As of May 26, European stocks have outperformed other major global equity markets for returns in 2021, driven by a range of exchange-listed funds.

* President Biden has ordered an investigation into the origins of the coronavirus.

* More investors are betting on further growth in Eurozone stocks.

* Will Biden reappoint or replace Fed Chairman Powell, whose term ends in February?

* Supply shortages loom globally as China’s factories face constraints.

* A key Biden official in Asia mentions that the era of US engagement with China has ended.

* Hedge fund assets have reached a record $4.1 trillion.

* The Chinese currency has reached its strongest level since 2016 against a basket of trading partners.

* An activist investor successfully ousts directors from Exxon in a landmark pro-climate campaign.

* A Dutch court has ordered Royal Dutch Shell to increase its carbon emissions reductions.

* Amazon has announced its acquisition of MGM and its extensive library of films and TV shows.

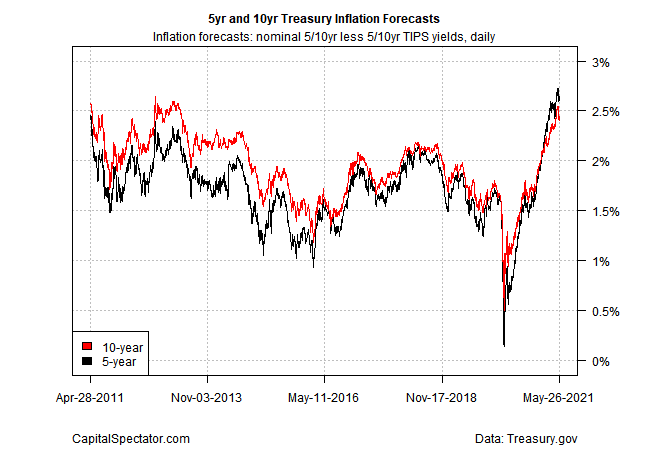

* Inflation forecasts in the Treasury market remain below recent peaks:

Currently, emerging markets are attracting attention in global asset allocation strategies, as many believe they will significantly benefit from the economic recovery driven by vaccinations. This view is interesting and holds validity, but early results have been mixed when examining a broad cross-section of emerging market stocks.

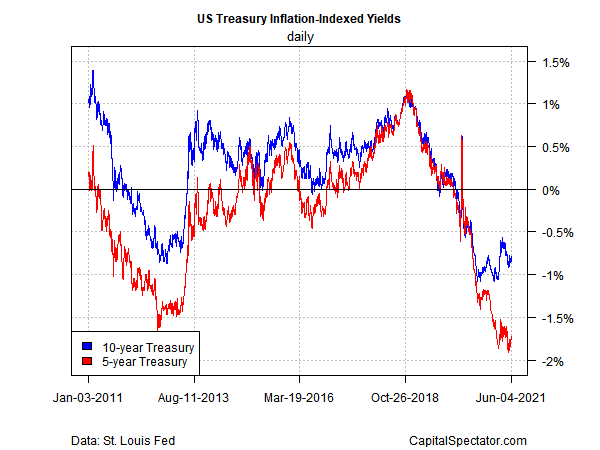

After a notable rebound from pandemic-related lows, the 10-year Treasury yield is approaching pre-COVID-19 levels that were prevalent before early 2020. However, the rate has been relatively stable over the past two months, leading to questions about future movements.

* GOP senators are poised to propose a $1 trillion infrastructure counteroffer to President Biden.

* Exxon faces challenges regarding climate issues from an activist investor.

* Is money supply the crucial element impacting gold prices?

* The US Consumer Confidence Index declined for the first time in six months in May.

* New US home sales dropped more than anticipated in April.

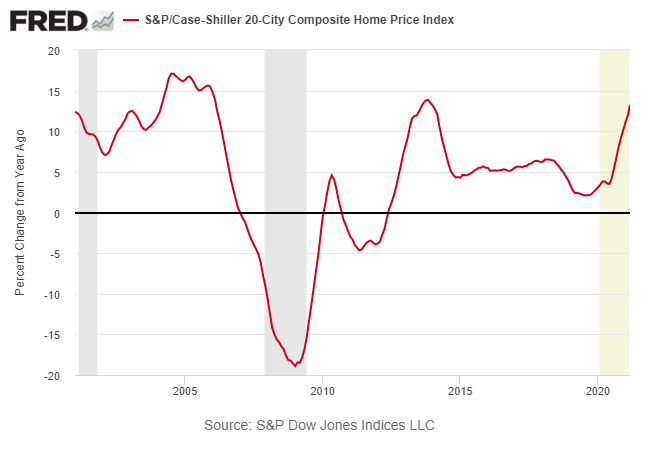

* The year-over-year change in US house prices reached a 15-year high in March:

Earlier this month, I explored a model that estimates a theoretical level for the crucial 10-year Treasury yield. In this follow-up, I will examine a second model for added perspective.

