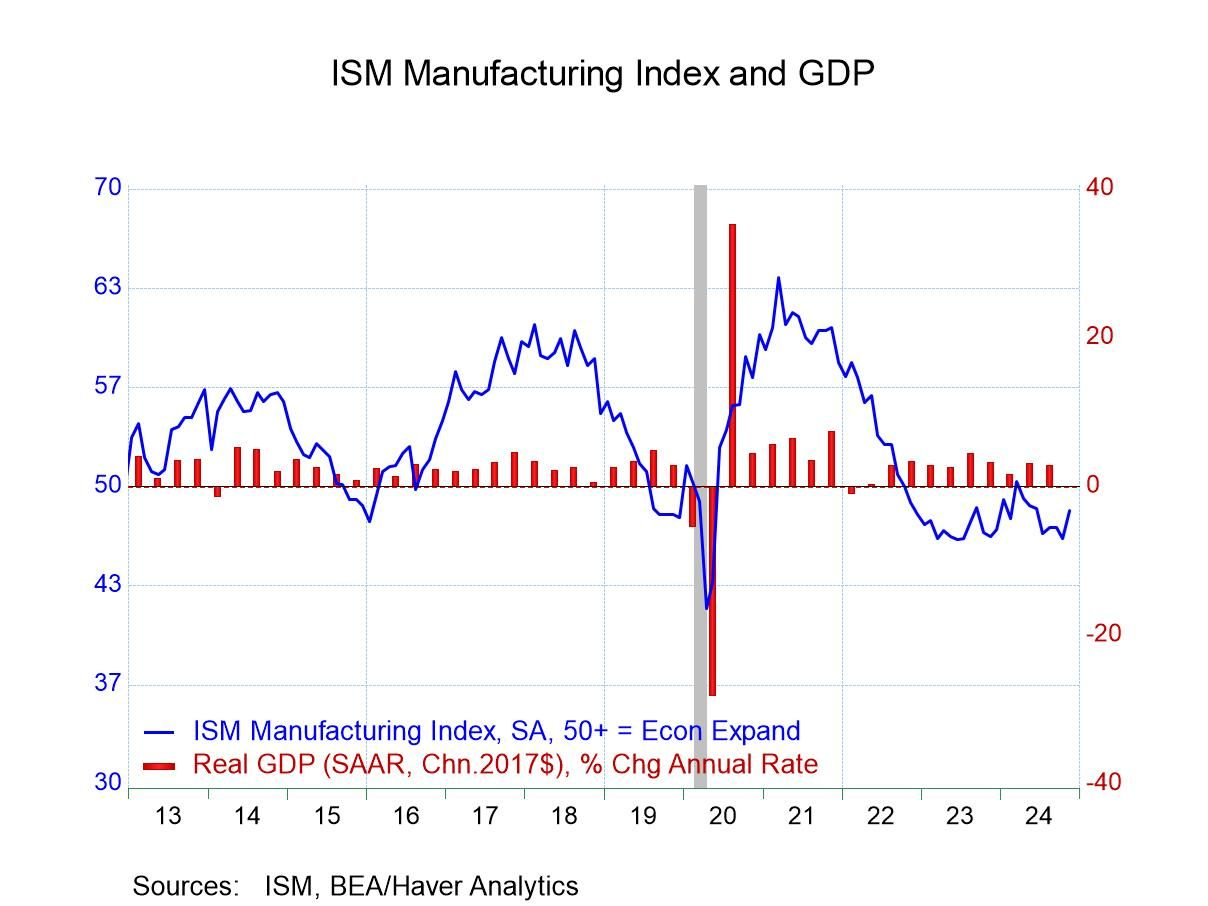

The contraction in US manufacturing showed signs of easing in November, based on the ISM Manufacturing Index. With a reading of 48.4, this is the highest figure observed since June, although it still falls short of the neutral benchmark of 50.

Global financial markets had a mixed performance in November. US stocks and real estate investment trusts emerged as the strongest performers, bouncing back with substantial gains after October’s downturn. Conversely, commodities and shares in emerging markets experienced the steepest losses during the same month.

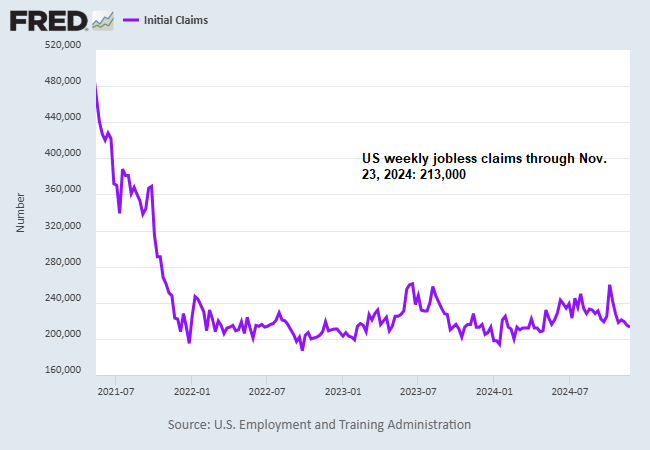

US jobless claims decreased for the third consecutive week, reaching a seven-month low. This decline, along with a relatively low number of new filings for unemployment benefits, indicates that the labor market is likely to maintain its strength for the time being. “The persistent trend in first-time claims shows that companies are managing their workforce carefully in an economy operating at full employment,” noted Joseph Brusuelas, chief economist at RSM US.

