In October, the long-term risk premium forecast for the Global Market Index (GMI) showed a recovery, increasing to 6.1% based on updated figures from the previous month. This revised estimate reflects the anticipated returns above the “risk-free” rate, derived from a risk-based model, which we will explore further below.

* More than 100 countries have committed to halting deforestation by 2030.

* The US is set to introduce stricter regulations on methane emissions in the oil and gas sector.

* A California state court has ruled that drug companies aren’t liable for the opioid crisis, as decided by the court.

* Supply-chain risks for the US economy remain at a near two-decade high.

* Shortages causing a slowdown in auto production pose a risk to the global economy, as reported by The New York Times.

* AQR warns against expecting stocks and bonds to shield investors from inflation.

* 82% of S&P 500 companies have outperformed Wall Street’s earnings expectations.

* Surging volatility in the bond market raises the question of whether this is a warning sign for stocks.

* US construction spending declined by 0.5% in September.

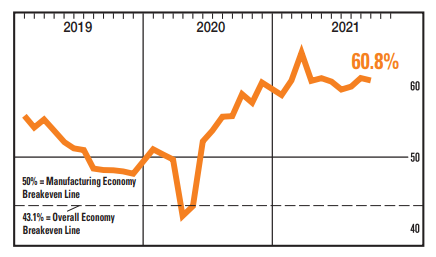

* The US Manufacturing PMI for October shows softer growth, although new orders “remain sharp.”

* The US ISM Manufacturing Index decreased slightly in October, yet still suggests robust growth:

In October, US real estate investment trusts (REITs) and stocks achieved the highest returns among major asset classes, surpassing others significantly.

* President Biden’s initiative for the US to lead climate change efforts faces significant challenges.

* COP26 climate negotiations carry major implications for investors.

* US Covid-19 cases have decreased by 58% from the latest peak.

* The pandemic has accelerated retirements among baby boomers.

* Treasury Secretary Yellen downplays the flattening yield curve, asserting recovery is robust.

* China’s factory output contracted for a second consecutive month in October.

* Japan’s new prime minister plans to boost wealth distribution through a “new capitalism” approach.

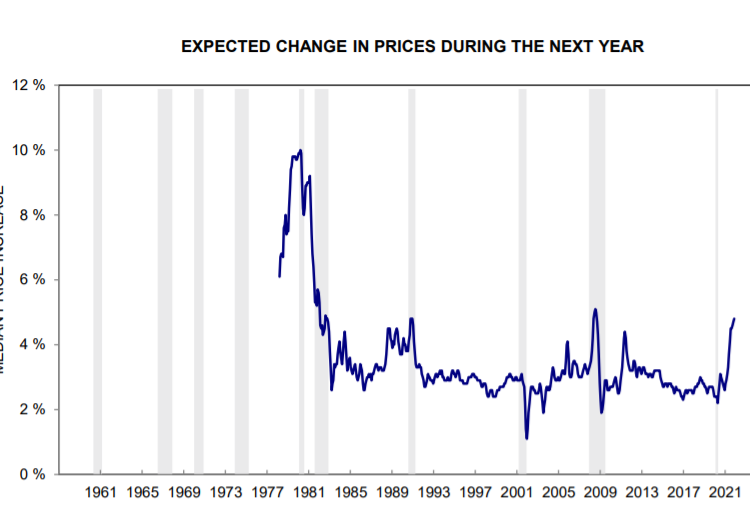

* Consumer prices and wages increased in September at the fastest rate seen in decades.

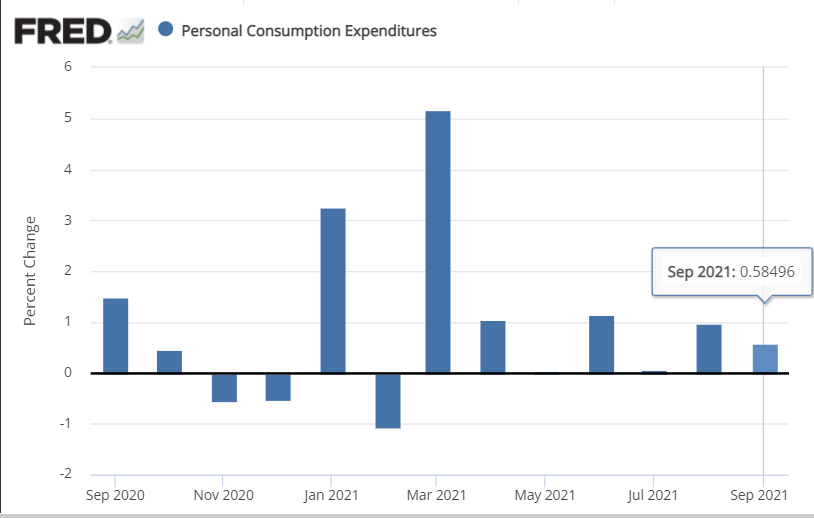

* Consumer spending continued to rise in September:

