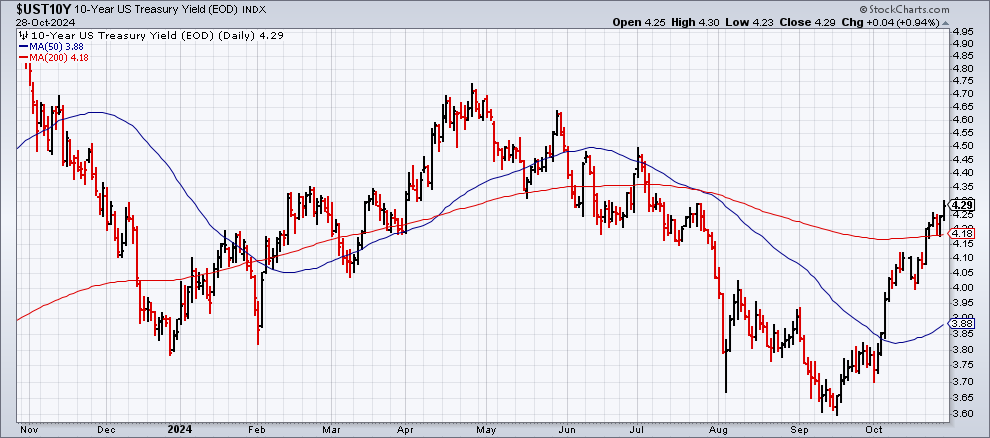

The yield on 10-year US Treasury bonds climbed to 4.29% on Monday, reaching its highest point since July. According to Tom Essaye, founder of Sevens Report Research, “If the economic data this week, particularly Friday’s jobs report, shows strength, expectations for a rate cut in November could diminish significantly, which might lead to increased volatility in the markets. Ultimately, maintaining a ‘Goldilocks’ data environment is crucial this week to ensure stable rate cut expectations.” Read more here.

The final week before the US elections is filled with essential economic reports. As a result, the chances of surprises that might influence voter perception are heightened in the coming days. Here’s a brief overview of this week’s important releases.

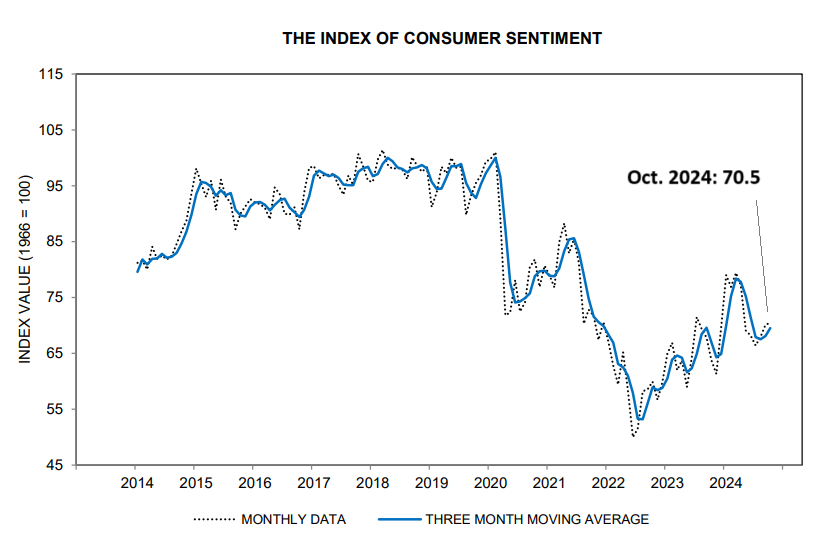

US consumer sentiment rose for the third consecutive month in October, as reported by the University of Michigan’s survey data. The university’s widely followed sentiment index increased this month, reaching its highest level since April. Joanne Hsu, Director of Surveys of Consumers at the university, states, “This month’s improvement was largely driven by slight enhancements in purchasing conditions for durable goods, partly attributed to lower interest rates.”

The Capital Spectator will be traveling for the next several days. Regular postings will resume on Monday, October 28. Cheers!

