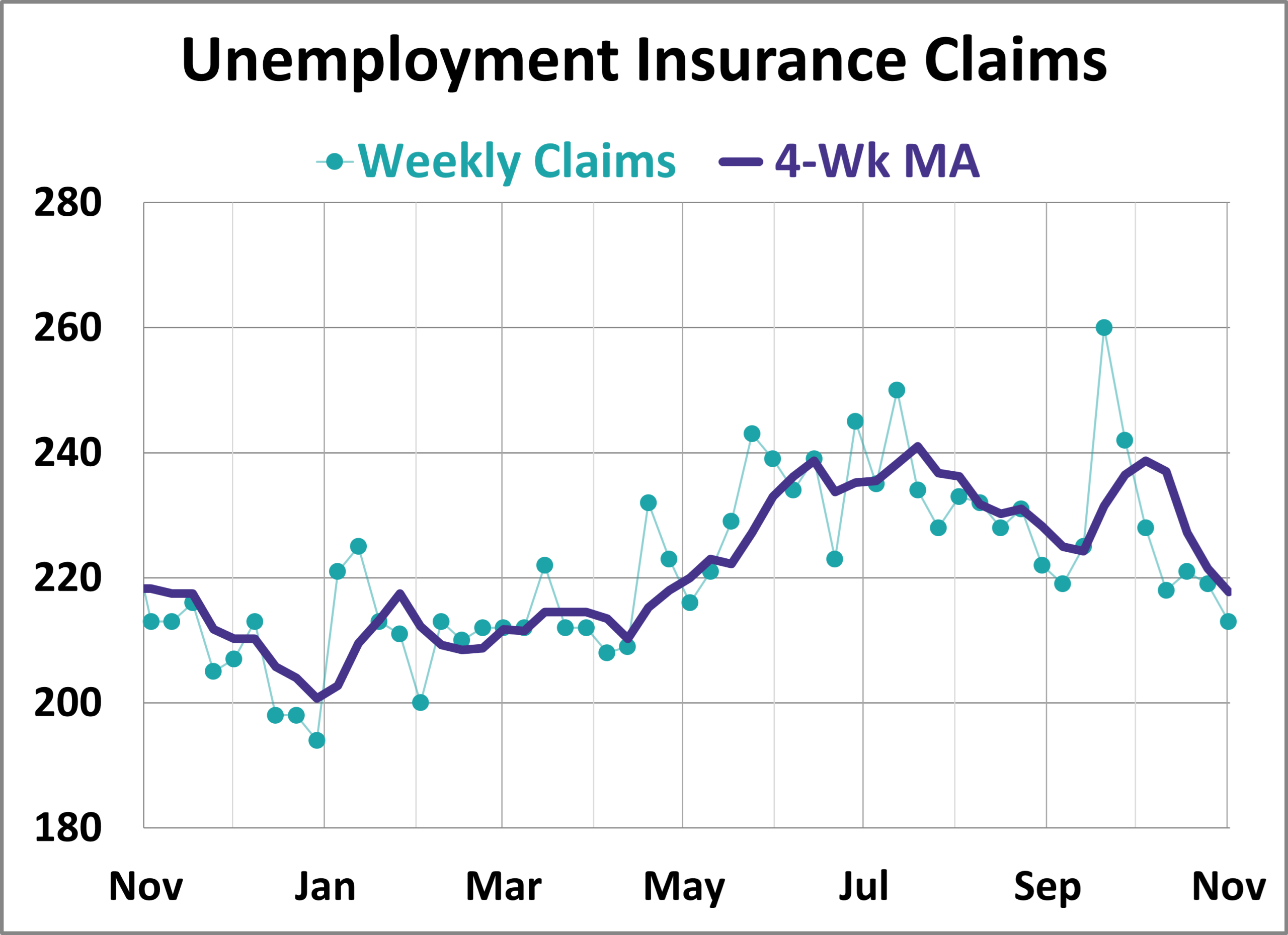

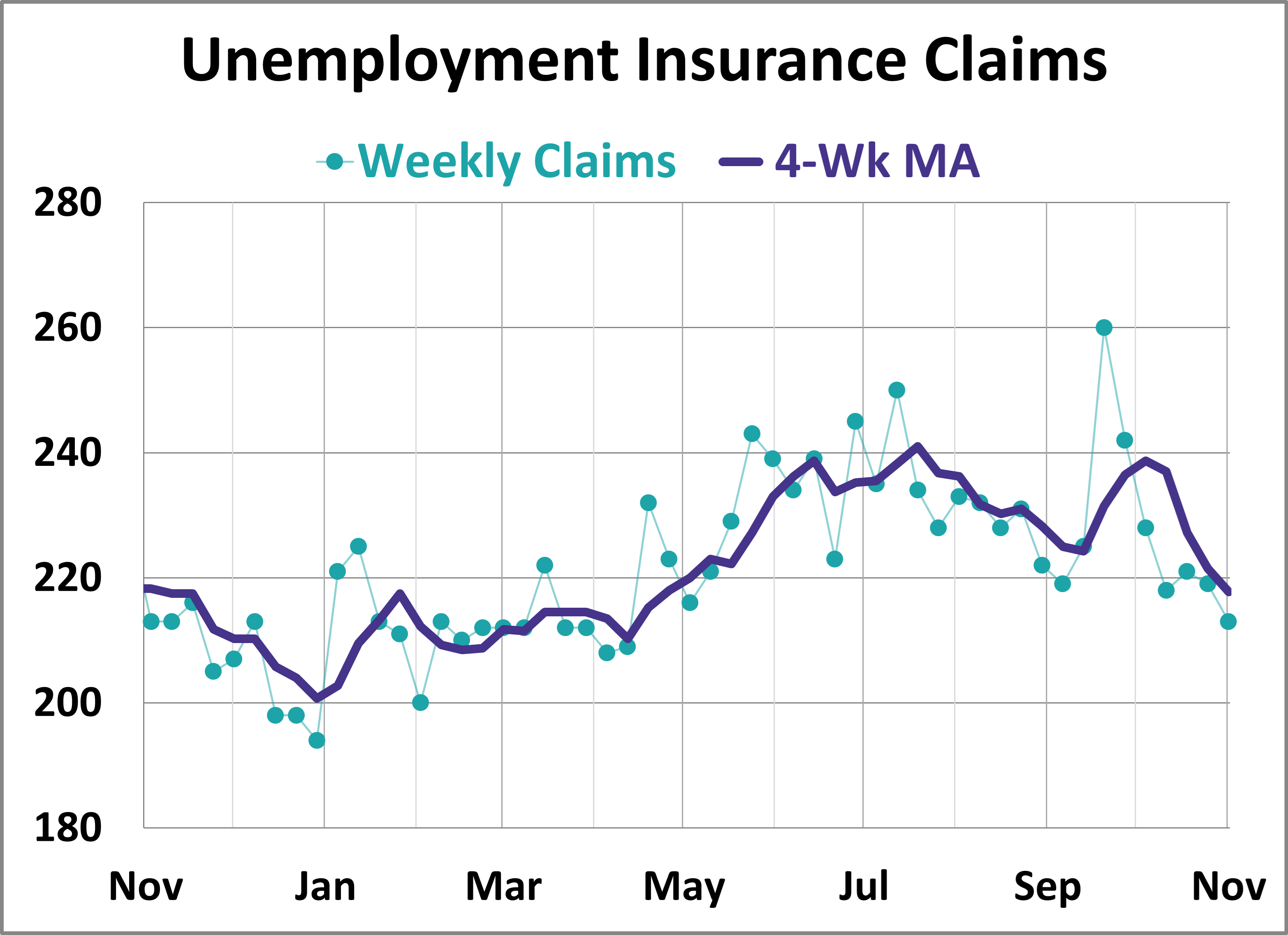

The sustained increase in continuing claims might provoke concern, but initial claims present a considerably more optimistic picture. Which metric truly matters more? It seems that the positive insights drawn from initial claims may offer a more accurate reflection of the near-term job market and, by extension, the economy. However, let’s explore this perspective further to provide clarity before coming to a conclusion.

