Current developments are signaling that the global energy crisis may worsen, as warned by the IEA. Meanwhile, the strong U.S. dollar is predicted to impact corporate profits negatively. Despite the tumultuous market conditions, dividend payouts are on course to hit another record this quarter. However, sentiment among U.S. small businesses has reached a 48-year low. Questions are also being raised about the economic implications of abortion bans in various states. Additionally, the recent collapse of a large crypto hedge fund highlights concerns regarding counterparty risks. Homebuyers in America are canceling deals at the highest rate since the onset of the pandemic, and notably, the U.S. Dollar Index has surged to a new 20-year peak:

U.S. stocks maintained a narrow trading range last week, achieving a slight increase. In contrast, the majority of global markets faced declines during the trading week ending July 8, as indicated by various ETFs.

* Ukraine experiences intensified shelling from Russia.

* Russia has temporarily halted gas supplies to Europe through a major pipeline.

* President Biden’s visit to the Middle East is facing numerous challenges.

* The emergence of a new coronavirus variant raises alarms among scientists.

* Texas is vulnerable to rolling blackouts amid a heatwave.

* Analysts speculate on how the UK economy might transform with Johnson’s departure.

* In China, hundreds of depositors peacefully protesting were violently dispersed.

* While the U.S. job market remains robust, small businesses are struggling.

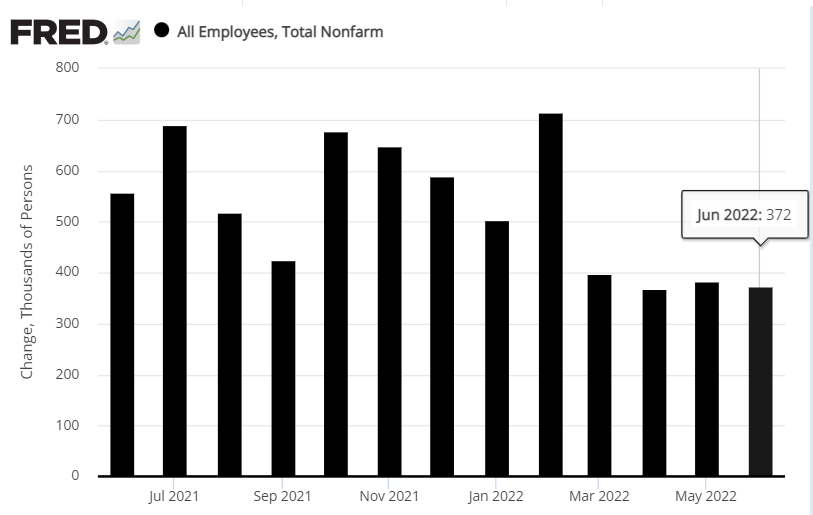

* U.S. payrolls are consistently increasing at a healthy rate in June:

● Cloudmoney: Cash, Cards, Crypto, and the War for Our Wallets

Brett Scott

Reference via New York Magazine

In the fast-evolving landscape of digital payment, convenience reigns supreme. Yet, this ease often comes with hidden costs. In “Cloudmoney: Cash, Cards, Crypto, and the War for Our Wallets,” journalist and former derivatives broker Brett Scott presents a compelling case that we all have a stake in the ongoing battle against cash. He critiques the push towards fully computerized transactions and a future that forsakes cash, arguing that a cashless society could inadvertently marginalize certain groups.

Investing in Deflation, Inflation, and Stagflation Regimes

Guido Baltussen (Erasmus University Rotterdam), et al.

July 2022

This research examines the performance of asset classes and factor premiums amid various inflationary conditions. Utilizing a comprehensive dataset dating back to 1875, it highlights that moderate inflation periods yield higher returns across both asset classes and factors. While deflationary phases see low nominal returns, real returns can still be appealing. Conversely, periods of high inflation and stagflation typically yield negative real returns for equity and bonds. However, during these challenging times, positive factor premiums can provide a buffer against some of the real capital losses.

* Former Prime Minister of Japan, Abe, was assassinated while giving a speech.

* Boris Johnson stepped down during a critical time for the UK economy.

* Putin asserts that Russia’s conflict with Ukraine is just beginning.

* The U.S. trade deficit decreased for the second consecutive month in May.

* Mortgage rates dropped for the second week, marking the largest decline since 2008.