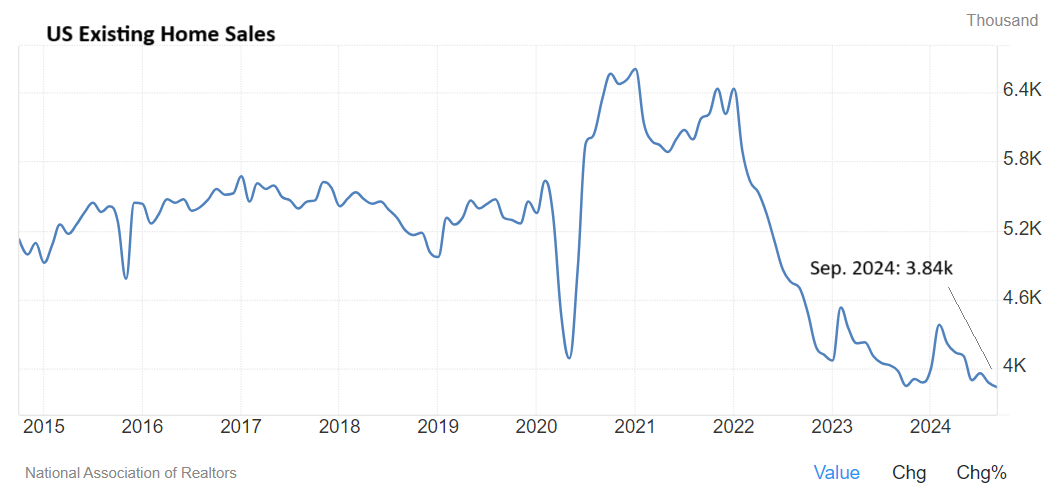

US existing home sales plummeted to a 14-year low in September. Lawrence Yun, Chief Economist at the National Association of Realtors, remarks, “Factors that typically drive higher home sales—such as significantly lower mortgage rates compared to a year ago, increasing inventory, and ongoing job growth—have not translated into improved home sales, which remain sluggish.” In stark contrast, sales of new homes have been on an upward trend in recent years.

How will the recent hurricanes that impacted the Southeast US affect the upcoming third-quarter GDP data? While the overall impact is expected to be minimal at this time, forecasts compiled by CapitalSpectator.com suggest some effects may be felt.

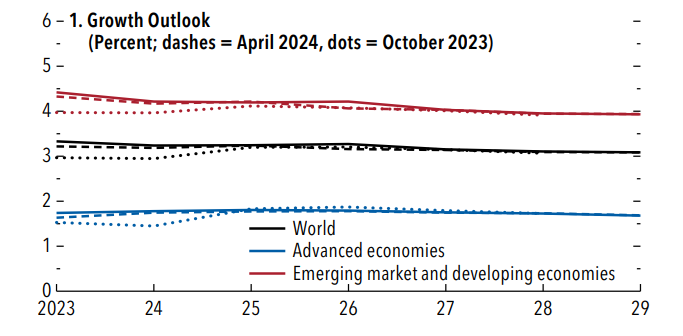

The IMF has projected that the US economy will continue to be a significant driver of global growth through 2025, as outlined in their latest World Economic Outlook report. The IMF has raised its growth forecasts for 2024 and 2025 for the US, contrasting with stagnant or slightly declining predictions for other developed nations. The IMF noted, “Global growth is anticipated to remain consistently low,” projecting a rate of 3.2% for both 2024 and 2025, which is almost unchanged from the estimates made in April and July of this year.

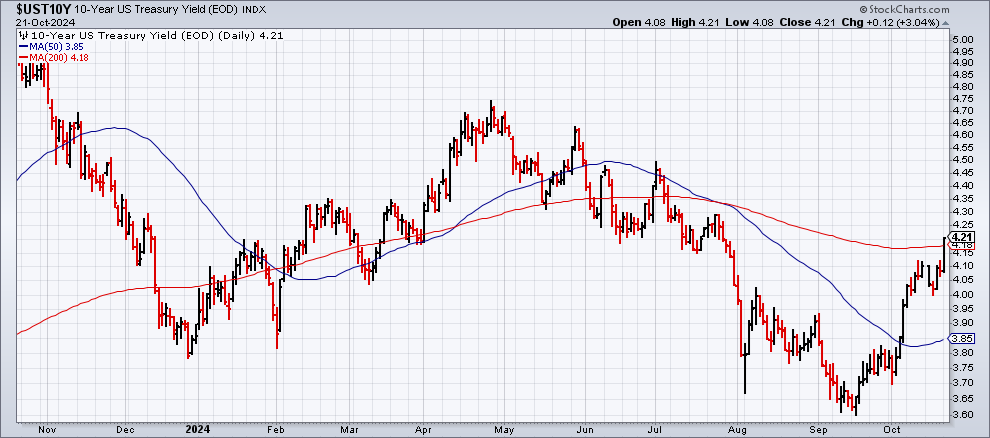

Will the bond market’s summer rally endure through the fall? New uncertainties are emerging as the market reassesses various risk factors, including increasing doubts regarding the Federal Reserve’s commitment to lowering interest rates.

The yield on US 10-year Treasury bonds increased to 4.21%, marking its highest level since late July. Robert Dishner, Senior Portfolio Manager at Neuberger Berman, comments, “With less than two weeks to go before the US elections, concerns regarding the fiscal outlook and its potential inflationary pressures are intensifying.”

The discussion around international diversification for US investors typically focuses on how to allocate global equities. However, the global bond market often takes a backseat in investors’ considerations. Given the performance of non-US bonds so far this year, strategists might feel inspired to reconsider this oversight.