In today’s rapidly shifting financial landscape, significant concerns have emerged regarding lending practices and market stability. The Financial Times highlights this with the article Top US financiers sound alarm on lending standards, which conveys a cautious stance, suggesting that while mistakes have been made, catastrophic outcomes may not be imminent. This piece reflects ongoing warnings about risks present in US equity markets.

While I refrain from offering financial advice or predictions, it is clear that many markets appear to be mispriced, leading to dubious risk/return dynamics for long positions.

Evaluating the current economic environment is notably more complex than in the lead-up to the 2008 crisis, where risky US mortgage loans and derivatives were at the forefront. During that period, there was substantial clarity about the underlying loans—evidenced by analysis from CoreLogic detailing subprime mortgage resets, which I argued would lead to adverse outcomes.1 My assessment, which contradicted the prevailing view, ultimately proved accurate.

Today, discerning the current financial situation is challenging due to a lack of transparency and the myriad of asset types now involved, as well as a multitude of international factors. For example, in 1987, analysts were largely focused on the speculative bubbles in Japan, unaware that a US crash was on the horizon. Presently, the fundamentals in Europe are deteriorating, yet we witness a surprising resilience in the euro and European stock markets, likely fueled by optimism surrounding military Keynesianism. This optimism exists despite ongoing political uncertainty, with a lack of governance in France and low approval ratings across leaders in Germany, Italy, and the UK.

The current landscape is further complicated by the absence of an engaged econoblogosphere similar to what existed prior to the Lehman Brothers collapse. In those days, a vibrant community comprising voices like Tanta from Calculated Risk, Ed Harrison, Felix Salmon, Barry Ritholtz, Nouriel Roubini, and Paul Krugman actively debated and analyzed emerging trends. Today, this crucial dialogue seems diminished.

Analogies to past crises, such as the savings and loan disaster that concealed additional turmoil in leveraged buyouts, serve as a reminder that historical comparisons may overlook vital aspects of today’s realities. One colleague managing workouts at GE had designated two conference rooms for his operations, dubbing them Triage and Don Quixote, illustrating the layered complexities of financial challenges during prior crises.

The overarching takeaway is that drawing parallels to historical events may obscure crucial elements in the current landscape. We now face a variety of challenges: the AI/tech bubble linked to questionable lending practices, risks in the private debt market, substantial leverage within private equity due to “subscription lines of credit,” political divisions across Western nations, and economic instability that could spill over from Europe and China—where deflationary pressures are mounting. The scenario is hardly reassuring.

In a rare admission against the grain, financial leaders have voiced concerns about the decline in lending standards, hinting at potential adverse outcomes. The conventional pattern during bull markets suggests that the frenzy often escalates until the last skeptic capitulates. Past bubbles, such as the dot-com era, demonstrate that markets can continue to surge to alarming heights before eventual corrections occur.

As we turn our attention back to the recent alarms raised by financial executives regarding debt, the Financial Times reports:

Top US financiers have warned of an erosion in lending standards after credit markets were shaken by the collapse of First Brands Group and Tricolor Holdings.

Apollo Global Management chief executive Marc Rowan indicated that the unraveling of these businesses followed a lengthy period during which lenders sought riskier borrowers.

The failure of First Brands and subprime auto lender Tricolor has reverberated through credit markets, resulting in substantial losses for investors including Blackstone and PGIM, as well as major banks like Jefferies.

This situation has increased scrutiny surrounding the private capital industry, particularly regarding the opacity of borrower profiles, characterized by high leverage.

“In some of these more levered credits, there’s been a willingness to cut corners,” Rowan noted at a Financial Times Private Capital Summit in London.

Both Rowan and Blackstone president Jonathan Gray pointed to banks for taking on exposure to First Brands and Tricolor, yet asserted that these failures do not indicate a systemic issue. Gray dismissed the notion that this event could serve as a “canary in the coal mine,” stating that both instances were driven by bank-led processes.

Recent years have witnessed ongoing tensions between banks and private capital firms, as organizations increasingly turned to private credit for financing. Traditional lenders have criticized this trend as regulatory arbitrage, expressing concerns that non-bank financial institutions operate under looser regulations.

However, the collapses of First Brands and Tricolor underscore how entwined these financial sectors are, complicating the identification of underwriting risk amid that ambitious quest for market share.

