As we analyze the landscape of inflation indicators, we are faced with a multitude of tools to assess whether the anticipated inflation surge is simply a fleeting phase or a significant shift indicating prolonged price pressures. Recently, I examined some usual indicators, such as core inflation and the forecasts implied by the Treasury market, to help navigate this uncertainty. However, this is just the beginning. Among the alternative metrics available, the Treasury term premium stands out as particularly noteworthy.

* Germany opposes the U.S.-backed initiative to waive Covid-19 vaccine patents.

* Vaccines demonstrate encouraging results against COVID variants.

* The main opposition leader in India warns that India’s Covid wave threatens the global situation.

* The Biden administration is expected to uphold investment limits in China.

* China’s economic growth accelerated in April, marking its fastest rate in 2021 based on PMI data.

* China’s exports surged beyond expectations in April.

* The Fed cautioned about the risk of ‘significant declines’ in asset prices due to rising valuations.

* Chinese rocket debris is anticipated to impact Earth this weekend.

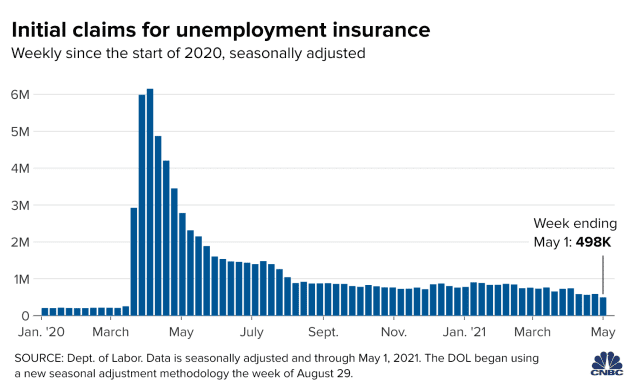

* U.S. jobless claims dropped below 500k last week, reaching a new pandemic low:

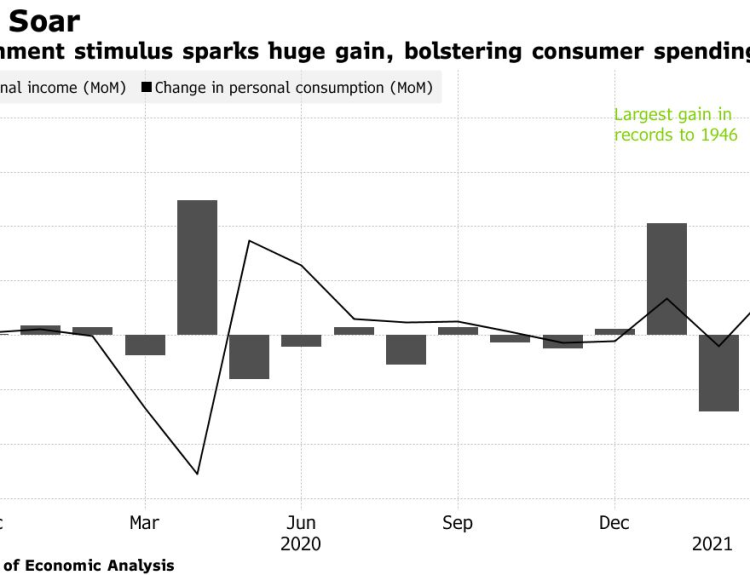

The U.S. economy gained momentum in the first quarter, and even more robust growth is anticipated for the April-through-June period, supported by various GDP nowcasts.

* The U.S. endorses a plan to waive intellectual property rules for vaccines.

* The Treasury Department urges Congress to increase the U.S. debt ceiling this summer.

* The world’s largest pension fund is reconsidering ESG investing approaches.

* An epic surge in lumber prices is adding approximately $36,000 to the cost of new homes.

* Global economic growth reached an 11-year high in April according to survey data.

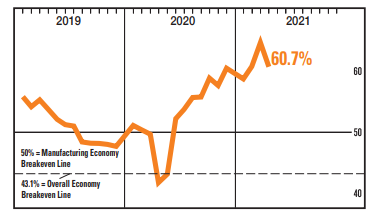

* The U.S. Services PMI indicates the strongest growth on record (since 2009) in April.

