The US economy is currently experiencing sluggish growth, a trend that may further deteriorate in the coming months. However, this slowdown has not yet raised significant recession alarms. While certain indicators, such as the inverted Treasury yield curve, might suggest otherwise, a comprehensive analysis of economic and financial data indicates a modest expansion, both recently and in the near future.

The Fed has decreased rates by 0.25 points, facing criticism from Trump: Politico

The Fed lost control of a key interest rate earlier this week: CNBC

OECD forecasts that global growth will slow to its lowest pace in a decade: WSJ

The US is consulting with Gulf allies on potential responses to the attacks on Saudi Arabia: Reuters

The UK Supreme Court concludes its hearing against the prime minister today: Reuters

A former Fed official claims that uncertainty from the trade war, not tariffs, is affecting the economy: CNBC

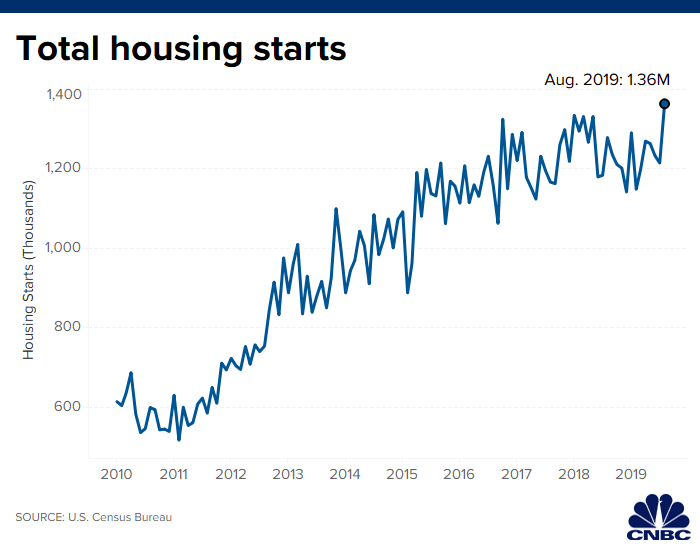

US housing starts saw a rise to a twelve-year high in August: CNBC

The average reader of economic reports might be inclined to view the recent uptick in recession indicators as uniform. However, the reliability and quality of such assessments can vary widely. It’s crucial to understand the fundamental principles behind the differing interpretations of business cycle trends.

The Fed is anticipated to lower rates today for the second time this year: WSJ

Saudi Arabia is expected to provide proof linking Iran to recent attacks: Reuters

Saudi Arabia assures that oil exports will continue as usual: Bloomberg

Elections in Israel, the second in five months, result in a deadlock: BBC

An economic crisis looms for Latin America: NY Times

Eurozone inflation remains stable in August, reaching its lowest level in nearly three years: Reuters

UK inflation has dipped to the slowest rate since 2016: Bloomberg

US manufacturing activity showed signs of recovery in August, according to the Federal Reserve: CNBC

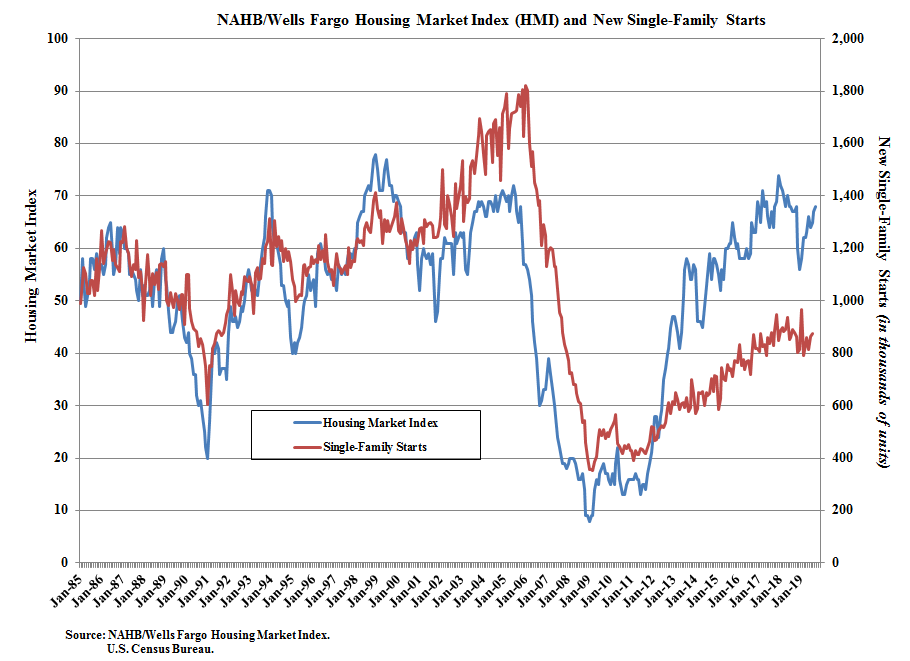

US homebuilders maintain a positive outlook in September regarding housing: NAHB

September has proven to be advantageous for undervalued stocks, leading investors to speculate whether this long-neglected segment of the US equity market might finally outperform its growth-focused counterparts. While a few weeks is hardly an accurate indicator, the anticipation continues to build.