* The EU and US have jointly imposed new sanctions on Belarus following the forced landing of a jet.

* CNN’s Back-To-Normal Index indicates that the US economy is approaching full recovery.

* Vaccinated Americans have not yet emerged as a robust driving force behind the economic rebound.

* Amazon is reportedly close to acquiring MGM studio.

* The Chinese currency has risen to a three-year high against the US dollar.

* There are concerns that the focus on inflation might be overshadowing the risks of escalating US-China tensions.

* The German economy contracted more than expected in the first quarter.

* German businesses have shown increased optimism regarding economic conditions in May.

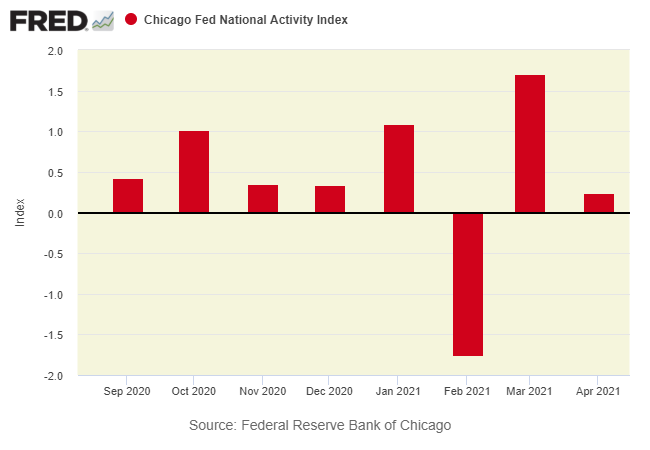

* US growth cooled in April following a surge in March, according to the Chicago Fed National Activity Index:

Last week, both foreign and US property stocks surged, achieving the highest gains among the major asset classes, as evidenced by a range of exchange-traded funds up to Friday, May 21.

Continue reading

* Belarus has forced a passenger airliner to land and arrested an opposition journalist.

* A bipartisan group of senators has reached a consensus on infrastructure spending.

* President Biden’s agenda enters a critical phase as it faces ambitious goals.

* Will consumers maintain their spending as economies reopen?

* New daily COVID-19 cases in the US have fallen to a one-year low.

* Existing home sales in the US declined for the third month in a row in April.

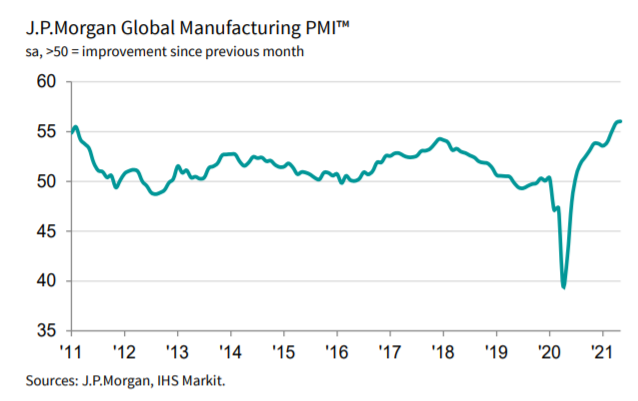

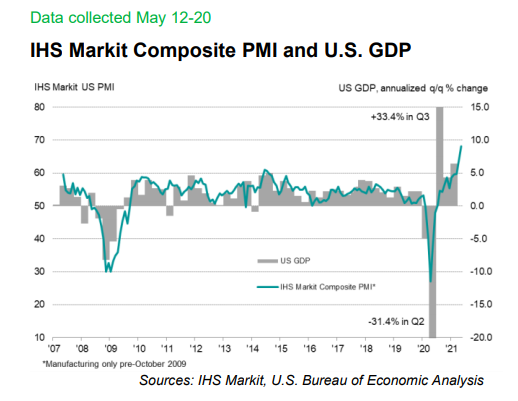

* US economic growth is showing signs of acceleration in May:

Global markets experienced a mixed but largely calm week through Friday, May 21. This tranquility also influenced our proprietary strategies, which remained relatively stable during the week.