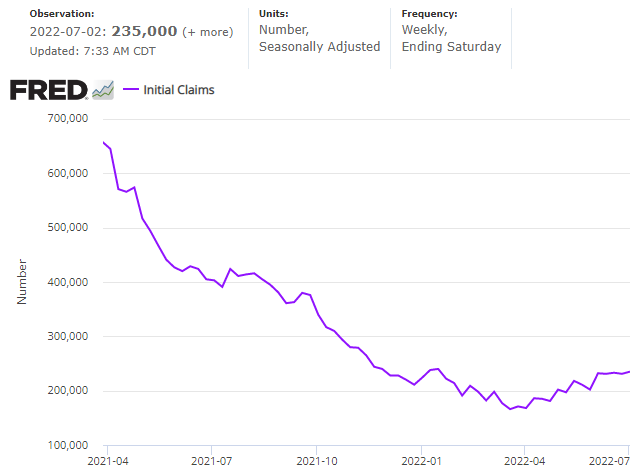

* Jobless claims in the U.S. remain low and stable, indicating a strong labor market:

A prevailing risk-off sentiment continues to shape market dynamics. Essentially, there has been little change in comparison to recent trends.

* Boris Johnson is set to resign as the Prime Minister of the UK amid growing scandals.

* Expectations are building for another 75-basis-point rate hike during the upcoming Fed meeting.

* Insights from Fed minutes highlight the focus on combating inflation.

* Growth within the U.S. services sector has slowed to a two-year low.

* Mortgage demand is decreasing despite falling mortgage rates.

* The Euro continues its descent towards parity with the dollar.

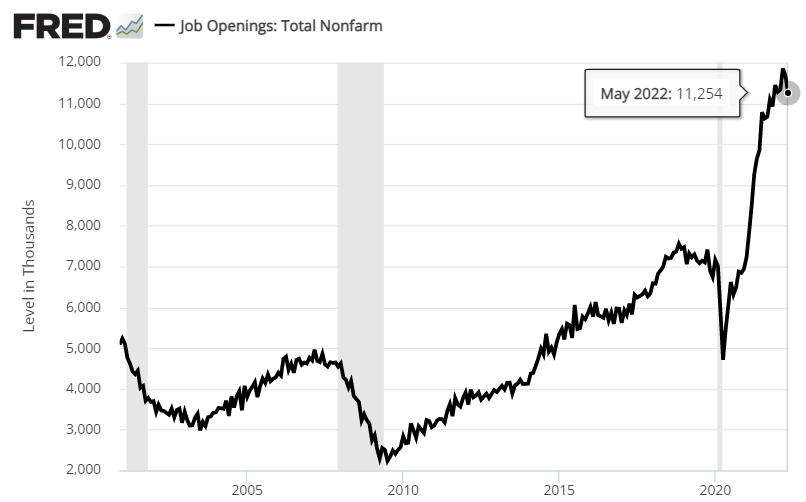

* Job openings in the U.S. declined in May, yet still outnumber available workers two-to-one:

The estimated risk premium for the Global Market Index (GMI) has shown signs of gradual easing. The updated long-term forecast suggests an annualized return of 4.9%. This estimate reinforces the need to lower expectations for globally diversified multi-asset-class portfolios in comparison to the returns experienced in previous years.

* The leadership of UK Prime Minister Johnson is in jeopardy as scandals accumulate.

* Demand for U.S. workers remains strong, according to private-sector reports.

* New COVID outbreaks in China have placed millions under lockdown.

* Observers are keen to see if today’s release of Fed minutes indicates support for another 75-basis-point rate hike.

* A recent Fed study found that the U.S. dollar’s global status remains strong and unchallenged.

* Chinese automaker BYD has surpassed Tesla to become the world’s largest electric vehicle manufacturer.

* Oil prices dropped below $100 for the first time in nearly two months.

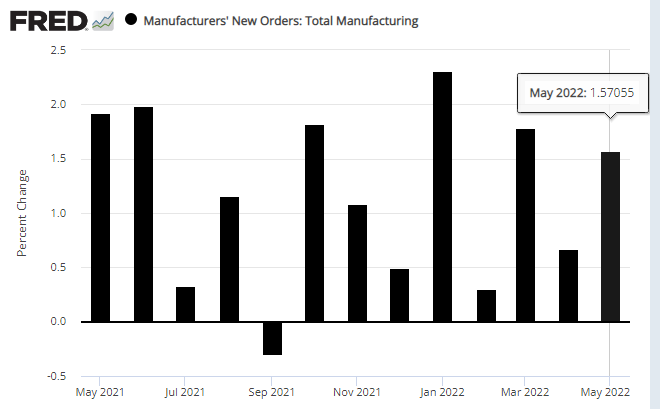

* U.S. factory orders increased more than anticipated in May:

Conclusion:

In summary, current global economic dynamics reflect a complex interplay of challenges and uncertainties, from energy crises to political instability. Stakeholders must stay informed and adaptable as the markets continue to navigate these turbulent times.