In recent developments, several significant events have shaped the economic landscape:

- President Biden signed legislation to raise the US debt ceiling until December.

- Jerome Powell’s chances for a second term at the Federal Reserve are compromised but remain intact.

- Brent crude oil prices have surged past $85 a barrel, marking the highest level since October 2018.

- Microsoft announced plans to close LinkedIn in China due to stringent regulations.

- The United Auto Workers have initiated a strike at John Deere, the first in 35 years.

- US workers seem to be protesting against inadequate wages and working conditions.

- State-owned oil companies are compensating for reduced output from Western firms.

- The SEC is set to approve the first US bitcoin futures fund to begin trading.

- Prices received by US producers decreased in September.

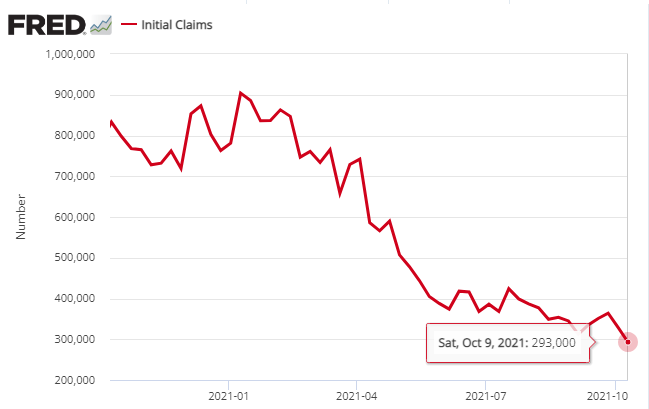

- US jobless claims dropped to a new pandemic low last week.

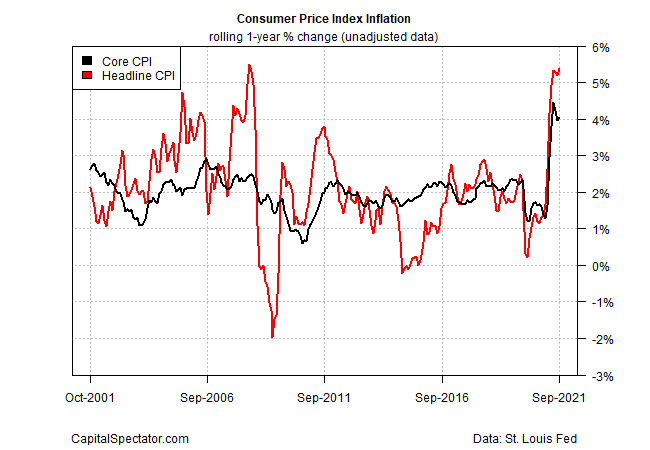

While inflation is no longer on the rise, it has yet to show definitive signs of declining from its recent highs.

Key highlights in recent economic news include:

- A gas shortage is expected to prompt power plants to switch from gas to oil.

- US home heating expenses are projected to rise significantly this winter, according to federal estimates.

- The Fed’s minutes indicate that a ‘gradual tapering process’ may begin as early as mid-November.

- A flatter yield curve between the 30-year and 5-year Treasuries signals increasing recession risks.

- Foreclosures are surging as COVID mortgage relief measures come to an end.

- China’s factory-gate prices reached a near-26-year peak in September.

- Chinese developers are facing exclusion from global debt markets following the Evergrande crisis.

- The Turkish currency has hit a record low after the president dismissed central bank leaders.

- US headline consumer inflation increased to 5.4% annually in September.

Last month’s fair value estimate for the US 10-year Treasury yield indicated a likely upward trend in this benchmark rate. As of now, this assessment appears to be accurate. The latest analysis continues to support the view that further increases in the 10-year rate are plausible.

Recent headlines include:

- The House approved a temporary increase to the US borrowing limit through December.

- The IMF has revised its growth forecasts downwards for both the US and the global economy.

- Global supply chain issues may worsen before they improve.

- The US will open its borders to vaccinated travelers from Canada and Mexico.

- China’s export growth was unexpectedly strong in September, as reported here.

- The UK economy continued its recovery in August.