JPMorgan Chase chief executive Jamie Dimon echoed similar sentiments, expressing his unease during the bank’s earnings report, marred by a $170 million loss stemming from Tricolor’s demise. “My antenna goes up when situations like this arise. I probably shouldn’t say this, but when you spot one cockroach, there are likely more lurking,” he remarked, adding that he perceived fraud as a factor in these situations, but did acknowledge the need for improved company procedures.

In a conventional sense, First Brands was involved in factoring—securing loans against receivables—a common practice in the garment sector. While it can signify a desire for high leverage or distress when exercised in an established context, First Brands availed itself of borrowing during a period of relaxed lending standards characterized by “cov lite” agreements, which typically have fewer protections for lenders.

Evidence suggests that First Brands may have engaged in double-pledging its receivables, an act that is criminal. In a parallel incident years ago, Ralph Esmirian, a respected figure in New York’s diamond industry, was prosecuted for selling collateral that had already been used to secure loans and also double-pledging after acquiring the esteemed jewelry retailer Fred Leighton. Esmirian received a six-year federal prison sentence. A recent Wall Street Journal article detailed the fallout from First Brands’ collapse:

[Patrick] James’s company, First Brands Group, has filed for bankruptcy, acknowledging that more than $2 billion is unaccounted for. Newly appointed directors are investigating irregularities in the company’s financial dealings, while the Justice Department has commenced an inquiry.

First Brands, of which James is the chief executive officer and sole equity owner, borrowed over $10 billion from prominent institutions despite facing lawsuits from business partners alleging misrepresentation in complex financial arrangements involving James. Major banks including UBS Group and Jefferies Financial Group are now at risk.

The company managed to raise billions through off-balance-sheet financing, significantly leveraging receivables owed to it by clients like AutoZone.

In theory, Jefferies, exposed to First Brands to the tune of $715 million via its Point Bonita fund, could absorb the entire loss. However, similar to past crises,2 pressure from investors who participated in the fund could compel Jefferies to make amends, leading to far greater consequences.

Shifting focus to recent stock market warnings, the Financial Times reports:

The leaders of Goldman Sachs, JPMorgan Chase, and Citi have cautioned investors that current exuberance might propel the recent rally in financial markets into bubble territory.

Goldman’s CEO David Solomon remarked: “There is no doubt that a considerable amount of investor exuberance is present, with US equity markets consistently reaching record highs in recent months.”

“Much of this has been driven by significant investment in [artificial intelligence] infrastructure, leading to substantial capital formation. However, history suggests that periods of widespread excitement around new technologies often result in a divergence wherein some ventures prosper while others falter.”

Jamie Dimon from JPMorgan added: “We have a plethora of assets that appear to be entering bubble territory. That said, they might still have another 20 percent to rise. Nonetheless, it’s a concerning indicator.”

Citi’s CEO Jane Fraser pointed out that the global economy has “proven more resilient than many anticipated,” in part due to investments in AI, while expressing that pockets of valuation excess exist in the market, prompting a hope for continued discipline.

Moreover, the related debt exposure linked to AI is substantial. As reported by Bloomberg on October 7:

The debt associated with artificial intelligence has surged to an astounding $1.2 trillion, now comprising the largest segment in the investment-grade market, according to JPMorgan. AI companies represent 14% of the high-grade market, an increase from 11.5% in 2020, surpassing US banks’ share of 11.7% in the JPMorgan US Liquid Index (JULI). Analysts identified 75 companies across various sectors closely linked to AI, including Oracle Corp., Apple Inc., and Duke Energy Corp. Many of these firms are prolific debt issuers, and in the case of the tech sector, they enjoy significant cash reserves with minimal net debt.

It is important to remember that investment-grade ratings are meant to signify security. Although there are mentions of AI-related junk debt, I have yet to find any aggregate estimates.

