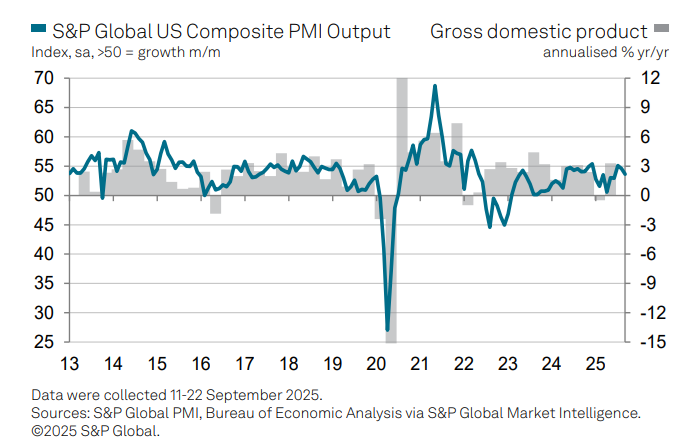

US economic growth experiences a slowdown in September, as indicated by the Composite PMI Output Index, a survey-based measure of GDP. While the momentum eased for the second consecutive month, Chris Williamson, chief business economist at S&P Global Market Intelligence, notes that “Further robust growth of output in September rounds off the best quarter so far this year for US businesses.”

There has been a resurgence of recession predictions recently, driven by significant shifts in macroeconomic conditions. The year has seen a surge in uncertainty regarding what these changes mean for the economy. Some analysts are sounding alarms that the current economic expansion may be nearing its end. However, a thorough examination of a broad array of indicators suggests that it may still be too early to conclude that more than a slowdown in growth is imminent.

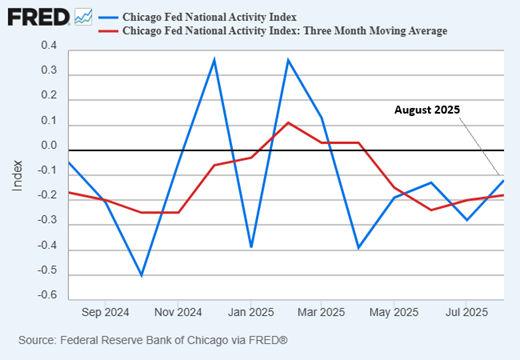

The US economic landscape showed signs of improvement in August, according to the Chicago Fed National Activity Index. Even though the output fell short of expectations, this monthly report represented the strongest performance since March.

Throughout much of the year, larger companies have outperformed their smaller counterparts in terms of market performance. However, the smallest firms (micro-caps) are now positioning themselves as serious competitors against the industry leaders (mega-caps) for year-to-date performance, as demonstrated by a selection of ETFs through the market close on September 19.

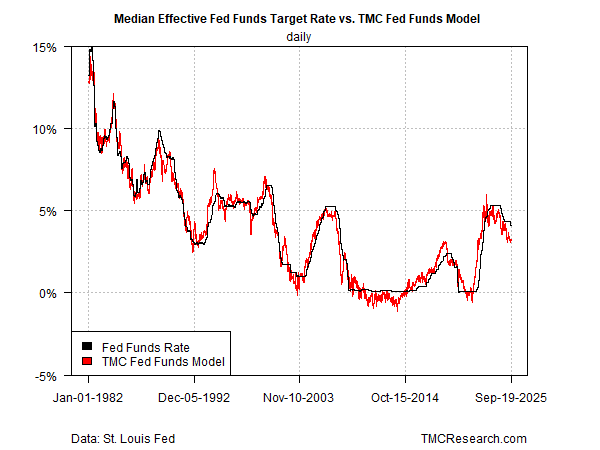

Markets are signaling potential cuts in Federal Reserve rates. Following last week’s interest rate reduction by the Fed, Fed funds futures suggest a high probability that the central bank will further ease monetary policy in its next two policy meetings of 2025. The 2-year yield is currently trading significantly below the target-rate range, reflecting expectations for additional cuts. Furthermore, TMC Research’s Fed funds model indicates that current policy remains moderately restrictive, suggesting that further easing is likely.

● How Progress Ends: Technology, Innovation, and the Fate of Nations

● How Progress Ends: Technology, Innovation, and the Fate of Nations

Carl Benedikt Frey

Review via Publishers Weekly

In this insightful study, Oxford economic historian Frey (The Technology Trap) explores how bureaucratic resistance and corporate monopolies can hinder technological advancement. He traces the history of technology from ancient civilizations to the present, examining systems that foster innovation. One model involves a centralized government imposing change from above, while the other encourages a decentralized approach, reminiscent of the U.S. during the Industrial Revolution, where inventors can secure funding for experimental ventures. Frey contends that Silicon Valley’s success in the digital age stems from its synergy of startups and venture capital, while he sees China’s rise as a blend of capitalist enterprises and a strong state. He expresses concern about the future of innovation in both nations.

