In recent news, several economic developments have drawn attention. Here’s a brief overview:

- Expectations are low for the virtual meeting between Biden and Xi of China.

- Energy market disconnect may lead to shortages, according to IHS Markit’s Yergin.

- The US Dollar Index retreats after nearing a 16-month high.

- Will interest rates remain low indefinitely? Yes, predicts a manager at GAM Investments, as discussed here.

- China’s new home prices have witnessed their most significant decline since 2015, reports indicate.

- Economists in the UK anticipate that the Bank of England will raise rates in December.

- Japan’s economy contracted in Q3, declining more than expected.

- Rising inflation may enhance profits for certain companies.

- Gold has reached a five-month high amid rising inflation.

- Cargo demand is predicted to boost the aerospace sector, as per a Boeing executive’s forecast.

- The Consumer Sentiment Index in the US has dipped to its lowest level in a decade during early November.

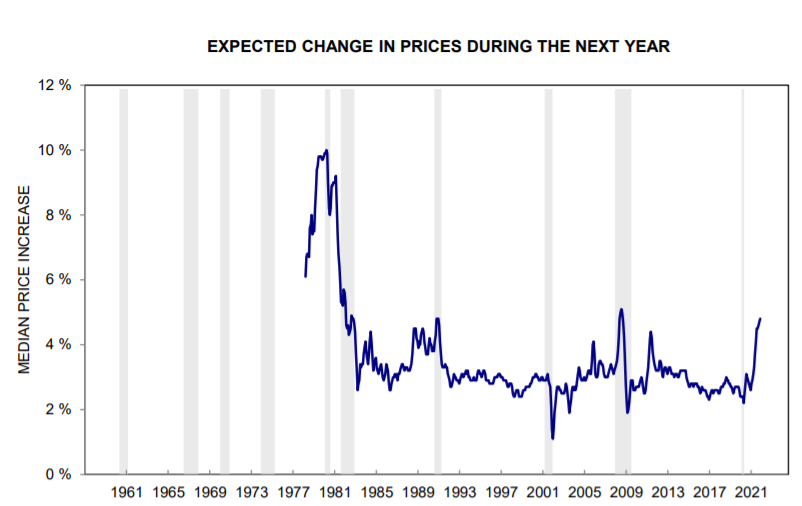

- Inflation expectations among US consumers for the next year have climbed to their highest in over ten years:

● The Generation Myth: Why When You’re Born Matters Less Than You Think

Bobby Duffy

Summary via publisher (Basic Books)

Many tend to categorize individuals based on their birth cohorts, but acclaimed social researcher Bobby Duffy challenges this notion. He argues that generational identities are not static; rather, they evolve throughout our lives. Duffy’s analysis of the beliefs of over three million individuals concerning topics such as homeownership and well-being suggests that the distinctions we often make between generations may be less pronounced than we think.

This year, energy stocks and commodities have seen a significant rally, yet they still feature prominently on our deep-value list, based on the relative rankings of around 150 ETFs.

Several key issues have emerged recently:

- Urgent action on climate change is demanded at the COP26 climate summit.

- Belarus has threatened to cut gas supplies to Europe due to a border dispute.

- The conflict at the Belarus-Poland border spilled over into UN discussions.

- Record-high job openings in the US have been reported, with job site Indeed noting a significant increase since June according to reports.

- Is the current inflation surge echoing the brief price spikes observed from 1946 to 1948?

- The White House has devised a strategy to mitigate inflation. Will it be effective, and when?

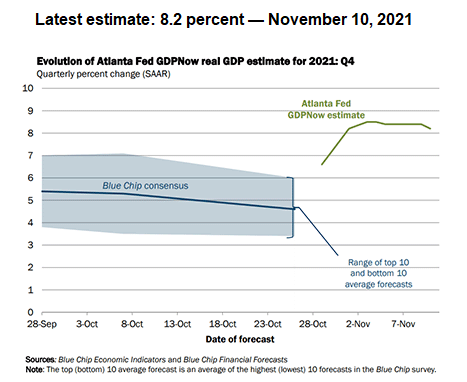

- Atlanta Fed’s GDPNow model projects a strong economic rebound in Q4:

The recent sharp slowdown in US economic growth during the third quarter, primarily driven by weakened consumer spending, took many economists by surprise. However, signs suggest a rebound in Q4 may be on the horizon. A significant factor behind this optimistic projection is the anticipated recovery in consumer spending, with next week’s retail sales update (scheduled for Nov. 16) likely to provide additional support for this expectation.

