* Increasing wages in the US spark worries about potential inflation pressures.

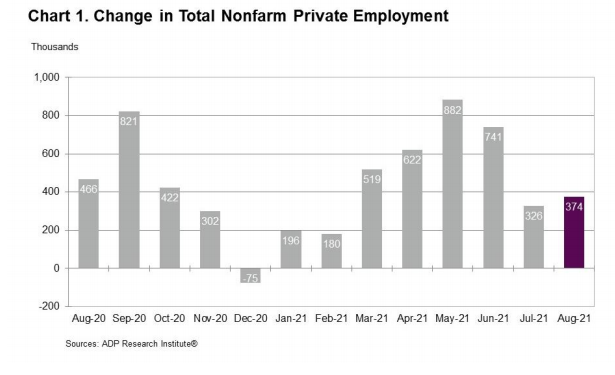

* A Fed official continues to advocate for a rapid ‘taper’ despite disappointing job growth in the US.

* The UK plans to increase taxes to their highest level in decades to address Covid-related deficits.

* Do digital currencies pave the way for significantly negative interest rates?

* Afghanistan announces hardline figures for key positions in the newly formed Taliban government.

* Rising natural gas prices pose a risk to the Eurozone economy and beyond.

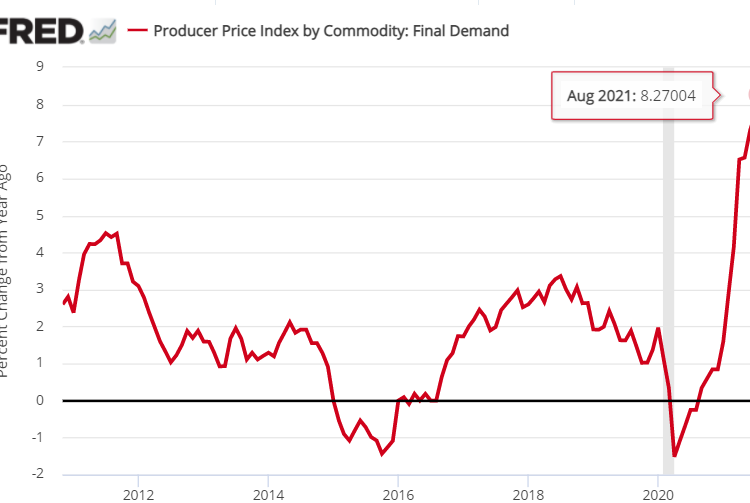

* Does the surge in global inflation signals across economies indicate that it’s temporary?

* The SEC may initiate legal action against Coinbase over its crypto lending initiative.

* The yield on the US 10-year Treasury note has climbed to an 8-week high:

As we approach the end of 2021, uncertainty continues to loom over the economy, inflation rates, monetary policy, and the ongoing pandemic. Investors are striving to gauge how the final quarter of the year will unfold, while the US bond market has shown mixed results year-to-date, as indicated by a selection of ETFs up to September 3.

* The extension of US jobless benefits is set to expire this week for millions still unemployed.

* Economists at Goldman Sachs revise the US growth forecast downward.

* President Xi of China calls for a greater emphasis on wealth redistribution in China.

* The tech crackdown in China is expected to weigh down the nation’s economy, as stated by a former WTO chief.

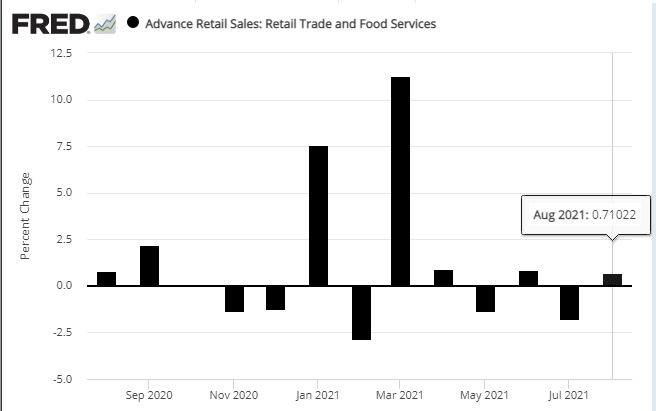

* China’s exports accelerated in August, showing stronger performance despite disruptions from Covid-19.

* El Salvador has become the first nation to recognize bitcoin as legal tender.

* There is a significant gender gap in higher education, as men enroll at record low levels compared to female students.

* Analysts are weighing the possibility that global growth may have peaked.

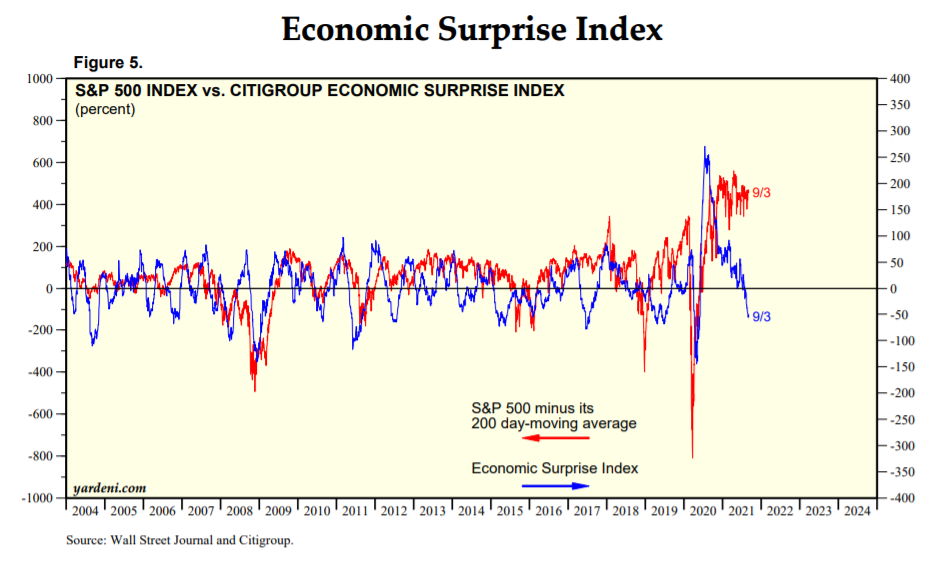

* US stock prices remain high, although the economic surprise index has turned negative.

