The Age of Fire Is Over: Why All Existing Forecasts on the Energy Transition Are Wrong

Vincent Petit

Summary via publisher (World Scientific)

The ongoing discourse surrounding climate change and energy transition primarily focuses on decarbonizing energy supply to reduce greenhouse gas emissions. In contrast, this book presents a different perspective.

The Age of Fire is Over: A New Approach to the Energy Transition argues that energy transitions are influenced more by shifts in demand rather than merely changes in supply. By examining recently developed key technologies, the book contends that the actual Energy Transition has yet to begin. It anticipates that upcoming technologies will dramatically reshape demand, delivering services at reduced costs while also introducing innovative services that have yet to be conceived.

In this issue:

- Bounce back: stocks, real estate and commodities recover

- Strong gains for our portfolio strategy benchmarks

Equity Tail Risk in the Treasury Bond Market

Mirco Rubin (EDHEC) and Dario Ruzzi (Bank of Italy)

December 23, 2020

This paper examines the impact of equity tail risk on the U.S. government bond market. It estimates equity tail risk by analyzing the option-implied stock market volatility resulting from significant negative movements, drawing on research by Bollerslev, Todorov, and Xu (2015). The study evaluates the value of this risk in reduced-form predictive regressions for Treasury returns as well as in an affine term structure model for interest rates. Results reveal that left-tail volatility in the stock market significantly predicts one-month-ahead excess returns on Treasuries in both in-sample and out-of-sample scenarios. Incorporating equity tail risk as a forecasting factor can provide substantial benefits for mean-variance investors in bond markets. Furthermore, the term structure model indicates that equity tail risk is effectively priced within the U.S. government bond market. Aligned with the theory of flight-to-safety, findings indicate that Treasury prices rise, and there are net capital flows from equities to bonds as perceptions of tail risk increase. This predictive capability and pricing of equity tail risk holds true for major government bond markets across Europe.

* Biden and a bipartisan group of senators reach an agreement on a near-$1 trillion infrastructure bill.

* The U.S. bans imports of solar materials from China linked to forced labor.

* Which Chinese firms are next to face challenges from Beijing’s fintech crackdown?

* The ongoing influence of Larry Summers on U.S. economic discourse.

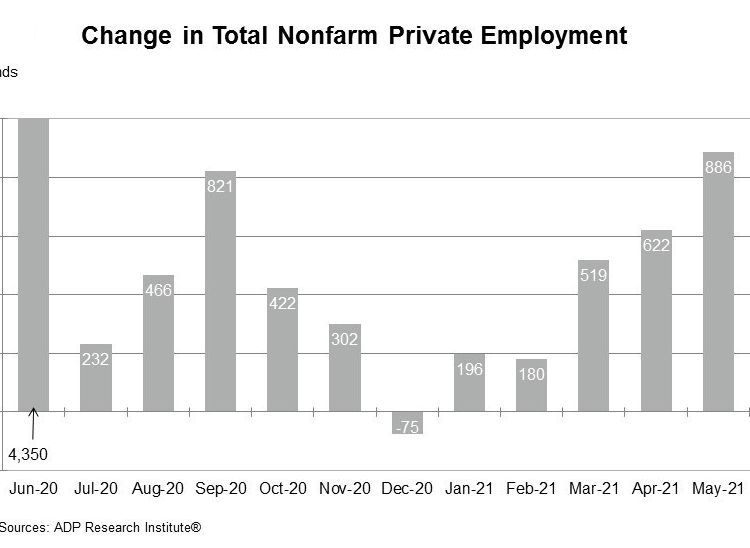

* U.S. jobless claims continue to decline in the latest week.

* The trade deficit for the U.S. increased in May.

* Revised U.S. GDP growth in Q1 was unchanged at a robust 6.4% growth rate.