Recent highlights include:

- The US and China jointly announced a climate agreement at the COP26 summit.

- The recent uptick in US inflation increases the likelihood of an interest rate hike.

- The US dollar reached its highest point of the year against the pound and euro on Thursday.

- When adjusted for inflation, US wage increases in October have been negated.

- Financial institutions may become new targets for climate-related litigation.

- Belarus’s president has threatened to cut gas supplies to the EU amidst a border crisis.

- The UK’s GDP growth slowed during Q3.

- US jobless claims dropped once again last week, marking another low since the pandemic began.

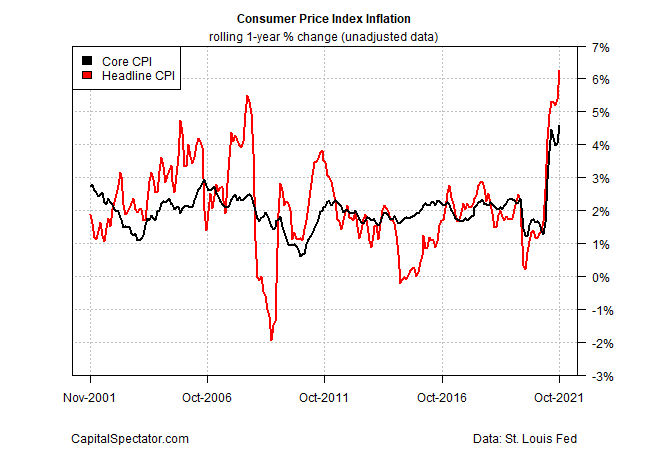

- US consumer inflation accelerated in October, reaching its highest levels in 30 years:

In the first article of this series, we discussed a foundational method to identify outliers—extreme data points—within a time series, focusing on the technique of dividing data into quartiles and using the interquartile range (IQR) to establish a definition of “normal.” While this approach is beneficial, it may not always suffice. Fortunately, there are alternative methodologies available for additional insights. For comparison purposes, let’s delve into one method and explore the evaluation of outlier risk using Z-scores.

Key points from recent economic updates include:

- St. Louis Fed President James Bullard forecasts two rate hikes in 2022.

- General Electric announced its intention to split into three separate companies.

- American households are presently carrying unprecedented levels of debt.

- China’s producer-price inflation surged to a 26-year peak in October.

- Economic advisors to the German government revised the growth forecast downward.

- Fed Governor Brainard had an interview at the White House as a potential replacement for Powell.

- The 30-year US Treasury yield fell to 1.79%, the lowest since July.

- Small business sentiment in the US declined in October, hitting its lowest point since March.

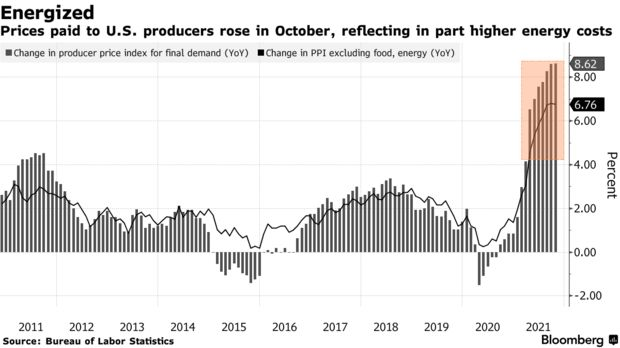

- US producer-price inflation remained stable at 8.6% year-over-year, the highest since 2010:

Anyone seeking definitive signs that inflation is subsiding as indicated by tomorrow’s CPI report for October (set for release on Nov. 10) may find little to support their hopes.

Recent updates highlight various pressing concerns:

- China’s real estate troubles may impact the US financial system, as warned by the Fed.

- Goldman Sachs projects that US inflation will continue to rise before eventually peaking.

- Negative real interest rates persist across developed economies.

- The migrant crisis intensifies on the Poland/European Union border.

- Surging heating costs pose a risk of continued inflation this winter.

- Global investments in Chinese stocks and bonds increase despite ongoing regulatory crackdowns.

- Tesla’s remarkable run has created challenges for fund managers who missed the rally.

- Bitcoin and ether have reached new historic highs.

- The Covid recession was notably unique — truly unusual.

- The 30-year Treasury yield is approaching a four-month low ahead of tomorrow’s inflation report:

Overall, the economic landscape is marked by fluctuating consumer sentiment, inflationary pressures, and significant geopolitical developments. It remains to be seen how these factors will evolve in the coming months.