- Eurozone industrial production declined in August amid ongoing supply disruptions.

- US small business sentiment decreased in September, falling well below its recent peak.

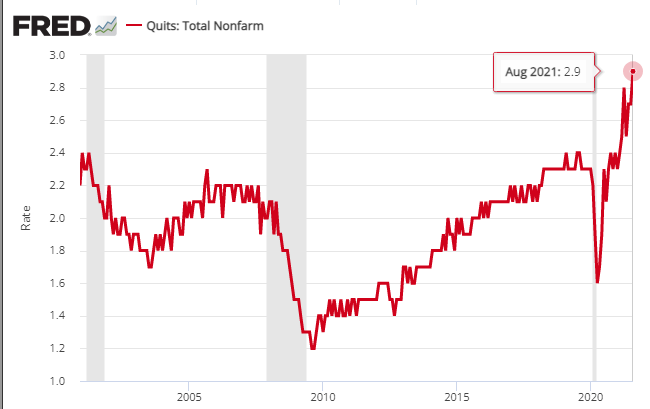

- A record number of US workers left their jobs in August.

While alternative energy sources hold great promise for the future, traditional energy isn’t fading away just yet.

The House is set to vote on the US debt-limit increase that was approved by the Senate last week.

- A global tax deal is facing uncertainty in the US due to a complex legal issue.

- JPMorgan’s Dimon forecasts that supply chain disruptions will ease soon.

- China’s financial sector is under increased scrutiny from the government.

- India faces a growing risk of an energy crisis.

- Microsoft reported that Iran allegedly hacked US and Israeli defense tech companies recently.

- South Korea’s central bank has maintained interest rates but signaled a potential hike in November.

- Three US economists were awarded the Nobel Prize in Economics.

- The US oil price benchmark has exceeded $80 per barrel, the highest since 2018.

In light of ongoing inflation concerns, commodity prices have seen considerable gains, achieving the strongest performance among various asset classes for the week leading up to October 8, according to a range of ETFs.

Current issues include:

- A global economic rebound is at risk due to supply chain bottlenecks, rising energy prices, and inflation concerns.

- Congress is facing a challenging autumn with vital legislation pending approval.

- China’s property bonds have dropped amidst default fears.

- The threat of inflation is increasing as energy prices rise.

- Analysts predict that the surge in corporate earnings has peaked recently.

- The port crisis in the US, linked to supply chain disruptions, shows no signs of improvement.

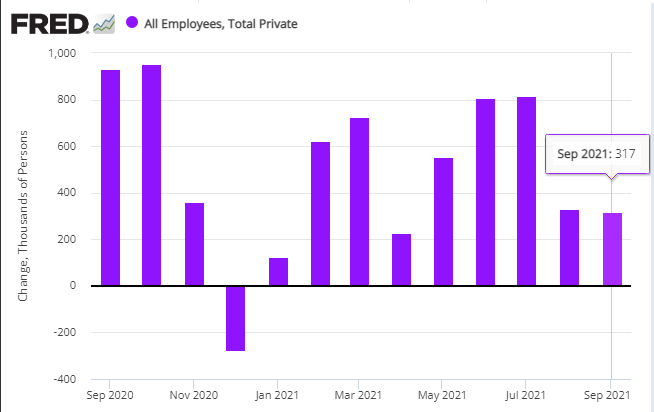

- US payrolls did not increase significantly in September as unemployment benefits were cut.

- US companies added fewer jobs than expected in September, close to August’s figures.

Stanley McChrystal and Anna Butrico

Summary via publisher (Penguin Random House)

Retired four-star general Stan McChrystal has experienced the severe risks associated with combat. From his early days at West Point to years spent in Afghanistan, and through his guidance of business leaders during global challenges, McChrystal has observed how individuals and organizations often struggle to manage risk effectively. This book proposes a battle-tested framework for identifying and responding to risk. Rather than merely predicting risk as a force, McChrystal highlights ten dimensions of control that can be adjusted at any moment. By closely monitoring these variables, we can cultivate a robust Risk Immune System that empowers us to anticipate, recognize, analyze, and act upon the inevitability of unexpected events.