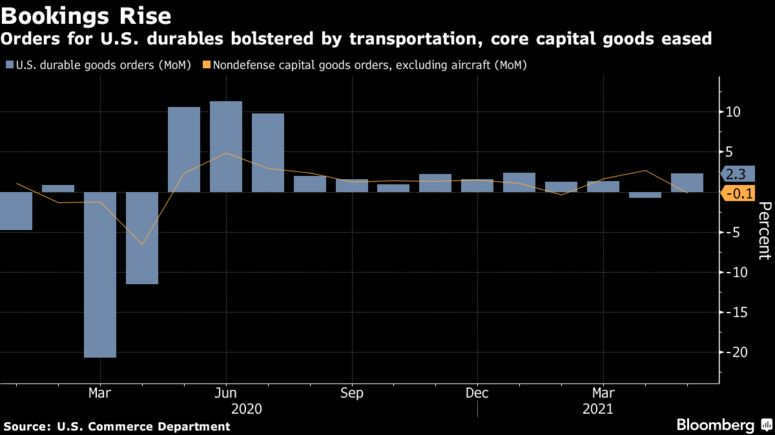

* U.S. durable goods orders rose sharply in May, driven by new orders for aircraft:

The initial estimate for the U.S. economic activity in the second quarter indicates a continuation of accelerated growth, supported by recent predictive models.

* An infrastructure bill is taking shape through negotiations between the White House and the Senate.

* A House committee has approved legislation aimed at curbing the market dominance of Big Tech.

* The White House has replaced the director at the Federal Housing Finance Agency.

* A tense encounter occurred between a British warship and Russian forces in the Black Sea.

* German business sentiment improved in June, reaching the highest level since November 2018.

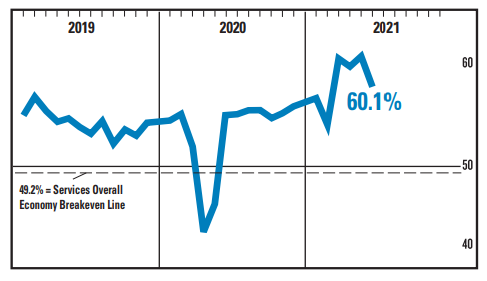

* U.S. economic growth slowed in June, though it remains robust according to PMI survey data.

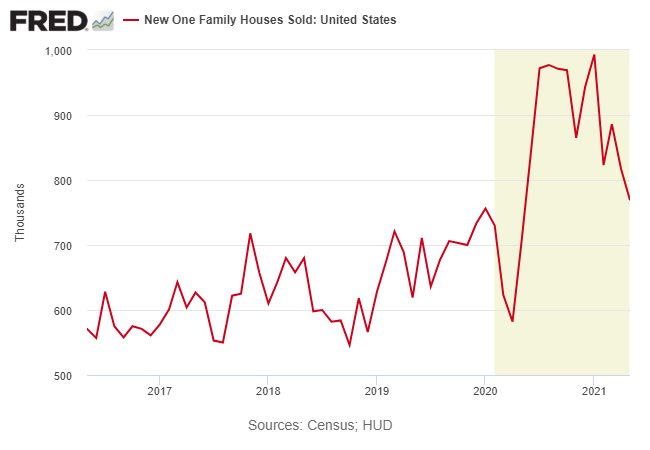

* New home sales in the U.S. declined in May to an 11-month low as prices surged:

The Treasury market reflects rising expectations that the recent surge in inflation may be temporary. While it remains uncertain if this forecast will hold true, the recent easing of 10- and 30-year Treasury yields suggests that investors are increasingly skeptical about the ongoing reflation trade.

While shares in the traditional energy sector may be facing obsolescence as the trend towards renewables continues to gain momentum, Big Oil has still managed to spearhead U.S. equity sectors this year.

* Will the Delta variant trigger a new wave of COVID-19 in the U.S.?

* The Fed chairman downplayed the risks of inflation during congressional testimony.

* NY Fed president mentioned that a rate hike is “still distant.”

* China condemned the recent passage of a U.S. warship through the Taiwan Strait.

* U.S. births decreased significantly following the start of the pandemic.

* The Eurozone economy grew at its fastest pace in 15 years in June, according to survey data.

* The UK saw strong growth in June, with employment reaching record highs.

* Japan’s economy continued to contract in June according to PMI data.

* Mid-Atlantic manufacturing activity strengthened in June.

* In the U.S., existing home prices recorded the highest year-on-year increase on record despite existing home sales declining for the fourth consecutive month in May:

Recently, inflation has surged, prompting concerns that the U.S. economy is facing significant threats to pricing stability reminiscent of the 1970s. Conversely, some experts argue that the current inflation trend is temporary, suggesting that price increases will subside as supply chain bottlenecks ease following the economic reopening. Even in scenarios where inflation proves more persistent than anticipated, the Federal Reserve is expected to intervene effectively.