US jobless claims have dropped to their lowest level since April. According to Jefferies US economist Thomas Simons, “The weekly claims report remains the best real-time barometer of labor market conditions.” He adds, “Currently, the data indicates that the labor market is maintaining a healthy, albeit stable, level.”

If you could monitor only one economic indicator for the economy, tracking payroll trends would be an excellent choice. This metric represents the fuel driving consumer spending, which constitutes nearly 70% of all economic activity. Fortunately, the labor market appears robust, according to several traditional indicators. However, an alternative measure that your editor is observing raises some concerns about possible developments in 2025.

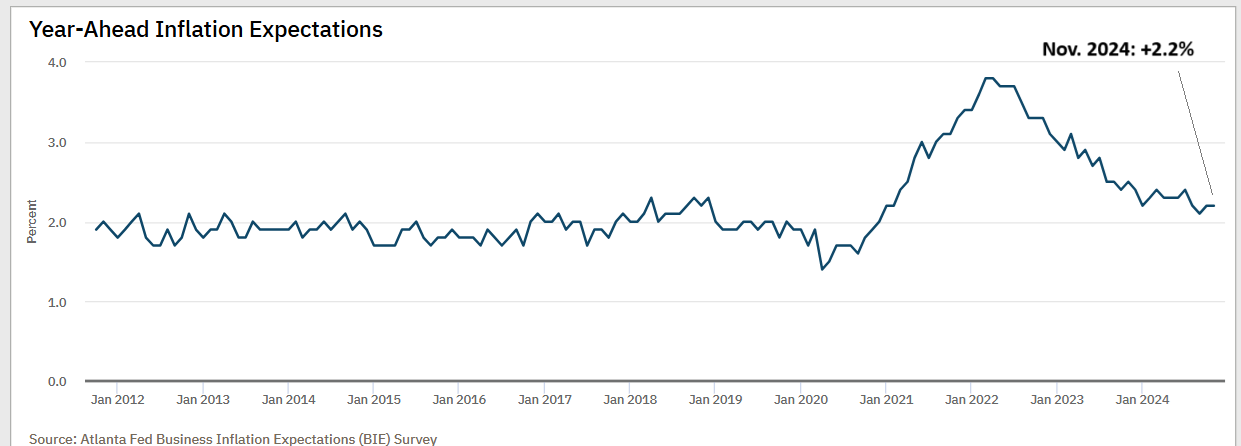

Business inflation expectations in November remained steady at 2.2%, according to the Atlanta Fed. Their latest survey indicates that inflation expectations are close to the lowest levels seen in the past 3.5 years.

The upcoming decisions by central banks could be among the toughest seen in many years. Both policy hawks and doves have substantial evidence supporting their positions. Ultimately, the incoming data will be crucial. However, being overly cautious and waiting for definitive signals might jeopardize the Federal Reserve’s progress in controlling inflation without hampering economic growth. Conversely, one could argue that current policies remain too restrictive for an economy that is showing signs of a slight slowdown.