In what has been a turbulent year for the fixed-income market, corporate bonds have risen to the forefront, becoming the standout performers in the asset class for 2025, based on a set of ETFs through the close on September 18.

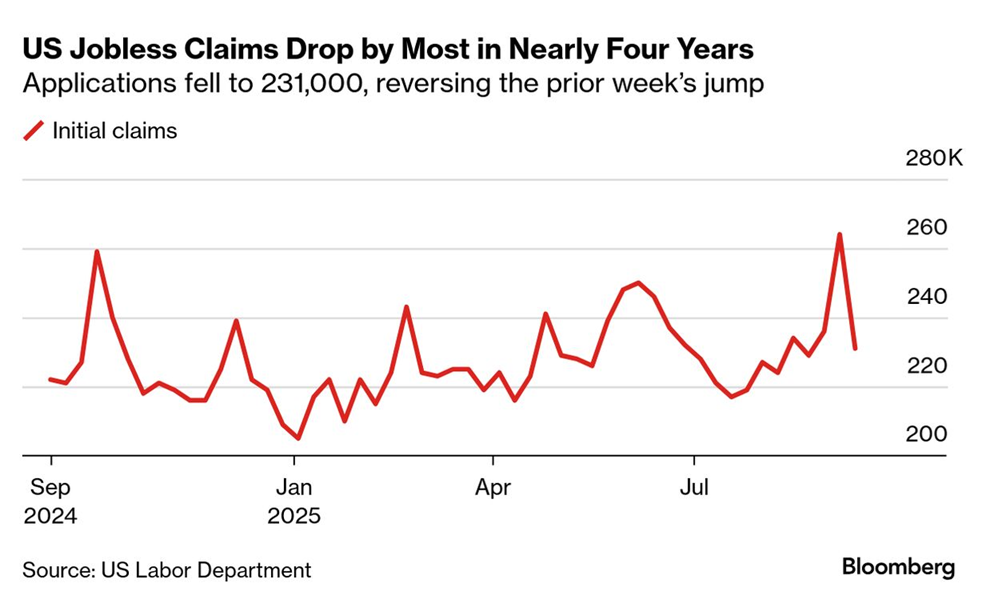

There was a significant drop in US jobless claims, reversing the previous week’s surge that pushed new unemployment filings to a four-year high. “This decrease is particularly noteworthy as claims in Texas, which had previously contributed to the spike, have declined, although they still remain high,” stated Nancy Vanden Houten, lead US economist at Oxford Economics. “When looking beyond the noise, initial claims continue to align with a relatively low rate of layoffs.”

Thank you, sir, may I have another?

This has become the prevailing sentiment in the markets following the Federal Reserve’s anticipated ¼-point reduction of its target rate, announced on Wednesday. Despite a rise in key Treasury yields, indicating some concern about rate cuts amid increasing inflation well above the Fed’s 2% target, market indicators still suggest that the Fed will pursue further easing. The primary factor driving this decision is a decelerating labor market, which the central bank currently views as a more significant risk than rising inflation.

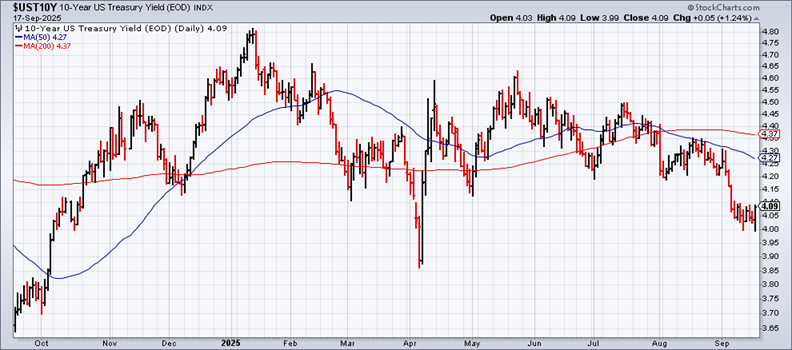

The US 10-year yield saw an uptick on Wednesday, coinciding with the Federal Reserve’s decision to lower its target rate. The central bank, as expected, reduced the Fed funds rate by ¼ point to a range of 4.0% to 4.25%. The 10-year yield momentarily dipped below 4.0% during the session but subsequently increased to 4.09%, marking the highest level since September 9.