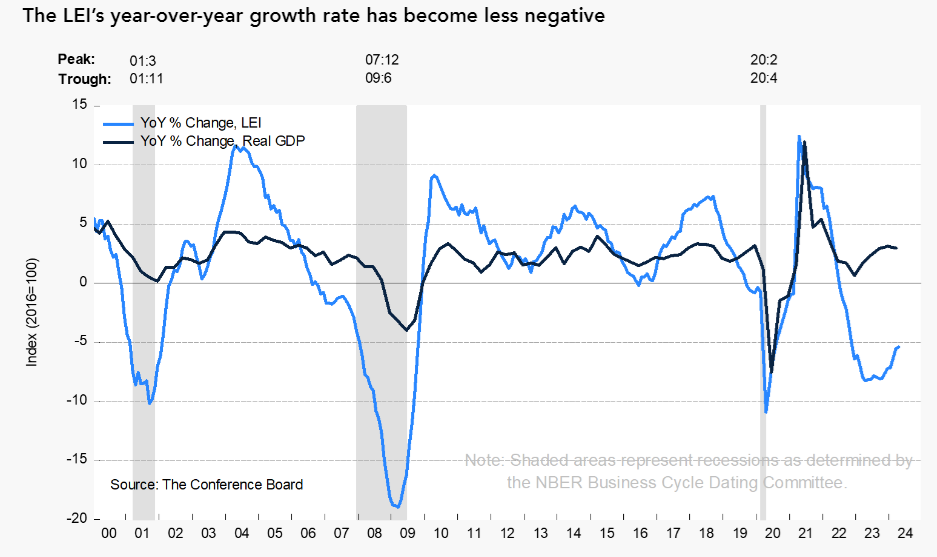

* The US Leading Economic Index remains negative in April, indicating continued growth challenges.

● A Map of the New Normal: How Inflation, War, and Sanctions Will Change Your World Forever

Jeff Rubin

Adapted essay from book via The Globe and Mail

The world is embroiled in a continually escalating global trade conflict. Almost daily, new sanctions are being imposed, sparking reciprocal actions against Western goods.

Where might this lead? Can the West still achieve victories in such conflicts, as it has in the past? If not, what are the implications for failure?

Alongside sanctions, a new global order has emerged, wherein the United States and its NATO partners can no longer leverage their economic and military clout to unilaterally dictate conditions to the rest of the world.

Regime-Based Strategic Asset Allocation

Eric Bouyé and Jerome Teiletche (World Bank)

April 2024

What should investors consider in the context of economic regimes? While research and practice typically approach this topic from a tactical asset allocation perspective, this article takes a different approach by addressing the issue from a strategic and analytical standpoint. We model economic regimes as a mixture of distributions, exploring the outcomes for return distributions. Subsequently, we derive the implications for portfolios constructed under popular asset allocation methodologies, such as mean-variance optimization and risk budgeting. Utilizing these analytical outcomes, we propose new portfolio construction methodologies that capitalize on information regarding macroeconomic regimes by optimizing portfolios for each regime, addressing their risk characteristics, and assessing the long-term probabilities of those regimes. Empirical evidence suggests that macro-regime-based portfolios can outperform traditional asset-based portfolios across both multi-asset and equity factor universes over a historical sample spanning over fifty years.

This format retains the original HTML structure while enhancing the clarity and readability of the content, ensuring that it flows smoothly for readers. Each section builds upon relevant economic topics and insights, creating a cohesive narrative throughout.