More than seven years have passed since the UK seized Venezuela’s gold reserves.

Recently, Venezuela’s Interim President, Delcy Rodríguez, reached out through a letter to King Charles III of England, requesting the release of the Venezuelan gold reserves that have been held in the Bank of England for over seven years. In her correspondence, she emphasized the urgency of accessing these funds to support reconstruction efforts following the devastating earthquakes that struck last month.

“That gold belongs to our people,” Rodríguez asserted in her letter. “It is necessary to address the aftermath of the [June 24] earthquake.”

When the 31 tonnes of Venezuelan gold were confiscated in early 2019, its estimated value was around $1.9 billion. However, since then, gold prices have skyrocketed, more than doubling in value. Presently, those 31 tonnes are estimated to be worth approximately $4.06 billion.

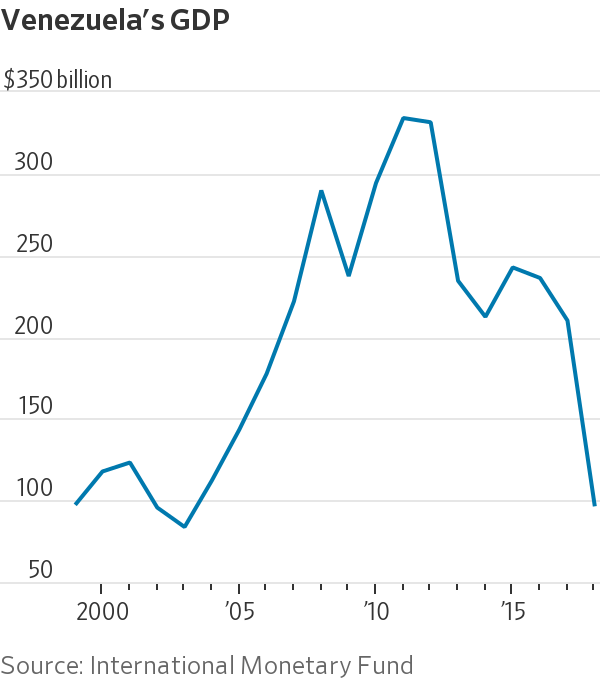

This is a significant sum for a nation grappling with its worst natural disaster in decades. Just prior, Venezuela endured one of the most dire economic contractions in peacetime history, as documented by Mark Weisbrot in an article for the Center for Economic and Policy Research (CEPR):

According to the International Monetary Fund, Venezuela’s GDP plummeted by 74% from 2012 to 2020. This loss of income is approximately three times greater than what was endured in the US during the Great Depression of the 1930s.

While the earthquake represents a natural disaster, this economic collapse was man-made. IMF data indicates that 88% of this economic decline occurred after the US imposed economic sanctions beginning in 2015. The situation deteriorated further with the sanctions introduced by the Trump administration in 2017, effectively isolating Venezuela from most international financial systems and reducing its foreign exchange earnings. Such pressures led to a severe crisis, showcasing the destructive potential of sanctions on a national economy.

The Wall Street Journal provides a visual representation of the significant damage caused by two main events: the 2014 collapse of oil and commodity prices and the subsequent US sanctions:

Since the US military intervention in Venezuela and the abduction of Nicolás Maduro on January 3, the country’s economic situation has worsened. Francisco Rodríguez, also from CEPR, estimates a mere 2.5% year-over-year growth in Venezuela’s economy during the first quarter, marking its weakest performance in years, despite a 25% increase in oil exports. This anomaly is largely due to the fact that a significant portion of these exports is not re-entering the Venezuelan economy.

The recent earthquakes have resulted in a devastating death toll of 3,800, with numbers likely to rise in the coming weeks. The UN estimates that the economic fallout could reach $37 billion, equivalent to 32% of Venezuela’s already struggling GDP.

President Rodríguez, facing dwindling popularity, is keen to access Venezuela’s sovereign funds to expedite reconstruction, stimulate economic activity, and restore educational services in affected areas. However, with most sanctions still in effect and US Secretary of State Marco Rubio wielding significant influence, such access remains uncertain.

In an article by the New York Times titled “How Marco Rubio Is Running Venezuela from Afar”:

Since the US forces captured Maduro from his residence in the early hours of January 3, Rubio has come to exert control over Venezuela as its de facto viceroy, a role not seen since Paul Bremer’s leadership in occupied Iraq in 2003.

