The US economy is projected to experience a slowdown in growth during the third quarter. However, early estimates of GDP indicate that this decline is likely to be relatively mild.

* President Biden addresses the tumultuous collapse of the Afghan government.

* With valuable rare earth metals at stake, China may partner with the Taliban.

* Five US states set new records for daily Covid cases.

* The US announces historic cuts to Colorado River water usage.

* China introduces new regulations to tighten control over its tech industry.

* Revised Eurozone GDP figures for Q2 confirm a 2% growth rate.

* The NY Fed Manufacturing Index indicates substantially slower growth in August.

* The yield on US 10-year bonds declines to 1.26%, reaching a seven-day low:

International real estate stocks outside the US, along with companies from developed markets abroad, led performance among the major asset classes for the trading week ending August 13, according to a range of ETFs.

* Scenes of chaos at Kabul airport as the Taliban seize control of Afghanistan.

* The Biden administration faces criticism as Afghanistan falls under Taliban rule.

* The collapse of Afghanistan creates new challenges for the US and its allies.

* Global economic risks from shipping disruptions continue to rise.

* The Delta variant impacts demand and increases costs for businesses.

* There is growing support within the Fed for announcing tapering of bond purchases in September, which might occur.

* Retail spending and industrial output in China are weaker than anticipated for July.

* Japan’s economy grew faster than expected in the second quarter.

* Short-seller firm Hindenburg Research is making headlines for its recent activities.

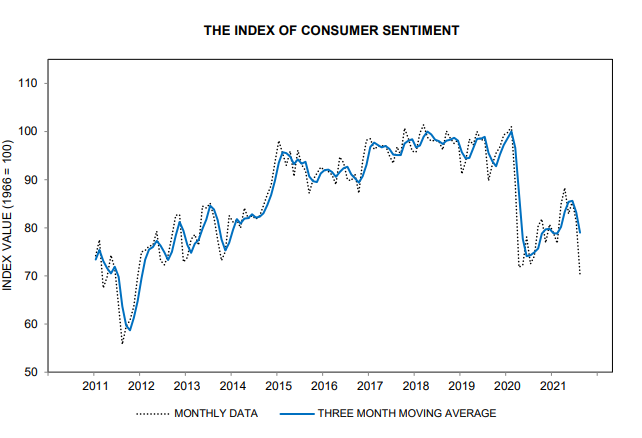

* US consumer sentiment drops to a ten-year low in early August:

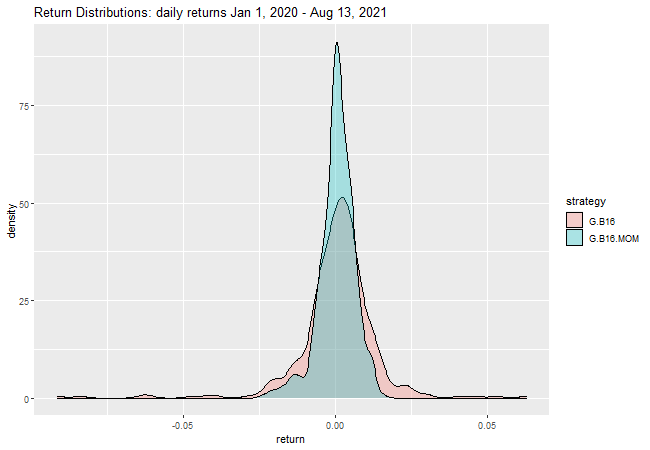

Our collection of proprietary strategies made notable strides last week in narrowing the performance gap compared to the benchmark this year. Though there remains much work ahead, it’s encouraging to see that two out of the three strategies have aligned with the benchmark, and one has even surpassed it.

Tom Standage

Review via The Wall Street Journal

Tom Standage, deputy editor of the Economist, has carved out a niche in exploring the evolution of technology, observing its historical context while contemplating future implications. In his latest book, “A Brief History of Motion: From the Wheel, to the Car, to What Comes Next,” he presents a fascinating account—though it may not reach the heights of his previous works. Nevertheless, akin to all of Standage’s books, it offers deep insights, well-crafted prose, and intriguing details that are sure to engage readers.

- European shares are experiencing a bull market surge

- US stocks close the week at yet another record high

- All of our strategy benchmarks show robust gains this week

Europe is heating up: And it’s not just the weather. Regions across Europe are seeing soaring temperatures, with Sicily breaking records at a blistering 119.8 degrees Fahrenheit this week.

Decomposing Momentum: Eliminating its Crash Component

Pascal Büsing (University of Muenster), et al.

July 15, 2021

This paper proposes a cross-sectional momentum strategy that mitigates crash risks and is independent of market conditions. By dividing the standard momentum return from months t-12 to t-2, based on the highest stock price during this period, both resulting return components independently forecast subsequent returns. However, the long-short returns from the first component completely avoid negative skewness, as crashes in momentum are driven solely by the second component.

* The Supreme Court upholds Indiana University’s vaccine mandate.

* The UK’s Defence Secretary warns that Afghanistan is at risk of becoming a ‘failed state’.

* Home prices in the US surge across the nation.

* Economists predict that the Fed will announce a tapering plan in September.

* Disney reports better-than-expected earnings for Q3.

* Recent severe weather events result in significant first-half losses for insurers.

* Growth forecasts for China have been adjusted downward due to the Delta variant surge.

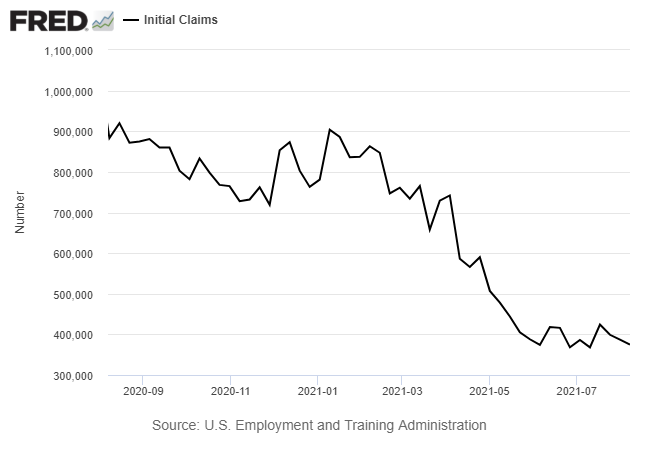

* US jobless claims declined for the third consecutive week:

The US Macro Trend Index (MTI) tracks the strength of economic activity trends within the country. This index is formulated through analysis of two business cycle indicators: the ADS Index from the Philadelphia Fed and the Weekly Economic Index (WEI) from the New York Fed. Each indicator takes a unique approach to assess US economic performance in real-time using various indicators reported at daily and weekly intervals. MTI’s goal is to measure both deceleration and acceleration in the overall macroeconomic trend through the ADS and WEI. It is important to note that MTI is not a direct measure of economic growth or contraction; rather, it quantifies the strength or weakness of the current economic trend.

MTI serves as a useful framework for evaluating the prevailing strength of the economic trend and gauging how it evolves over time.

The MTI computation involves:

1. Calculating the mean of the 1-, 2-, 5-, and 10-period differences for the ADS Index.

2. Calculating the mean of the 1- and 2-period differences for the WEI.

3. Averaging the two results and transforming them into Z-scores on a rolling one-year basis.