Recent updates to the nowcasts for U.S. economic activity in the fourth quarter have shown significant upward revisions. However, the median estimate remains relatively unchanged, based on various data sources compiled by CapitalSpectator.com. Consequently, the U.S. economy appears poised for a slowdown in the final quarter of the year according to the median nowcast.

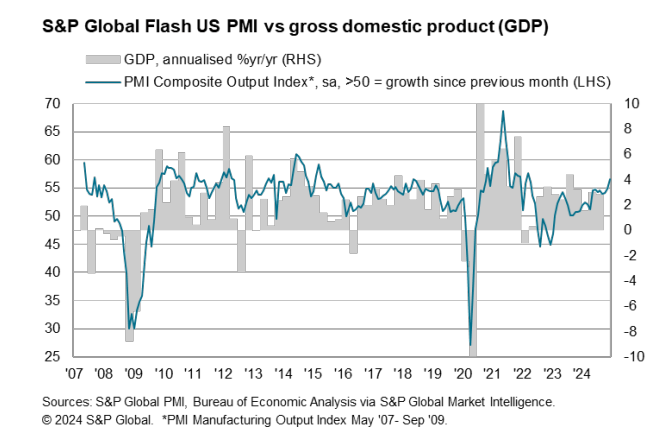

In December, U.S. economic activity reached a 33-month high according to the U.S. Composite, a GDP proxy based on surveys. “The services sector is thriving, with output increasing at its fastest rate since the economy reopened from COVID lockdowns in 2021,” declares Chris Williamson, chief business economist at S&P Global Market Intelligence. “This expansion in the service sector is propelling overall economic growth to its highest level in nearly three years, indicating GDP growth at an annualized rate of just over 3% in December.”

Here’s the follow-up to the first installment of our year-end review of Book Bits columns published in 2024. Enjoy your reading!

● Shocks, Crises, and False Alarms: How to Assess True Macroeconomic Risk

● Shocks, Crises, and False Alarms: How to Assess True Macroeconomic Risk

Philipp Carlsson-Szlezak and Paul Swartz

Excerpt via Harvard Business Review

In 2022, predictions of a wave of defaults in emerging markets due to rising U.S. interest rates were not realized. Similarly, a looming recession was forecasted repeatedly in 2022 and again in 2023, yet the resilient U.S. economy outperformed expectations, delivering strong growth.

This unpredictability comes with financial and organizational costs for executives and investors alike. For instance, automakers that reduced semiconductor orders in 2020 based on misinterpreted recession signals faced lost sales during the subsequent economic recovery. Abrupt strategic shifts in response to false alarms can also erode the trust leaders hold within their organizations. Clearly, understanding macroeconomic trends plays a crucial role.

I’m heading to Boston for a long weekend. I’ll resume updates on Tuesday, December 17. Please refrain from causing any disruptions while I’m away.

I’m heading to Boston for a long weekend. I’ll resume updates on Tuesday, December 17. Please refrain from causing any disruptions while I’m away.

The premium for the U.S. 10-year Treasury yield saw a continued rebound in November compared to a “fair value” estimate calculated by CapitalSpectator.com. This represents the second consecutive month of increased premium, which is now at its highest level since May.