Thanksgiving is a time for feasting, expressing gratitude, and stepping away from daily routines. Your editor will be offline for a few days, but regular updates will resume on Monday, December 2. Cheers!

Thanksgiving is a time for feasting, expressing gratitude, and stepping away from daily routines. Your editor will be offline for a few days, but regular updates will resume on Monday, December 2. Cheers!

The US economic landscape is projected to conclude the year with a moderate uptick in output, as indicated by median estimates for Q4 GDP derived from various nowcast methodologies. Consequently, the likelihood of a recession remains minimal in the near future. The pivotal concern now is whether significant changes in US economic policy in 2025 might shift this outlook.

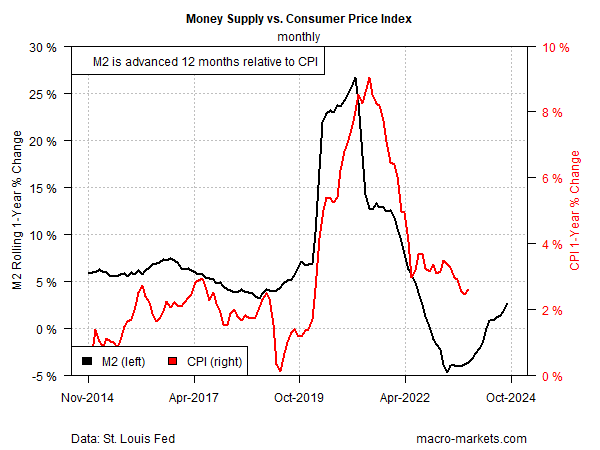

Could a reflation challenge be on the horizon for the Federal Reserve in 2025? A TMC Research note highlights various factors that could converge in 2025, potentially necessitating a recalibration of monetary policy: “Given the potential for reflationary dynamics emerging from multiple sources in 2025, any increase in money supply growth could be ill-timed for the Federal Reserve as it seeks to manage inflation.”

As the year draws to a close, US stocks are positioned as the frontrunners in performance among the major asset classes for 2024.

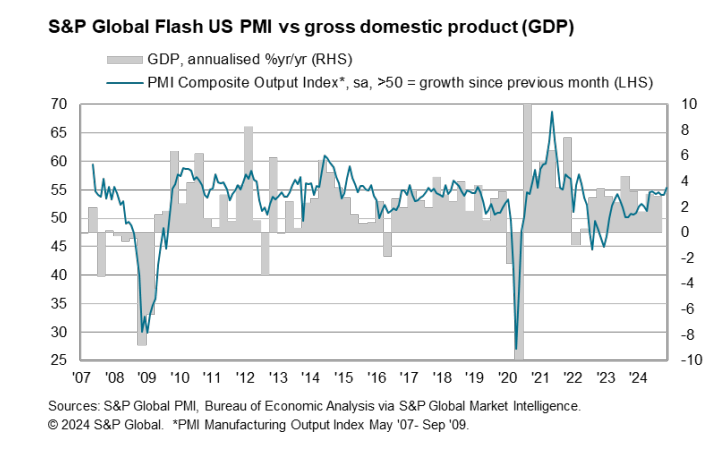

US business activity saw an uptick in November, according to the PMI survey data. The US PMI Composite Output Index, which serves as a GDP indicator, climbed to 55.3, marking a 31-month high. “In November, the overall business sentiment improved significantly, with confidence about future prospects reaching a two-and-a-half year peak,” stated Chris Williamson, chief business economist at S&P Global Market Intelligence. “Expectations of lower interest rates and a pro-business stance from the incoming administration have fostered increased optimism, driving higher output and order inflows in November.”

● Tech Agnostic: How Technology Became the World’s Most Powerful Religion, and Why It Desperately Needs a Reformation

● Tech Agnostic: How Technology Became the World’s Most Powerful Religion, and Why It Desperately Needs a Reformation

Greg M. Epstein

Q&A with the author via The.ink

Q: How does it benefit us to view “tech” – distinct from “technology” as you discuss in your book – as a type of religion? Are there ways this framework may limit our understanding?

A: This perspective helps illuminate the disconnect between the narratives we hear about tech and the actual realities. It prompts us to critically examine our interactions with the mythical realm of Silicon Valley and recognize when we create idealized visions or dystopian scenarios of technology.

The increasing trend in continuing claims raises some concerns, yet initial claims present a much more optimistic narrative. Which metric provides a clearer picture? The promising outlook offered by initial claims likely serves as the superior measure for predicting payroll trends and overall economic health. However, it is crucial to explore this perspective in depth before making definitive conclusions.