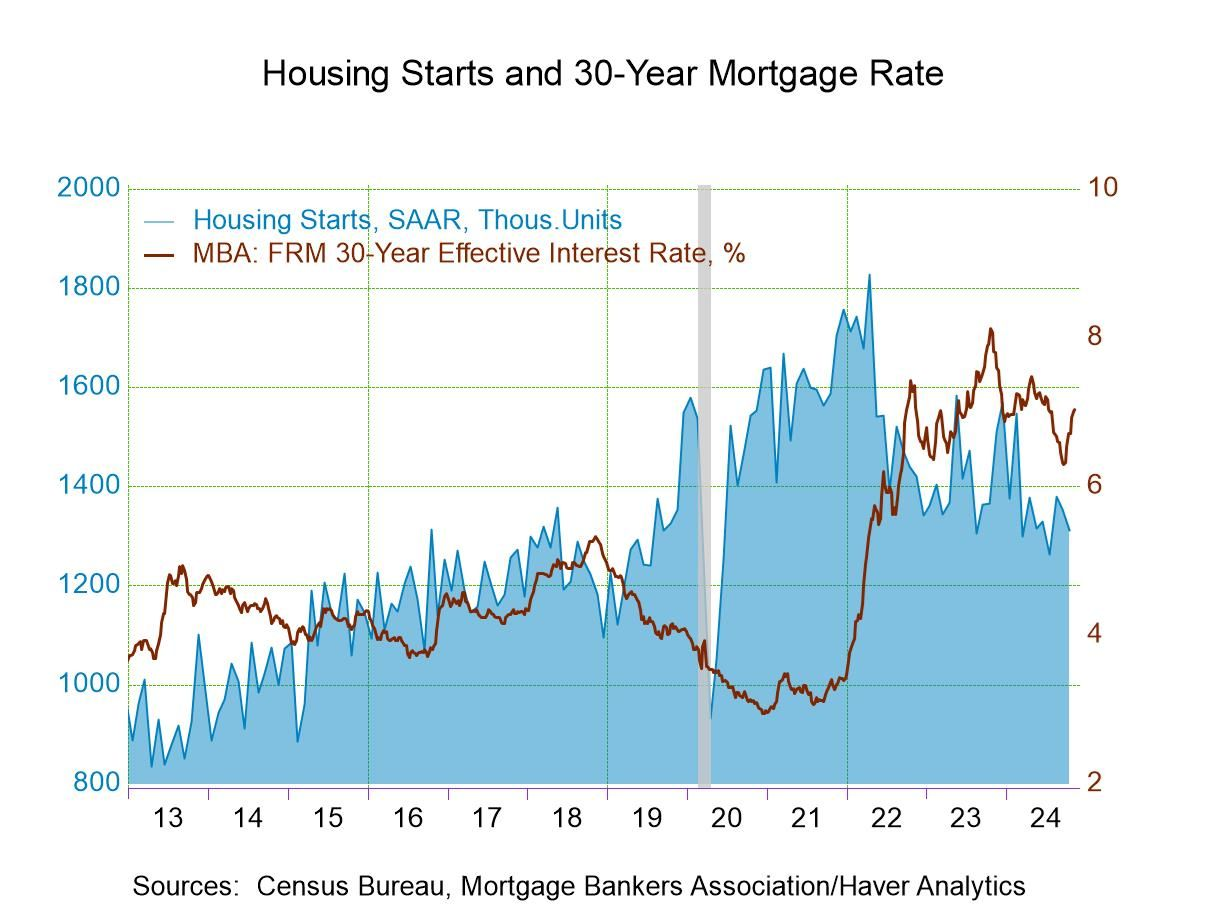

US housing starts experienced a decline in October, dropping 3.1% from September and falling 4.0% year-over-year. Haver Analytics suggests, “Hurricanes Helene and Milton likely impacted housing activity in October.” Christopher Rupkey, chief economist at FWDBONDS, adds, “Despite weather-related disruptions in the South, the downturn in residential housing construction is deepening, leaving buyers facing significant supply shortages as they search for new single-family homes.”

Recent historical trends provide little context for stability, with at least one exception: the average trailing payout rate of a globally diversified portfolio.