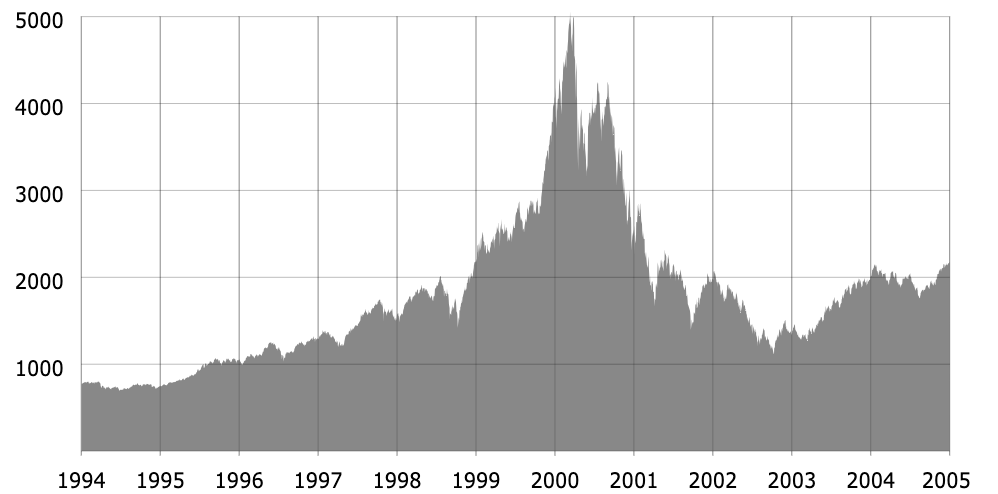

Even solely considering the frothiness of the stock market, we may be experiencing a bubble that rivals or even surpasses the dot-com era. There are others who share this sentiment. For instance, Mark Spitznagel of Universa Investments, who employs a hedging strategy inspired by Nassim Nicholas Taleb, predicts an impending blow-off top followed by an 80% market crash. Reportedly, he suggested we could see SPX soar to around 8000 before experiencing a massive downturn—though predicting precise figures is inherently uncertain. Thus, while getting in now might yield short-term gains, the risks of catastrophic loss loom large, especially if you fail to exit at the right moment. Spitznagel compared current conditions to the preceding situation in 1929, indicating an imminent euphoric peak followed by a severe crash. It’s crucial to remain rational and avoid succumbing to the pressure of fear of missing out (FOMO).

Even if the bubble bursts at its current levels, the repercussions on the real economy would be significant:

⚠️ This is truly INSANE:

US households now own a RECORD 52% of their financial assets in equities.

This share has more than DOUBLED since the Great Financial Crisis, surpassing the 2000 Dot-Com Bubble by ~5 points.

They hold just 15% in cash and 14% in debt assets. pic.twitter.com/6DRmtxYSze

— Global Markets Investor (@GlobalMktObserv) October 13, 2025

This concentration of holdings predominantly lies with wealthier households, who, for the past two years, have been pivotal in driving the economy as consumers. Therefore, any significant scaling back on their spending could result in even more pronounced effects.

For some time, I have noted concerns about deflation, especially given the evident trends in China, where deflation seems to be taking root and may spill over into international markets. Domestic real estate prices in China continue to plummet. The government has acknowledged an oversupply in critical sectors, particularly in electric vehicles, leading to intense price competition. While they are attempting to address the problem now, historical efforts to rationalize capacities have taken years to manifest. Furthermore, experts predict that the current overcapacity situation poses even greater challenges. Although China is increasing exports to Southeast Asia, this trend indicates weakness, not strength, with some aimed at re-exports to the US, being perceived as “channel stuffing.” In the US, we are already teetering on the edge of deflation—evident in stagnant wages in the casual labor market, minimal inflation rates, and official projections of only 0.5% to 1.0% inflation.

In addition to the deflationary impact of a significant market downturn, the implementation of tariffs is likely to compound the issue. While the initial phase of tariffs may induce inflation, as businesses absorb some costs, history suggests that the ensuing consumer and business spending reductions—akin to the effects of the Smoot-Hawley Tariff—could ultimately lead to a deflationary scenario. Lacy Hunt argues that the current combination of tariffs and liquidity shortages in international markets is triggering a deflationary debt spiral:

“The only other time this ever happened was between 1929 & 1930.”

Lacy Hunt sees a deflationary debt spiral unfolding now caused by tariffs & lack of liquidity in international markets.

This is how the Federal Reserve & President Hoover intentionally collapsed the system in 1929 https://t.co/5D925EiJ3l pic.twitter.com/KJVOn5vrop

— Financelot (@FinanceLancelot) October 9, 2025

While the outlook is daunting, with a lack of strong leadership in the Treasury and Trump prioritizing Fed dominance over sound policy, optimistic expectations for effective emergency responses amid potential downturns seem naïve. Vigilance is essential.

____

1 Not a joke. From the March 2007 post, quoting the Wall Street Journal:

[Author] Christopher Cagan, director of research at the real-estate-information concern [CoreLogic] based in Santa Ana, Calif., said those foreclosures are likely to occur over six to seven years and won’t be enough to damage the national economy.

2 This scenario transpired in connection with credit card receivables, which were explicitly classified as non-recourse to the seller. However, buyers subsequently pushed for some form of restitution, effectively saying, “We will not consider future deals without assurance.”