Andrew Ross

Essay by the author via Orlando Sentinel

The affordable housing crisis in the US is approaching a state of emergency. A recent forecast from Zillow suggests that by December, the average renter will be spending more than 30% of their pre-tax income on rent. This figure marks the official threshold for being classified as “housing-cost burdened.”

With rising housing prices and rents, along with the expiration of eviction moratoriums, millions of renters find themselves at risk of homelessness.

Finding an appropriate yield remains a challenge; however, it appears to be getting slightly easier. A review of our standard ETF proxies for the major asset classes indicates that opportunities for yield-seeking investors are becoming more favorable compared to our previous assessment in April.

* President Biden arrives in Europe for the COP26 climate summit.

* The Democrats’ infrastructure spending package remains unresolved as the month ends.

* Earnings from Apple and Amazon disappoint investors.

* Treasury Secretary Yellen remarks that spending bills will be anti-inflationary by reducing key expenses.

* Inflation in the Eurozone has surged above 4%, pushing toward a possible interest rate hike.

* Jobless claims in the US fell for another week, reaching a new low since the pandemic began.

* The market is beginning to anticipate Federal Reserve rate hikes in 2022.

* Pending home sales unexpectedly dropped in September.

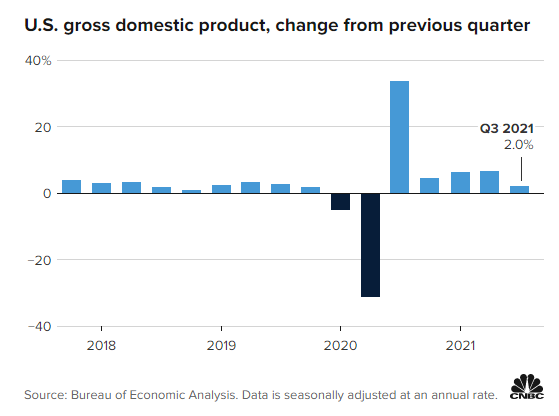

* US GDP growth slowed to 2% in the third quarter, marking the smallest gain since the expansion began:

While it may be too soon to rule out the potential for US inflation to peak in the near future, recent forecasts suggesting an imminent decline in price pressure now appear less likely.

* An attempt to quickly reach an agreement on the Democrats’ social spending plan fails to materialize.

* The US is reportedly providing training to troops in Taiwan.

* A top US general expresses concerns over China’s hypersonic weapons test.

* One-third of China’s property developers are projected to struggle with debt repayment.

* The ongoing chip shortage impacts profits at GM and Ford.

* US economic growth is forecasted to slow in the third quarter, with expectations for a rebound.

* The US trade deficit for goods widened in September, accompanied by a decline in exports.

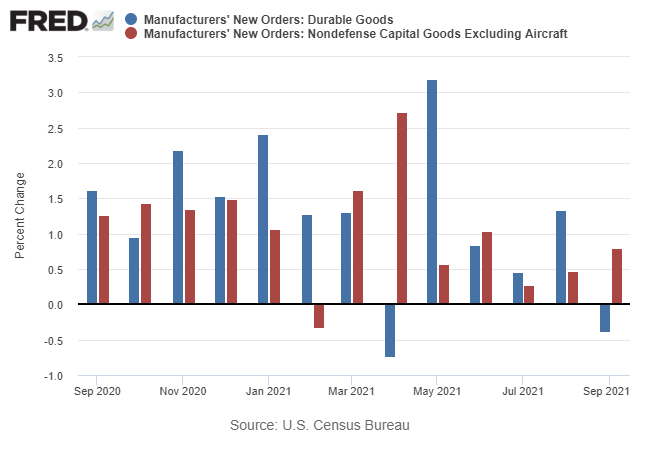

* New US orders for durable goods decreased at the headline level in September:

The resurgence of energy stocks continues as they lead the sector rankings for the year, based on a selection of ETFs through the market close on October 26.

In summary, October brought a mix of financial developments, highlighting risk premiums, supply chain challenges, and the ongoing effects of the pandemic on various sectors. With significant changes in inflation expectations and shifting market trends, investors are navigating a complex landscape that may influence their strategies moving forward.