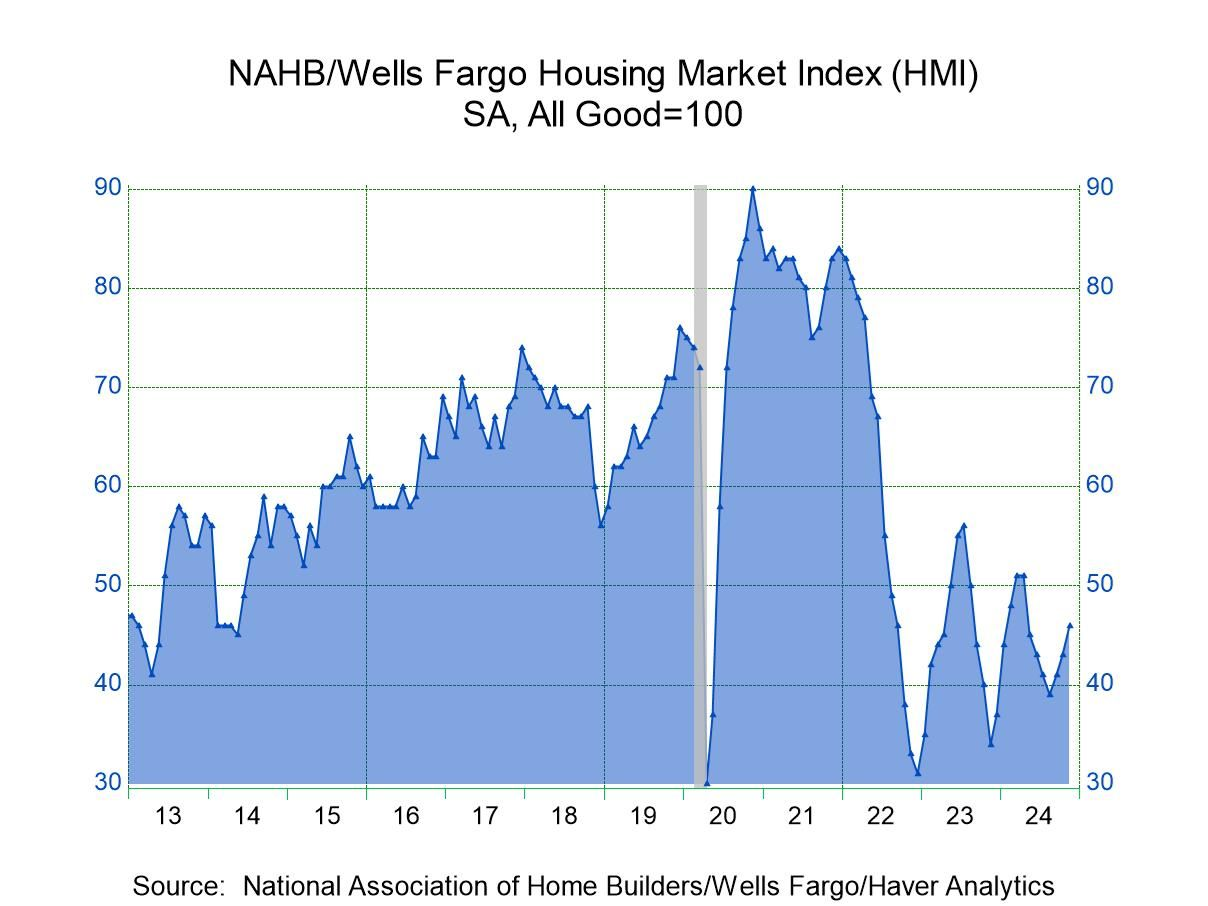

US home builder sentiment has risen for the third consecutive month in November, reaching its highest point since May, although it remains below the neutral 50 mark. “Now that the elections are behind us, builders are increasing their confidence that Republican control in Washington will yield significant regulatory relief, facilitating the construction of more homes and apartments,” states Carl Harris, chairman of the NAHB. “This positive outlook is mirrored in a marked increase in builder sales expectations for the next six months.”

Preliminary forecasts for US economic output in the fourth quarter suggest another potential slowdown, according to CapitalSpectator.com’s initial GDP nowcast. This estimate reflects the consensus among various forecasting sources.