Many global markets continue to show favorable conditions for risk-on investment, yet our proprietary strategies are lagging behind the unmanaged benchmark—Global Beta 16 (G.B16), which has increased by 12.8% so far this year (see the table at the end for fund composition).

● Shutdown: How Covid Shook the World’s Economy

● Shutdown: How Covid Shook the World’s EconomyAdam Tooze

Review via Reuters

The crisis forced governments to abandon outdated orthodoxies that were already being challenged. Politicians who once aimed to manage public spending found themselves allocating vast resources to support isolated citizens and businesses under restrictions. Central banks significantly increased their bond purchases to stabilize various financial sectors. Prior commitments to free trade and private enterprise were sidelined in the urgent quest for face masks, vaccines, and aid for struggling industries.

- Most global markets posted solid gains this week.

- Our portfolio strategy benchmarks also enjoyed another week of strong performance.

Throughout August, risk-adjusted performance has consistently improved for the Global Market Index (GMI), an unmanaged portfolio that encompasses all the major asset classes (excluding cash). GMI’s Sharpe ratio increased for the sixth consecutive month, reaching 0.93—the highest mark in over two years.

* Millions of jobless Americans stand to lose federal unemployment benefits imminently.

* Japan’s prime minister declares his resignation after a year in office.

* Analysts are seeking insights to predict the Taliban’s governance in Afghanistan.

* China’s Services PMI indicates a sector contraction in August for the first time since April 2020.

* US jobless claims dropped to a record low since the pandemic last week.

* Revised Eurozone Composite PMI shows that growth stayed robust in August.

* GM will suspend most production at its North American facilities due to a chip shortage.

* One of the largest hedge funds will pay up to $7 billion to resolve a tax conflict.

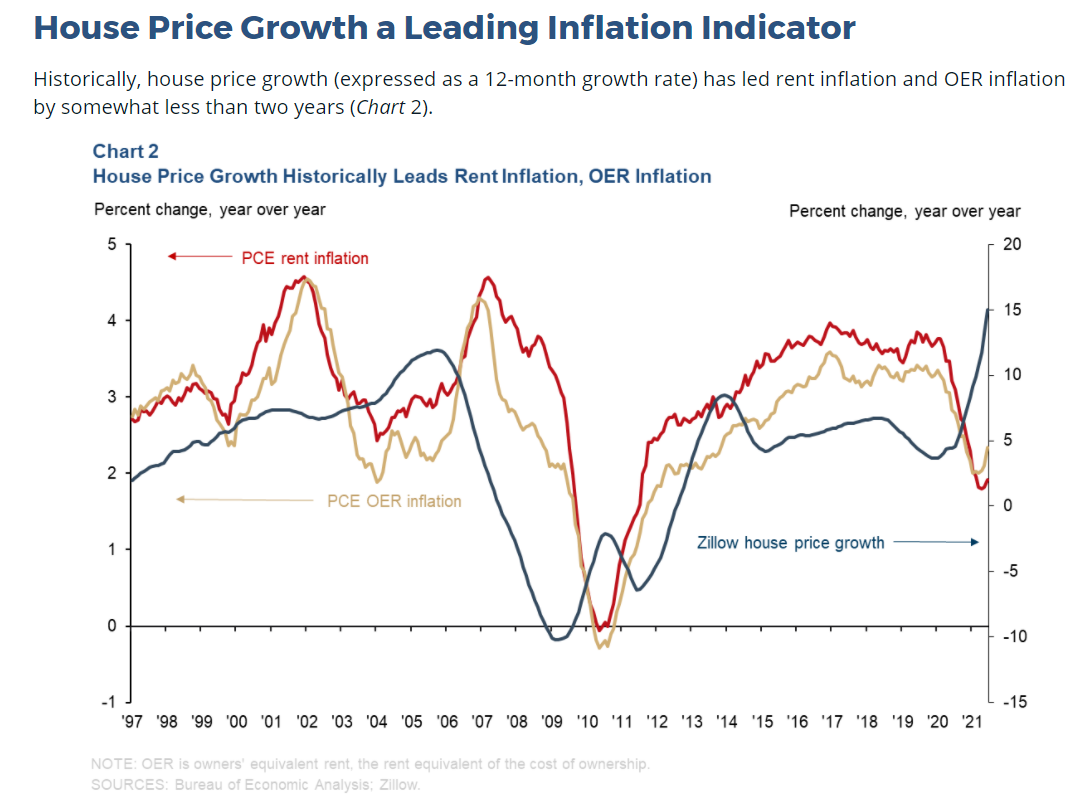

* US rent inflation is expected to rise, according to two economists from the Fed.

The anticipated risk premium for the Global Market Index (GMI) increased in August, reaching an annualized rate of 6.1%. This figure slightly exceeds the estimate from the previous month. This level remains comparatively high when viewed against recent historical trends. The forecast pertains to the long-term outlook of GMI’s returns relative to the “risk-free” rate, based on the yield of a 3-month Treasury bill.