Rubio plays a critical role in managing Venezuela’s finances, resource allocation, and governmental decisions. This influence extends despite his absence from the country, maintaining close relations with Delcy Rodríguez, who has taken the lead in the interim.

Yet, US interests aren’t the sole external factors at play.

For the first time since Hugo Chavez severed diplomatic ties and expelled the Israeli ambassador amid the Gaza War of 2008-09, Israeli officials and military personnel are once again present in Venezuela. This development reflects the broader implications of the US’s aggressive influence in Latin America—both through military interventions and engineered elections—as it paves the way for a reinvigorated Israeli presence in the region.

i24 News correspondent Amichai Stein reported that Delcy Rodriguez, Venezuela’s interim president, met with Israeli aid officials from the Foreign Ministry and military.

Delcy is acting president since the kidnapping of Nicolás Maduro… pic.twitter.com/pGNRgGOKRo

— The Cradle (@TheCradleMedia) July 8, 2026

Returning to the subject of the seized gold, the UK government decided to confiscate the 31 tons of Venezuelan gold in January 2019 after recognizing Juan Guaidó as Venezuela’s president. Prior to this recognition, the Bank of England had already denied the Maduro regime access to its gold, raising concerns about the legitimacy of Maduro’s election in late 2018.

Following Guaidó’s self-declaration of the presidency in Caracas, with Washington’s support, the UK began to assist Guaidó in his legal attempts to claim the gold stored at the Bank of England. However, Guaidó’s efforts ultimately failed because of legal challenges mounted by Venezuela’s legitimate government. Nonetheless, he managed to spend hundreds of millions of dollars of Venezuelan funds, seized by the US, which were made available to him.

To this day, Venezuela’s gold remains trapped in the vaults of the Bank of England—more than three years after Venezuela’s main opposition parties ousted Guaidó and terminated his parallel government.

According to UK Declassified’s article titled “Why Is Venezuela’s Gold Still Frozen in the Bank of England?,” published in January 2023:

The UK government has consistently maintained that Guaidó—rather than Nicolás Maduro—is the legitimate president of Venezuela. In this capacity, Guaidó’s legal team argued that he was authorized to act on behalf of the Central Bank of Venezuela and control the assets held in London.

During this period, Guaidó funded his UK legal battles using millions of dollars from Venezuelan assets that the US had seized. This situation highlights the irony of Guaidó attempting to claim Venezuelan state assets with resources that were stripped from the Venezuelan state.

Meanwhile, it appears that significant public funds were also utilized by the Foreign Office to maintain support for Guaidó.

Now that Guaidó has been removed from power, the legal basis for transferring the gold to the opposition has effectively collapsed. Despite this, the gold remains frozen at the Bank of England, with no clear resolution in sight.

This case serves as a precedent, potentially establishing a troubling practice where the UK can engage in asset appropriation from foreign states and transfer those assets to political factions involved in regime change.

This precedent could serve as a deterrent for any future state considering storing its assets at the Bank of England.

In fact, this has led to a rising urgency for foreign governments to reclaim their gold reserves stored abroad. As noted in a report from January, German economists and politicians have been increasingly vocal about the need to repatriate Germany’s gold reserves, many of which are held in the US and the UK. Notably, Germany had to endure a five-year wait to recover just 300 tons of its gold from the US Federal Reserve, and to date, has not received back any of the original gold bars it deposited.

This raises a significant question: Is Venezuela’s gold still truly secured in the Bank of England? Has it been sold, leased, or otherwise reallocated, a common occurrence with central bank gold? Given the long-standing manipulations within London’s gold market, the discrepancy between paper and physical gold markets, the lack of external audits akin to the Federal Reserve, and recent signs of shortages in London, there are no easy answers.

What is evident, however, is the lack of urgency from the Bank of England or the UK government to return Venezuela’s gold. In 2022, Delcy Rodríguez characterized the UK’s confiscation of Venezuela’s gold as “piracy,” condemning their actions as attempts to steal Venezuelan gold.

In January, BBC Mundo reported that the situation following the US’s abduction of President Nicolás Maduro and the appointment of Rodríguez as interim president has led to little change regarding access to these gold reserves (machine translation):

Does the recent upheaval in Caracas pave the way for the executive now led by Delcy Rodríguez to access the gold, which was valued at US$1.95 billion in 2020, now possibly worth US$4.4 billion due to rising gold prices? As of now, there are no indications to suggest this.