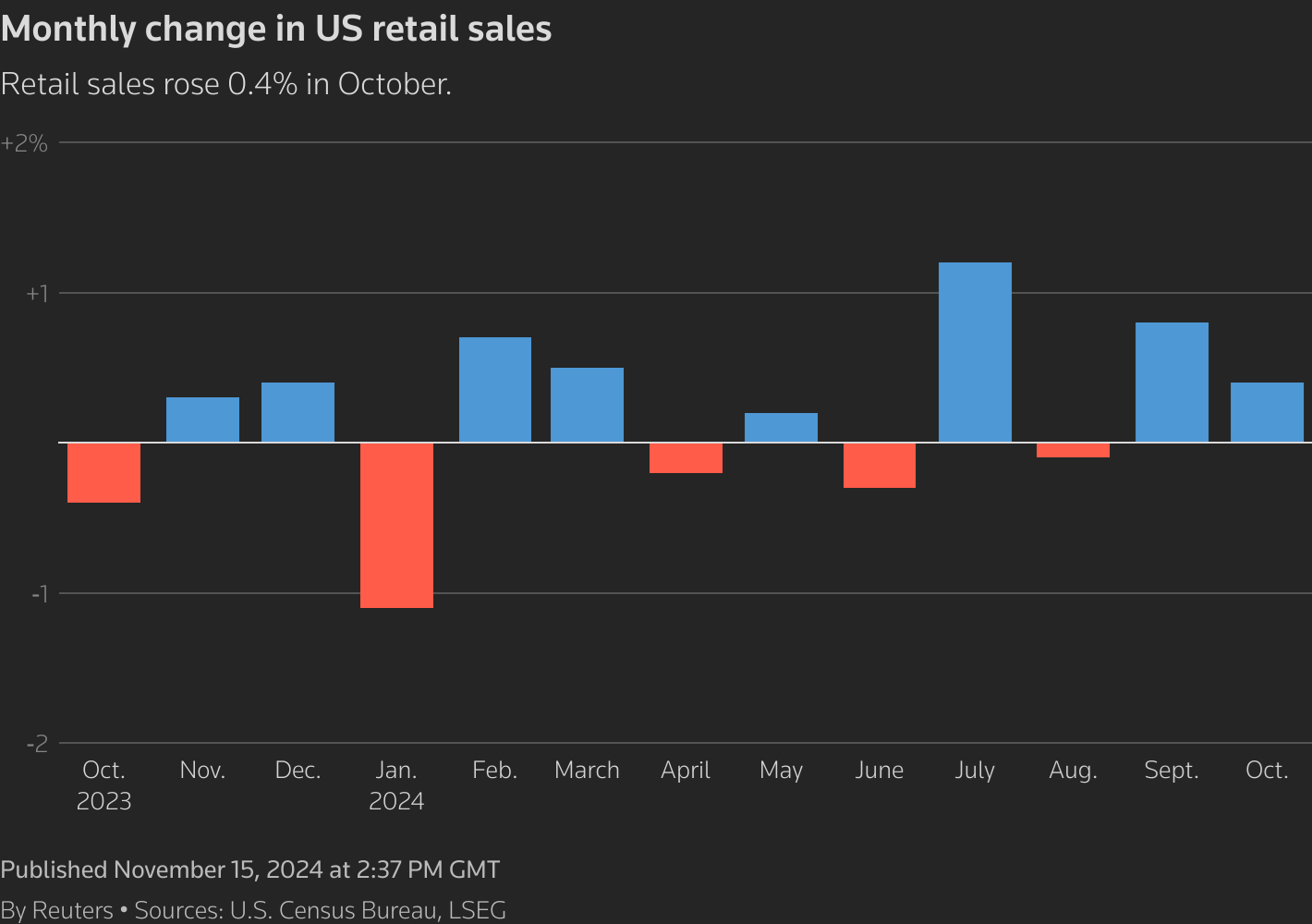

US retail sales outperformed expectations in October, leading to renewed doubts regarding the rationale for further rate cuts. Christopher Rupkey, chief economist at FWDBONDS, states, “October’s retail sales data leads many in the markets to question whether another rate cut in December is justified.” He continues, “As fiscal policies are expected to accelerate in pro-growth initiatives, it might be prudent for the Fed to reconsider adding fuel to the growth fire by lowering rates, which could inadvertently trigger inflation.”

Conclusion:

In summary, the labor market displays both strength and emerging concerns across various economic indicators. While initial claims suggest stability and ongoing employment, the mixed signals from other metrics highlight potential challenges ahead. Monitoring these trends will be essential as we approach the end of the year and look toward 2025.