The attack on oil facilities introduces fresh uncertainty into the global economy: CNN

The oil market is evaluating the impact of the attacks on Saudi production: NY Times

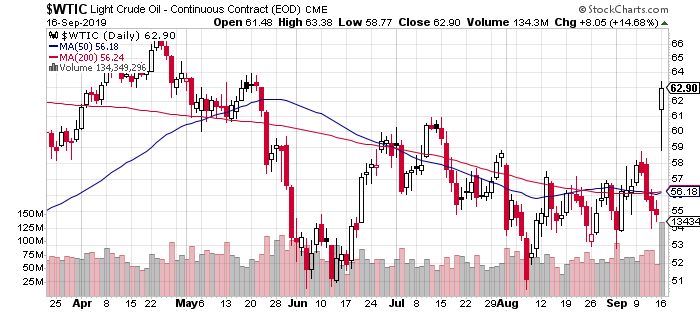

Oil prices are retreating after Monday’s spike: Reuters

US gasoline prices are expected to rise following the surge in oil prices: Bloomberg

Iran’s supreme leader claims the nation will never negotiate with America: CNBC

The Fed is divided but anticipated to cut interest rates this week: Reuters

Israelis head to the polls today for the second time in five months: Politico

German economic sentiment improved in September after a sharp decline: Investing.com

The NY Fed Manufacturing Index indicates sluggish growth in September: NY Fed

Oil prices spiked on Monday following the attacks on Saudi Arabia: CNBC

Non-US equities displayed the strongest gains last week among major asset classes, as measured by a selection of exchange-traded funds. However, the surge appears to have receded following the weekend attacks on Saudi oil-production facilities.

Oil prices skyrocketed after the attack on Saudi oil facilities: Reuters

The US economy is largely insulated from the consequences of the Saudi oil attack: WSJ

Trump states the US is ‘locked and loaded’ following the attack on Saudi oil supplies: CNBC

The United Auto Workers union has initiated a strike against GM: CNN

China’s economic growth continued to decelerate in August: Bloomberg

Johnson is set to inform the European Commission that the UK will not delay Brexit past October 31: BBC

The incoming ECB chief will likely maintain the ultra-loose monetary policy: Bloomberg

US import prices fell sharply in August: MW

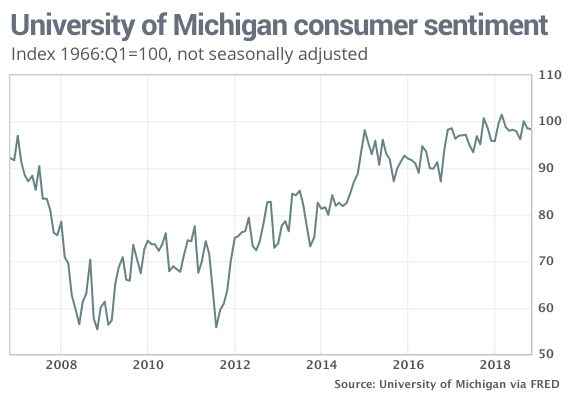

US consumer sentiment saw a moderate rebound in September: UoM

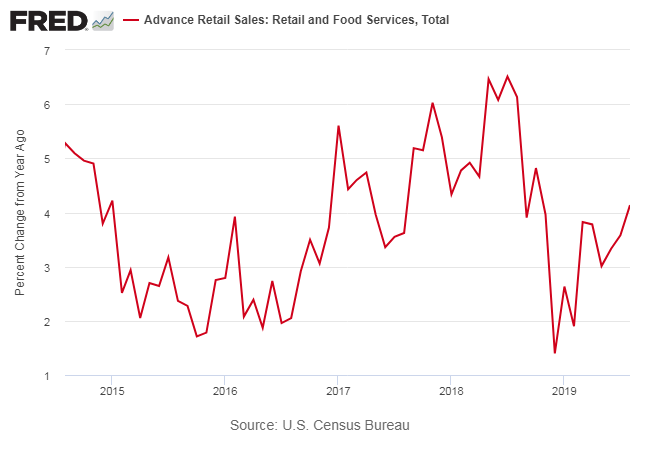

US retail sales increased to a +4.1% annual rate in August: CNBC

● The Case For People’s Quantitative Easing

By Frances Coppola

Review via Brave New Europe

This book argues that although the quantitative easing adopted since the Great Financial Crisis of 2007/08 has not succeeded, the failure lies in its implementation rather than the policy itself. The concept, introduced by Milton Friedman and Ann Schwartz in 1963 as a remedy for a financial downturn, suggested drastically increasing the money supply to empower consumers and revive the economy. Friedman metaphorically illustrated this idea with a helicopter dropping money directly into communities. However, following the Great Financial Crisis, central banks globally initiated a massive “helicopter money” strategy by dispensing trillions of dollars. Coppola explains that the “Great Experiment” of quantitative easing fell short because it involved recklessly distributing money onto global financial markets without carefully monitoring its impact. Thus, rather than achieving the anticipated economic stimulus, we find ourselves in a protracted period of stagnation.

Continue reading

Just as inflation seemed to decrease, the latest consumer price report for August issued a surprising alert. The core Consumer Price Index (CPI), excluding food and energy, increased by 0.3% last month, reaching a 2.4% annual rate—the highest in 11 years. While a single data point does not indicate a trend, this release stands out at a time when the US economy is grappling with slow growth and expectations for potential interest rate cuts, possibly even negative rates.

In summary, while the US economy faces challenges such as slow growth and inflation pressures, there remains a cautiously optimistic outlook based on various indicators. Investors and markets should continue to monitor these trends closely to navigate the complexities of the economic landscape in the months ahead.