The case remains pending in the English courts, and as such, the gold is still in the Bank of England,” stated Sarosh Zaiwalla, founder of the law firm representing the BCV [Banco Central de Venezuela] and the Venezuelan government.

Following Rodríguez’s letter to King Charles, there seems to be increasing attention towards the issue.

British MP Richard Burgon has introduced an Early Day Motion (EDM) in the House of Commons demanding the immediate release of 31 tonnes of Venezuelan gold currently held by the Bank of England (BoE).https://t.co/JHza5CdLva

— Venezuelanalysis (@venanalysis) July 12, 2026

According to the aforementioned report from the pro-Chavista Orinoco Tribune, this motion, introduced on June 29, 2026, has garnered the backing of 30 MPs out of a total of 650. However, it remains unlikely that this will lead to significant policy changes or accelerate the legal process, which appears contingent on input from Viceroy Rubio.

Thus, the most accurate answer to the question posed in this article is: likely not. As with the US and EU showing no sign of returning $300 billion of Russia’s frozen assets, the City of London seems in no rush to return Venezuela’s gold, which may very well be out of their control already.

Venezuela’s situation is not just about the gold; it is also about the crucial foreign currency reserves of which the gold in the BoE comprises about 15%. Although the US has eased some restrictions on Venezuelan oil and certain state-owned banks, foreign financial institutions largely continue to withhold assets from the Venezuelan government.

This harsh climate of Western sanctions complicates the humanitarian efforts needed in the aftermath of the recent twin earthquakes. Over 100 economists and scholars—including Jeffrey Sachs, James K. Galbraith, Ann Pettifor, and Isabella Weber—have cautioned the US government in a letter:

“Regardless of one’s stance on Venezuela’s internal politics, the current array of coercive economic measures aimed at the country is overwhelmingly unjust. Sanctions affecting the central bank, public banking, the oil industry, and debt transactions disrupt payment systems, inflate import costs, obstruct banking relations, freeze assets, deter suppliers, and create scarcity for the entire population. This is precisely the moment to remove any economic or financial hurdles hindering relief and reconstruction efforts.”

The human toll resulting from the US sanctions against Venezuela escalates, now more than six months after US special forces captured Maduro, thereby replacing him with Delcy Rodríguez under pressured circumstances. Meanwhile, the growing fatalities from the US’s tightened siege of Cuba continue to unfold daily.

A 2025 study featured in Lancet Global Health, a leading medical journal, revealed that these extensive economic sanctions—deemed a less violent alternative to war—result in approximately 564,000 deaths annually, primarily among children under the age of five. In some years, this toll surmounts a million lives.

As previously addressed, respected studies have demonstrated that sanctions enforced by the US and EU since 1970 correlate with an estimated 38 million deaths—a staggering number overshadowing the effects of direct conflict—yet this truth often goes unreported in much of the Western media.

John Mearsheimer, a prominent scholar on international relations, didn’t overlook such findings. In an interview with Middle Eastern Eye, he provided a stark critique of US-led sanctions:

“America displays a profound ruthlessness. The scale of suffering we’ve inflicted worldwide is staggering… In places like Venezuela, Cuba, and Iran, we utilize our economic power to essentially starve people, compounding their suffering to spur them into revolt against their governments… Considering this, it becomes increasingly challenging to characterize the United States as a benevolent nation.”

🚨 BIG EXPOSE

A report by The Lancet states, “American sanctions from 1971 to 2021… have caused the deaths of 38 million people.” ~John Mearsheimer Critiquing US Foreign Policy. pic.twitter.com/5fadhlCZUz

— ✎𝒜 πundhati🌵🍉🇵🇸 (@Polytikles) March 13, 2026

[1] From Financial News:

Rehypothecation refers to the practice where one bank lends securities that have been pledged as collateral by its clients. In the US, rehypothecation is limited to specific asset types or amounts, whereas Europe lacks such restrictions.

Following the fallout from Lehman Brothers’ collapse, hedge fund managers discovered that assets they had pledged as collateral were entangled within the failed bank, often without their knowledge. The funds became inaccessible due to the rehypothecation practice, prompting significant liquidity challenges in the hedge funds.