Yves here. I find this particular post frustrating because it overlooks a significant issue: the relatively mild economic fallout from the substantial decline in oil and gas supplies caused by the Iran conflict can largely be attributed to drawing down existing inventories. Energy analyst Steve Hanke suggests that the global decrease in oil supply has reached 14 million barrels per day, while consumption has only dropped by 2 million barrels, thanks to the depletion of stocks. While I am unsure of the exact impact on major economies, it is clear that once these reserves are exhausted, energy prices will surge due to insufficient supply, and buyers will fiercely compete for the limited resources available.

Additionally, this analysis, like many others, overlooks the broader economic repercussions of the Iran conflict, treating energy issues as the sole negative consequence. As commodities expert pointed out in A Crude Awakening, the implications of lost petroleum extend far beyond mere supply disruptions:

OIL IS THE RARE EARTH OF THE MACRO SYSTEM. Over the past fifty years, efficiency gains have made oil cheaper per GDP unit but have also increased its irreplaceability. The remaining oil available is crucial for functions that have no substitutes—like petrochemical feedstocks, aviation fuel, grid balancing, and fertilizers. Removing these resources doesn’t merely diminish demand; it leads to production shutdowns. Today, the world is more susceptible to an oil shock than it was in 1973.

Moreover, and European readers are invited to correct me if I’m wrong, I don’t perceive Europe as more resilient than during the initial stage of the Special Military Operation. The pronounced political divisions and oppressive actions intended to quell dissent, such as electoral manipulation in Romania and restrictions on free speech, suggest otherwise.

It’s noteworthy that the post lacks any images for Figures 3, 4, and 5, but I’m hopeful this will be rectified in due course.

By Maarten Verwey, Director General, DG Economic and Financial Affairs European Commission and Kristian Orsini, Deputy Head, Economic situation, forecasts, business and consumer surveys unit, DG ECFIN European Commission. Originally published at VoxEU

The escalating conflict in the Middle East has sparked a renewed energy crisis for Europe. Although the macroeconomic effects are anticipated to be less severe than those experienced during the 2021–22 energy crisis, this outlook heavily relies on the assumption that supply interruptions will be temporary. This article posits that Europe is entering this crisis from a stronger position, marked by reduced dependence on fossil fuels, enhanced energy efficiency, and accelerated renewable energy adoption. However, if energy prices remain elevated for an extended period, challenging policy decisions are bound to resurface, making it imperative to maintain incentives for structural adjustments and avoid repeating the costly blunders of the past crisis.

The conflict has disrupted shipping routes through the Strait of Hormuz, significantly diminishing global shipments of oil and liquefied natural gas (LNG). Despite substantial progress in decreasing reliance on Russian energy and diversifying supply sources, Europe remains vulnerable to external shocks as long as it primarily relies on imported fossil fuels (Corsello and Foschi 2026). While diversification mitigates vulnerability to specific suppliers, it cannot completely shield the economy from global energy market disruptions.

The channels through which this new energy crisis is manifesting—the second in less than five years—bear resemblance to previous shocks. Rising energy prices are presenting a negative terms-of-trade obstacle for Europe, transferring income abroad in the form of pricier fossil fuel imports. Initially driven by escalating energy costs, inflation is projected to rise again, eventually broadening to encompass more energy-intensive items within the consumer basket—this includes food—and finally transitioning to more persistent service inflation. Domestic demand is expected to wane, with investment visibly adjusting in response to lower margins, stricter monetary and financing conditions, greater uncertainty, and increased risk premiums.

Private consumption is also likely to taper off as elevated inflation diminishes real disposable income growth, prompting households to temporarily increase precautionary savings. The negative impact from net exports is expected to amplify as slumping global demand exacerbates pre-existing challenges related to prices and competitiveness.