* U.S. services growth slowed in April but remained robust as per ISM data.

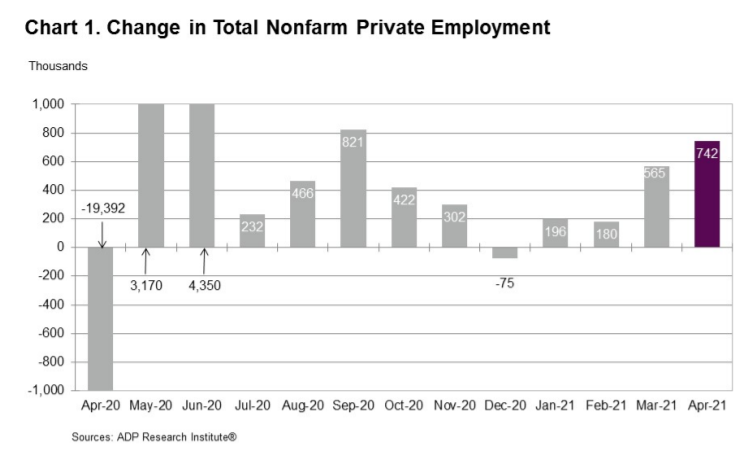

* Growth in U.S. private payrolls accelerated in April, marking the largest increase in seven months:

Ongoing inflation concerns and reports of rising prices for essential materials continue to benefit commodities.

Today’s post introduces the inaugural Risk Review column reviewing major asset classes, to be published monthly. This serves as a companion piece to the monthly performance report and risk-premia estimates. Readers can utilize this trio of reports to quickly summarize historical performance, expected returns, and risk metrics.

* Treasury Secretary Yellen states that rates may need to increase to prevent the overheating of the U.S. economy.

* Supply shortages and logistical bottlenecks could compel companies to raise prices.

* Forecasts suggest Covid-related deaths in India may double in the coming weeks.

* Eurozone growth continued to strengthen in April, as suggested by PMI survey data.

* The birthrate in the U.S.

declined to a record low again in 2020.

* U.S. factory orders sharply rebounded in March.

* The U.S. trade deficit surged to a new record high in March.

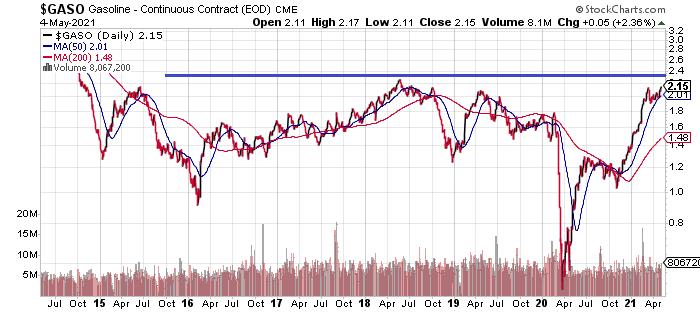

* U.S. gasoline prices are nearing a seven-year peak:

The expected risk premium for the Global Market Index (GMI) saw a slight increase in April, rising to 5.9% annualized—modestly above the previous month’s estimate. Although the current return estimate—defined as performance above the “risk-free” rate—still lags behind the prior peak for realized performance of GMI, this latest revision reflects an encouraging recovery from recent low projections.

* President Biden has lifted the cap on refugees allowed into the U.S.

* A congressional debate is set to commence regarding Biden’s economic plan.

* The pandemic situation in India has worsened, as total reported Covid-19 cases exceed 20 million.

* Warren Buffett has named his successor to run Berkshire Hathaway.

* Global manufacturing activity accelerated in April, as reflected in PMI data.

* U.S. construction spending

rebounded but fell short of forecasts in March.

* The U.S. Mfg PMI continued to rise in April, while the ISM Manufacturing Index unexpectedly declined:

April brought widespread gains across major asset classes, as risk assets around the globe rebounded following significant losses in March. With favorable market conditions, it was quite challenging to incur losses in traditionally managed multi-asset-class portfolios last month.