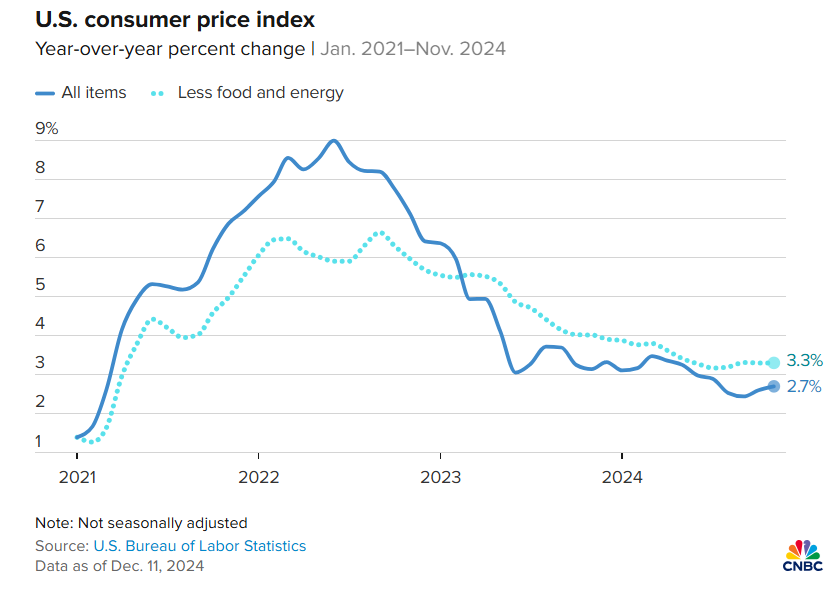

In November, U.S. consumer inflation increased modestly to a yearly rate of 2.7%, marking the second consecutive month of slight upticks. Core CPI, excluding volatile food and energy prices, remained stable at 3.3%. “This consistent core inflation sets the stage for a potential rate cut at the upcoming Federal Open Market Committee meeting,” states Whitney Watson, global co-head and co-CIO for fixed income at Goldman Sachs Asset Management. “With this new data, the Fed will head into the holiday break with confidence in the ongoing disinflation process and is likely to pursue further gradual easing in the new year.”

The competitive race for the top spot among equity sectors has recently shifted to a clear lead for communications services stocks, as indicated by a selection of ETFs through Tuesday’s close (December 10).

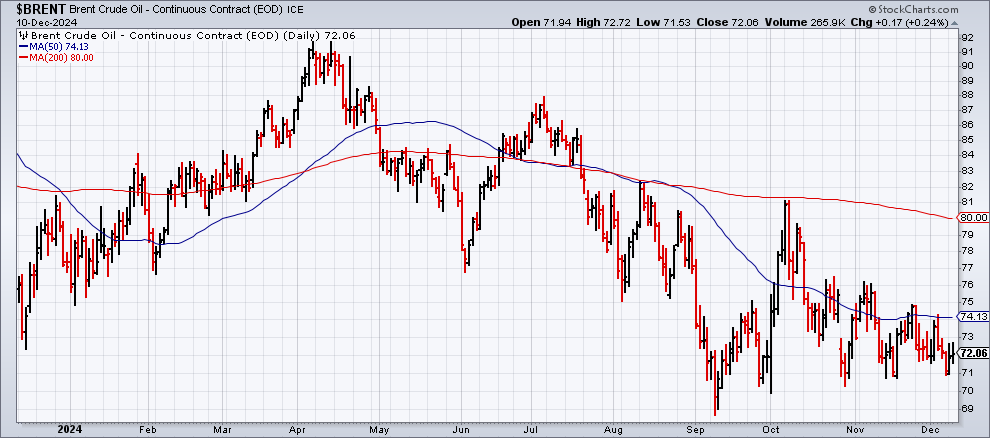

Saudi Arabia faces challenges in its objective to maintain elevated crude oil prices. “Increasing U.S. production and internal pressures within OPEC+ restrict the kingdom’s influence over pricing,” reports The Wall Street Journal. The prospect of deregulation may embolden U.S.-based shale drillers to ramp up output. Simultaneously, the International Energy Agency forecasts that global oil supply will outstrip demand by over one million barrels per day next year unless production cuts are implemented. Brent crude, the international benchmark, has decreased by 6.5% this year.

Disinflation trends have recently stalled, prompting economists to speculate whether this is a brief setback or a signal of a lasting shift. The consumer price report for November, coming out tomorrow, is highly anticipated for insights on this matter.

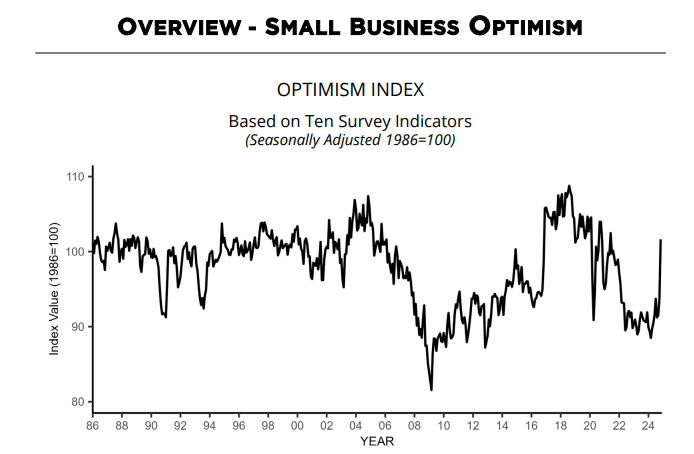

U.S. small business optimism saw a significant rise in November, according to NFIB’s survey. “The election results signify a major shift in economic policy, leading to increased optimism among small business owners,” states Bill Dunkelberg, chief economist at NFIB. “Main Street also reported greater confidence in future business conditions, breaking almost three years of record uncertainty.”

#### Conclusion

The economic landscape in the U.S. demonstrates a combination of optimism and challenges, with significant variations across different sectors. As we move forward, monitoring these trends and their implications will be vital for understanding future economic conditions.