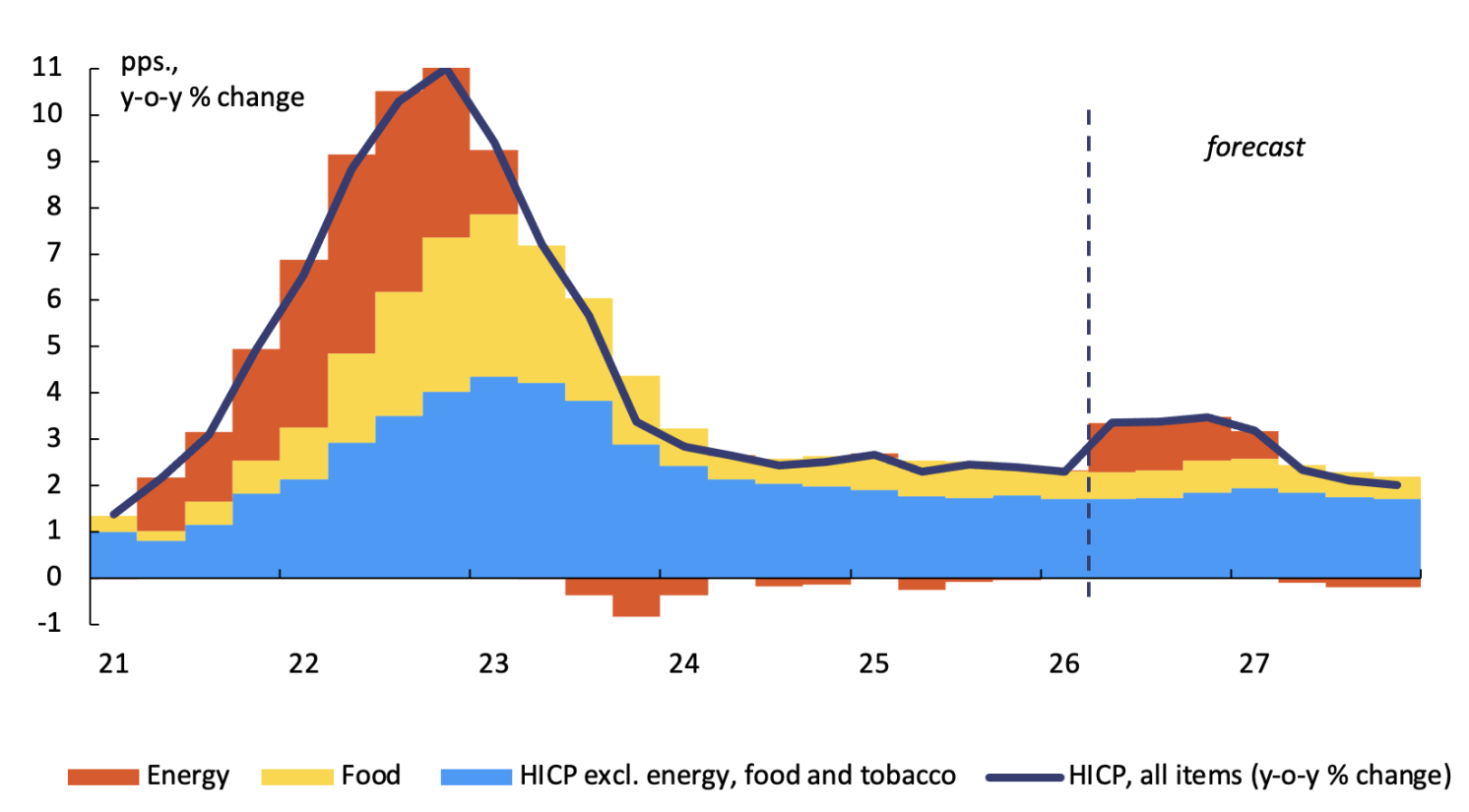

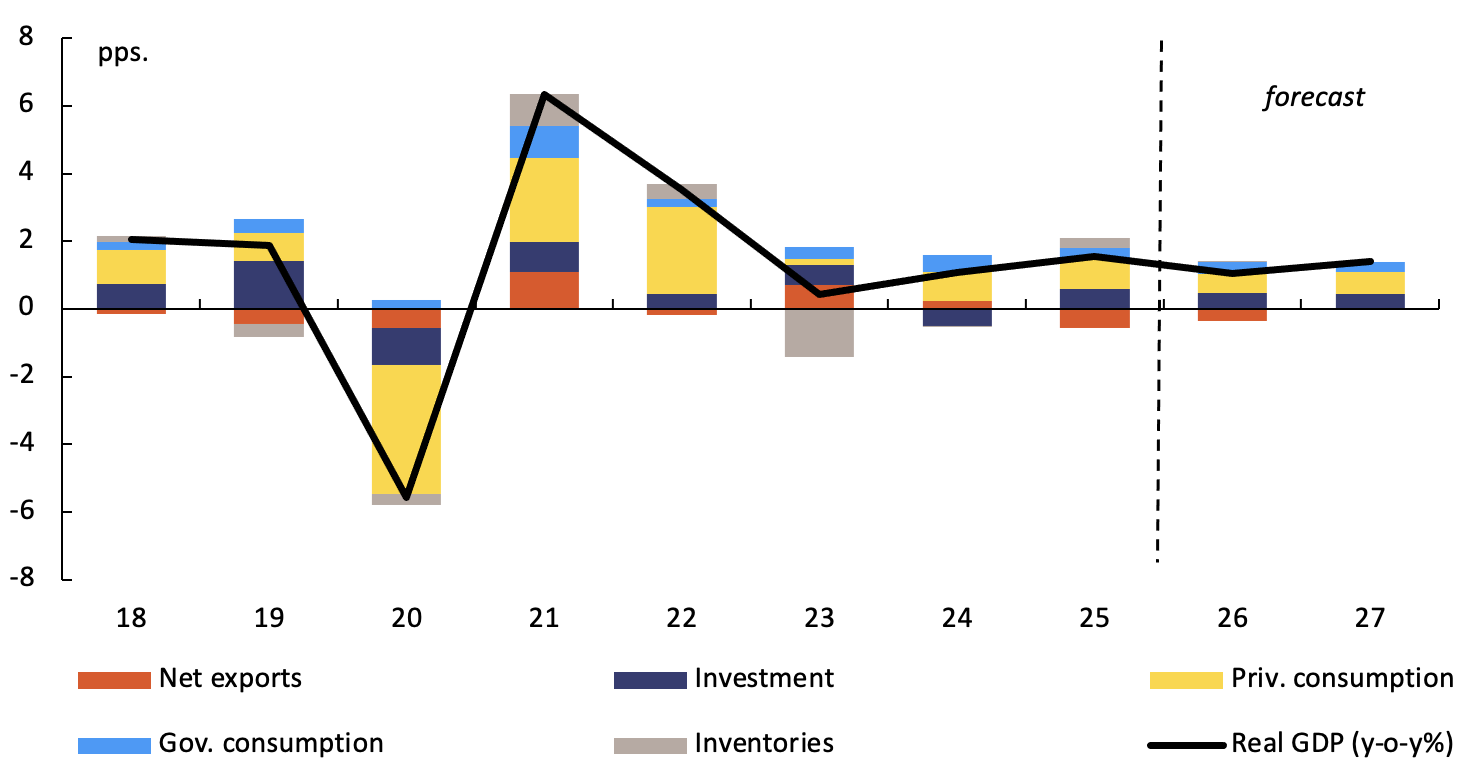

According to the European Commission’s 2026 Spring Forecast (European Commission 2026), after reaching 1.5% growth in 2025, EU GDP is projected to slow to 1.1% in 2026—0.3 percentage points lower than the Autumn 2025 forecast. Similarly, inflation is expected to rise to 3.1%, a full percentage point above earlier estimates. The effects from the energy shock are anticipated to extend into 2027, with GDP growth only modestly recovering to 1.4% and inflation declining to 2.4%, still 0.3 percentage points higher than previously projected (Figures 1 and 2). Notably, the impact of the Middle Eastern conflict is more significant than what a basic comparison with prior forecasts would suggest.1

Figure 1 Inflation breakdown in the EU

Source: European Commission Spring 2026 Forecast.

Figure 2 GDP growth in the EU

Source: European Commission Spring 2026 Forecast.

Despite these challenges, the overall macroeconomic fallout to date is not as severe as what was felt during the previous energy crisis. Several factors contribute to why this current shock has proven to be more contained. The earlier crisis stemmed from the gradual tightening and eventual fizzling out of Russian gas supplies to Europe, at a time when the EU was heavily reliant on pipeline imports and had limited alternatives for short-term replacements. Addressing the loss of Russian gas necessitated a comprehensive reorganization of Europe’s energy supply framework, including the establishment of new LNG import capacities, alternative supply contracts, and significant modifications to energy infrastructure. In contrast, the current crisis largely arises from shipping disruptions and energy exports from the Gulf. Although these disruptions impact globally traded energy markets and have effects that extend beyond Europe, they are likely to resolve more promptly once shipping routes and export infrastructures return to typical operations.

As such, the rise in energy prices has remained comparatively muted versus the extreme spikes seen during the 2021–22 crisis, particularly in gas prices, which peaked at fifteen to twenty times their previous levels. Current futures prices suggest a general expectation that supply conditions will improve in the months ahead as shipping limitations start to ease. Accordingly, projections indicate oil and gas prices should decline from current levels, although they are likely to stabilize at levels above pre-conflict averages.

Unlike the previous energy crisis, the current situation isn’t hitting an economy already experiencing intense underlying inflationary pressures. The rebound dynamics post-pandemic have subsided, labor market resilience has begun to wane, and financing conditions have become significantly tighter.

