* Russia is preparing to conduct extensive exercises involving its nuclear forces soon.

* US inflation data indicates the Federal Reserve will likely increase rates by 0.75 points once again.

* Social Security recipients in the US will see an 8.7% increase in their payouts, marking a 40-year peak.

* China’s inflation rose at its fastest rate in over two years as of September.

* The European Central Bank is urged for further rate hikes, as stated by Belgium’s central bank chief.

* Sales from UK pension funds are raising concerns across global bond markets.

* The Japanese yen is trading at a 32-year low against the US dollar.

* New jobless claims in the US increased last week but still remain at historically low levels.

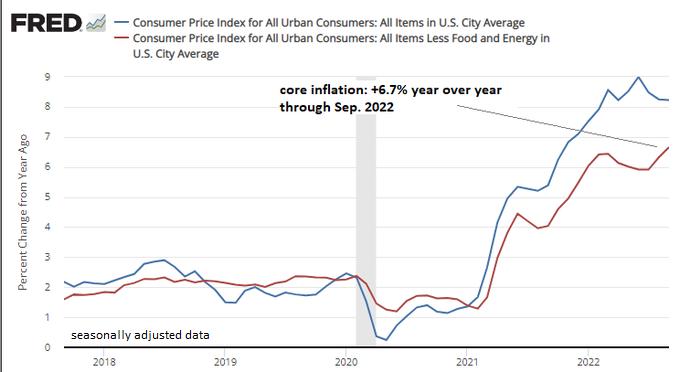

* Core consumer inflation in the US increased in September, reaching a 40-year high:

This year has presented significant challenges for stocks both in the US and globally. However, one notable exception remains—Latin American shares, which are thriving amidst the turbulence.

* Russia is continuing its extensive drone strikes on Ukraine.

* Federal Reserve officials anticipate that elevated interest rates will persist, according to the Fed minutes.

* OPEC+ has warned that the recent oil supply reductions may be a “tipping point for the global economy,” according to the IEA warning.

* Leading chip manufacturer capital spending cuts are a sign of concern for the tech sector.

* Intel is preparing for significant layoffs, raising alarms for the PC market.

* In the US, wholesale prices rose more than expected in September.

* Business inflation expectations remain steady at 3.3% in October, according to a survey from the Atlanta Fed.

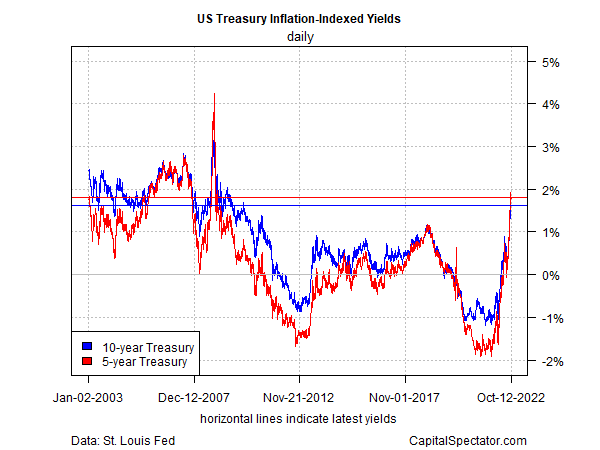

* Real (inflation-adjusted) yields from US Treasury bonds continue to hover near 12-year highs:

The economic outlook for the US appears uncertain due to various macroeconomic and geopolitical risks. Nevertheless, forecasts for a rebound in the third-quarter GDP remain positive, supported by median estimates compiled by CapitalSpectator.com.

* The IMF has issued a caution regarding the global economic outlook.

* Analysts suggest that a weak economic outlook could imply lower inflation

* Treasury Secretary Yellen states that the robust dollar is a ‘logical outcome’ of fiscal policy decisions according to her comments.

* The UK economy contracted in August, surprising many forecasters.

* Long-term inflation forecasts indicate relatively mild pricing pressures.

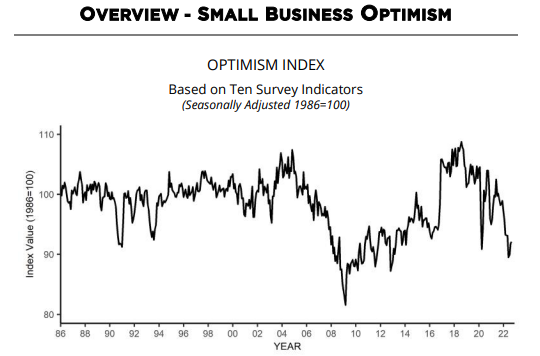

* Small business sentiment in the US has risen slightly for the third consecutive month in September:

Market sentiment varies greatly. Investors continuously assess the macroeconomic outlook, and while there are no definitive forecasts, implied estimates of significant trends emerge. A method to interpret these trends is by analyzing the movement of various proxy ETFs.

* Russia launches a second wave of missile strikes on Ukraine.

* President Putin forewarns of additional attacks following serious strikes on multiple Ukrainian locations.

* According to Goldman Sachs, it’s “premature” to factor in a dovish shift from the Federal Reserve into market predictions as they note.

* Fed’s Charles Evans emphasizes that combating inflation is the top policy objective.

* Fed Vice Chair speaks on how rate hikes will inevitably impact the economy over time.

* The Bank of England intervenes in the bond markets again, citing financial instability risk.

* The US stock market seems poised to revisit its recent lows:

Last week, global markets exhibited a varied performance, yet the overall trend remains negative, as suggested by a collection of proxy ETFs up until Friday’s close (October 7).

* Russia conducts a series of missile attacks across Ukraine.

* The consumer inflation report for September is gaining attention this week.

* The US introduces more restrictions on the sale of computer chip technology to China.

* Questions arise over whether the Federal Reserve-engineered economic slowdown will be more severe than necessary.

* Treasury Secretary Yellen says that oil production cuts pose a risk to the global economy.

* A resilient labor market indicates that the Fed’s inflation reduction efforts will continue.

* Fed Governor Christopher Waller warns that the housing market correction could deepen.

* Core inflation continues to rise, according to the chief economic adviser at Allianz, who notes ongoing increases.

* US payroll employment grew by a solid 263,000 jobs in September:

● The Cashless Revolution: China’s Reinvention of Money and the End of America’s Domination of Finance and Technology

Martin Chorzempa

Summary via publisher (Public Affairs Books)

The landscape of finance—how Wall Street operates and how individuals manage their money—is on the brink of transformation. This change is primarily driven by China, where finance and technology are merging in ways that will have repercussions beyond its borders. This global revolution in finance and technology—fintech—will have a similar impact as the changes brought about by giants like Amazon, Facebook, Google, and Twitter, which have reshaped retail and communication practices. China has rapidly reinvented its monetary system, progressing from a dated, cash-centric approach to one dominated by super-apps developed by tech leaders Alibaba and Tencent.