Forecasting the Long-Term Equity Premium for Asset Allocation

Athanasios Sakkas (University of Nottingham) and Nikolaos Tessaromatis (EDHEC)

July 12, 2021

This study reveals that forecasting long-term equity premiums using a cross-sectional global factor model (CS-GFM) yields superior results—both statistically and economically—compared to traditional time-series prediction models frequently employed in both academia and industry. The CS-GFM forecasts provide noteworthy utility benefits when contrasted with long-term asset allocation strategies that depend on eighteen widely adopted prediction models, showing consistent efficacy across the US and ten developed equity markets.

* Catastrophic flooding in Germany has claimed at least 93 lives.

* The US is expected to issue warnings to companies regarding Hong Kong’s deteriorating situation, according to Biden.

* Treasury Secretary Yellen anticipates several additional months of rapid inflation.

* Despite elevated inflation rates, bond yields remain low due to liquidity, as noted by a bond manager interviewed.

* Corporate debt ratings are being upgraded at a rapid pace amid economic recovery.

* US industrial output increased by 0.4% in June, although the manufacturing component faced a decline.

* U.S. import prices registered another substantial increase in June.

* The automobile market remains robust as a computer chip shortage restricts supply.

* NY Fed Manufacturing Index surged to a record high in July.

* US jobless claims dropped to a new low since the pandemic began:

The recent uptick in the 10-year Treasury yield was viewed by some analysts as potentially signaling the end of its downward trend. However, trading this week, up to Thursday (July 15), indicates a different narrative.

In previous posts, I examined various basic approaches to estimating fair value for the 10-year Treasury yield, a useful proxy for anticipated returns. This time, I plan to extend that analysis to forecast performance for the US equity market over a decade, aiming to establish a foundational outlook for a 60/40 US stock/bond portfolio over a ten-year period.

* Fed Chairman Powell still anticipates a moderation in the current US inflation surge.

* China’s GDP increased less than expected in Q2, yet still showed strong growth at +7.9%.

* Covid-19 infections are rising sharply again across the US and Latin America.

* The US Senate has passed legislation banning imports of products from China’s Xinjiang region.

* Delta Airlines announced its first profit since the pandemic began.

* Low and declining yields have not dampened the junk bond market this year.

* US factory gate prices surged in June, exceeding expectations:

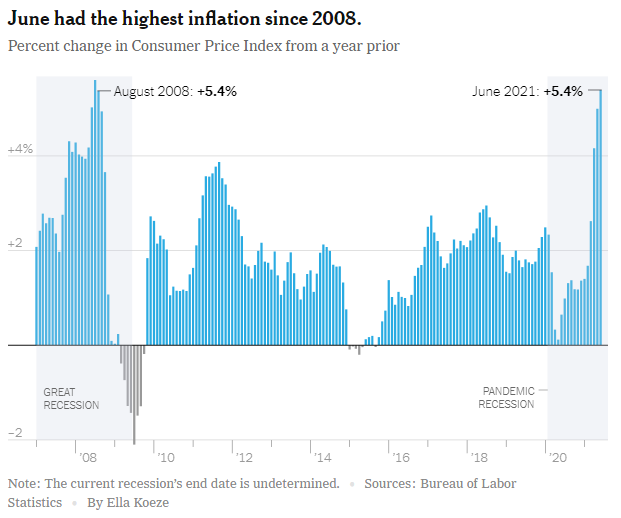

Consumer inflation in the US remained unexpectedly high in June, as reported by the Labor Department yesterday. At face value, these figures raise further questions about the Federal Reserve’s belief that the current inflation surge is temporary. However, a deeper analysis of the data presents a more nuanced perspective.

* Senate Democrats have proposed a $3.5 trillion infrastructure plan.

* US Covid-19 cases are on the rise again following months of decrease.

* The death toll continues to climb due to protests in several regions of South Africa.

* Global investments in Chinese stocks and bonds are still surging.

* US oil demand has rebounded to pre-pandemic levels.

* Europe is set to introduce proposals aiming to drastically reduce fossil fuel usage.

* US small business sentiment reached an eight-month high in June.

* Inflation in the UK rose to a three-year peak.

* US consumer inflation continued to accelerate in June:

Overall, global equity markets have performed well year-to-date, with the notable exception of China, based on data from US-listed exchange-traded products.

* Most regions of the country are experiencing a surge in Covid-19 cases due to variants.

* Biden expressed support for Cuban protesters, urging Havana to “listen to their people.”

* More Florida links have surfaced in the assassination of Haiti’s president.

* The pandemic has increased global government debt to its highest level since World War II.

* The International Energy Agency (IEA) predicts that oil markets will remain volatile following a breakdown in OPEC negotiations predicts.

* Microsoft has announced its acquisition of cybersecurity firm RiskIQ.

* ByteDance has indefinitely postponed its IPO plans following pressure from Chinese regulators.

* Index providers are considering the development of a comprehensive index.

* The Baltic Dry Index, a measure of shipping rates, remains near an 11-year high:

In the latest trading week (through July 9), diverse asset classes showed varied performance, as reflected by a series of proxy ETFs. US real estate investment trusts (REITs) stood out as top performers, while emerging market stocks and commodities faced significant setbacks.

In summary, the financial landscape over recent weeks has been characterized by critical developments and mixed signals across various markets. Notably, while many global equity markets are thriving, uncertainties remain, particularly in the context of inflation and economic recovery. Investors are encouraged to stay informed as these trends continue to evolve and influence future market performance.