Nonetheless, this seemingly favorable baseline remains precariously reliant on the assumption that global energy market disruptions will be temporary. Current forecasts were predicated on the expectation that shipping through the Strait of Hormuz would resume swiftly, and supply conditions would normalize in subsequent months. However, as the conflict continues, the likelihood of such an outcome diminishes, raising the possibility that energy prices may stay elevated for longer than previously thought. Thus, the risks related to the economic outlook are increasingly skewed toward the potential for a prolonged energy crisis.

If elevated energy prices persist beyond current projections, there will be growing pressures for policy interventions. The lessons learned from the previous crisis remain highly relevant in this context.

Today’s enhanced resilience in the EU is primarily a result of ongoing structural adjustments initiated and intensified by the last energy crisis. Some of these adjustments were driven by strong price incentives established following the steep rise in energy costs after 2021, while others stem from proactive policy decisions, such as rapidly expanding renewable energy, investing in energy infrastructure, and improving efficiencies through initiatives like REPowerEU. These efforts are complemented by significant regulatory reforms initiated before the crisis.

Since 2008, the gross available energy in the EU has dropped by around 20%, with about half of this reduction occurring in the past five years (Figure 3) (Jaxa-Rozen et al. 2026). Simultaneously, the swift adoption of renewable energy sources has lessened the dominance of fossil-fuel-generated electricity, thereby weakening the impact of gas price fluctuations on electricity pricing (Figure 4) (Borg et al. 2026). Collectively, these advancements have significantly diminished Europe’s reliance on imported fossil fuels and its susceptibility to external energy crises.

Figure 3 Structure of reductions in energy use in the EU from 2008 to 2024

Source: European Commission, Eurostat.

Figure 4 Electricity and natural gas (TTF) prices evolution in the EU

Note: Electricity futures (historical and future) are averages for DE, FR, IT, ES, NL, BE, and AT weighted by GDP.

Source: ICE Futures Europe.

While structural adjustments have bolstered Europe’s resilience, the last crisis also highlighted the limitations of wide-ranging fiscal interventions aimed at protecting households and businesses from rising energy costs. Following price surges in 2021 and 2022, governments enacted extensive fuel tax reductions and regulated retail pricing. These measures allow Member States to temporarily alleviate the burden of elevated energy costs for vulnerable households and energy-intensive businesses. However, Europe cannot rely on subsidies to mitigate an energy supply shock. If not funded by cuts elsewhere in government spending or through increased taxation, the financial burden of these measures ultimately falls on public finances, accumulating to 2.2% of EU GDP between 2022 and 2024. More critically, broad-based price subsidies and blanket tax reductions can dampen the essential price signals needed to encourage energy conservation, efficiency advancements, and investments in alternatives. This is significant not only for energy policy but also for macroeconomic stability. By maintaining demand amidst constrained supply, broad support measures can lead to more persistent inflationary pressure, which in turn necessitates tighter monetary conditions for an extended period. Higher financing costs would negatively impact investment across various sectors, including rate-sensitive investments in renewable energy, electricity grids, storage, and energy efficiency solutions (Jaxa-Rozen et al. 2026)—the investments necessary to enhance Europe’s resilience against future shocks (Lane 2026, Schnabel 2023).

Up to this point, the overall fiscal response has remained modest compared to what occurred in 2022, reflecting both the milder energy price increases and a more cautious approach in a context of narrower fiscal space. By early May, the direct budgetary costs of measures enacted were limited to 0.07% of EU GDP in 2026. Should the current measures be extended throughout the year, costs could approach 0.1% of GDP (Balcerowicz 2026).

Figure 5 Design of energy support measures, 2022 vs. 2026

Source: European Commission Spring 2026 Forecast.

Critically, the structure of many of these measures still mirrors those from the previous crisis, heavily relying on broad price interventions (Figure 5). This could become increasingly problematic if energy prices remain high for longer than currently expected, as political pressure to enhance existing schemes and introduce additional untargeted support measures is likely to mount.

The policy implication is clear: every euro spent on suppressing energy prices largely finances increased import costs for fossil fuels. In contrast, every euro invested in renewable generation, electrical networks, storage infrastructure, or energy efficiency diminishes future susceptibility to external shocks. While fiscal measures may still be essential in alleviating the effects of higher energy costs for vulnerable households and vital energy-intensive industries, support should be temporary, targeted, and designed to avoid undermining incentives for energy conservation, efficiency gains, and alternative investments. Ultimately, Europe’s resilience relies less on shielding the economy from necessary adjustments and more on accelerating the ongoing structural transformation (Mramor et al. 2026). This moment calls for reinforcing incentives for energy conservation and continuing to transition away from fossil fuels (Kammer 2026). The advancements spurred by the previous crisis equip Europe to handle the current challenges more effectively.

For references, see the original post.