In recent days, several significant global events have made headlines:

- * North Korea has reportedly launched a ballistic missile into the sea.

- * Protests in Kazakhstan have intensified, prompting the government to declare a state of emergency.

- * The stock market is currently overlooking rising bond yields.

- * Global manufacturing expansion was sustained at the end of 2021.

- * The U.S. may attempt to recover some of its manufacturing output that had shifted overseas, as companies set their sights on reshoring efforts.

- * Toyota surpassed General Motors in U.S. car sales, marking the first time a foreign company has taken the lead.

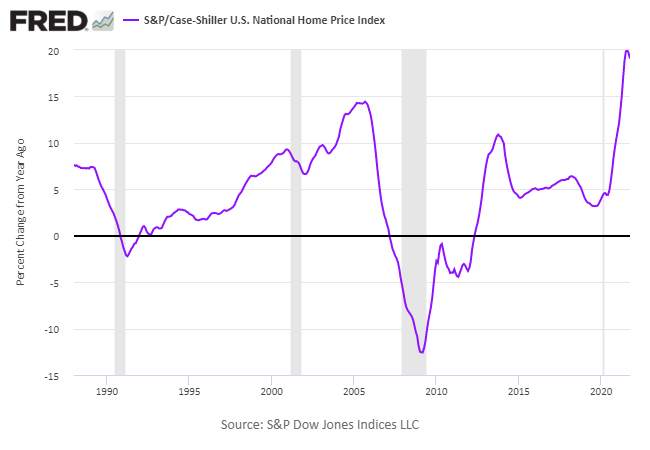

- * Zillow anticipates that U.S. home prices will continue to surge in 2022.

- * Job openings in the U.S. decreased in November, but they remain near record highs.

- * Small-company wages increased by over 4% in December, a record high according to Paychex.

- * U.S. manufacturing activity slowed in December to an 11-month low, as reported by the ISM Manufacturing Index.

The expected risk premium for the Global Market Index (GMI) remained steady at over 6.0% in December. The current estimate of 6.1% (slightly above the previous month’s figure) marks the third consecutive month above the 6.0% threshold.

* The U.S. has recorded over 1 million new daily Covid-19 cases, establishing a global high.

* Despite this surge, severe cases and hospitalizations related to Covid-19 remain manageable.

* Passive ETFs are paying a premium for their predictable rebalancing strategies.

* China’s factory activity grew at its fastest rate in six months during December.

* U.S. manufacturing was constrained in December by ongoing supply shortages.

* UK manufacturing expansion remained robust at the year’s end.

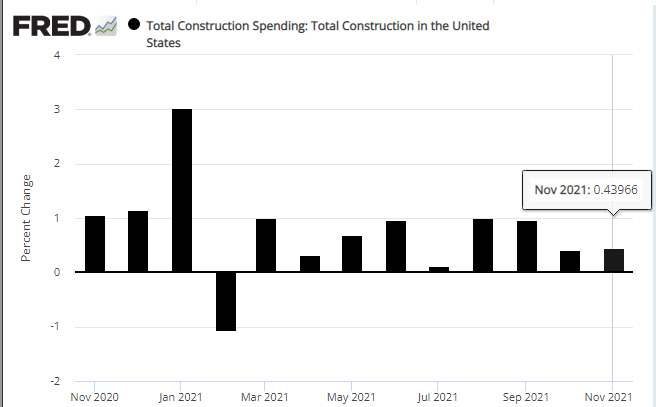

* Construction spending in the U.S. increased for the ninth consecutive month in November:

In December, U.S. real estate shares emerged as the top performers among major asset classes, showcasing significant growth throughout 2021 as evidenced by various ETFs. While many risk assets showed positive returns last month, real estate investment trusts (REITs) significantly outperformed the rest.

* President Biden reaffirmed substantial support for Ukraine in the event of a Russian invasion.

* The hospitalization rate remains a crucial stress test for Omicron, as Dr. Fauci indicates.

* Economists expect that U.S. employment will strengthen despite the recent surge in Covid-19 cases.

* ‘Inflation’ has become the most frequently mentioned term in Wall Street firms’ forecasts for 2022.

* Trading has been suspended in Hong Kong for the troubled property developer Evergrande.

* At least 20 U.S. states are set to raise their minimum wage rates.

* The manufacturing sector in China continued to expand in December, according to survey data.

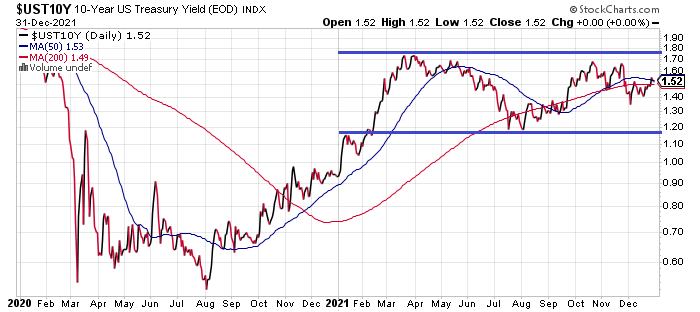

* BlackRock and Vanguard are cautious in their outlook for the U.S. Treasury market in 2022.

* The U.S. 10-year Treasury yield begins 2022 at a middling rate compared to 2021’s range:

This is a follow-up to Best of Books 2021: Part I, highlighting some notable reads from the past year. Regardless of your opinion on 2021, it offered several captivating books that deserve your attention. Here are five selections:

Uncertainty about the future is inevitable, especially when assessing the risks and opportunities for the year ahead. However, one thing is clear: inflation will take center stage in 2022, driving potential surprises.

* U.S. coronavirus deaths have remained relatively low. Will this trend continue?

* Airlines throughout the U.S. continue to cancel flights due to staffing shortages.

* Forecasting remains a complex task. The dual challenges of Covid-19 and inflation are making it even more difficult.

* Biden and Putin are scheduled to hold a phone conversation today amid tensions regarding Ukraine.

* According to industry expert Dan Yergin, U.S. oil output is projected to rise further in 2022, as noted.

* Pending home sales in the U.S. were unexpectedly weak in November.

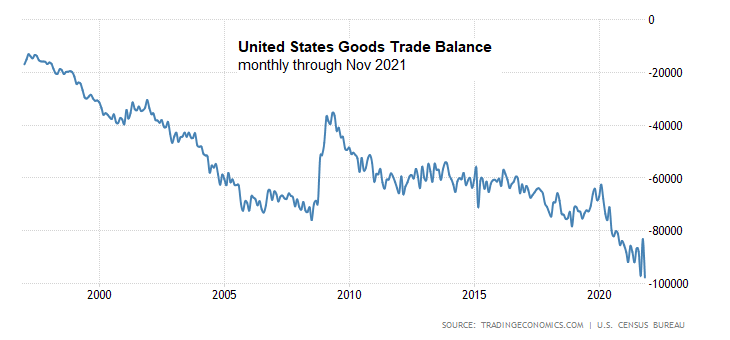

* The U.S. trade deficit in goods reached a new record in November:

The U.S. stock market is finishing the year with impressive gains, largely attributed to robust performance in the energy and real estate sectors.