Recent market developments have sparked significant attention across various sectors:

- The 10-year US Treasury yield has reached a two-year high in early trading on Tuesday.

- A preliminary study from Israel indicates that a fourth vaccine dose is insufficient to halt omicron infections.

- The UK is set to send missiles to Ukraine, preparing for possible aggression from Russia.

- Analysts claim US engagement policy with North Korea may be misguided, according to expert opinions.

- China’s Xi advises Western nations against hiking interest rates too hastily.

- US airlines are calling for ‘immediate intervention’ regarding the planned rollout of 5G, as reported.

- Oil prices have surged to a seven-year high amid fresh supply concerns:

In the previous week’s trading, emerging markets dominated the performance leaderboard in a generally diverse set of major asset classes, according to a collection of ETFs by the close on Friday (January 14).

Current economic conditions reflect several critical trends:

- Omicron and inflation are impacting the outlook for the US economy.

- China’s strict Covid policy presents a risk for global manufacturing.

- China’s GDP increased by 4.0% in Q4 year-over-year, marking the slowest growth in almost two years.

- In response to growth concerns, the China central bank has lowered interest rates.

- Oil prices are approaching the highest levels seen in over six years.

- North Korea has launched two missiles, marking its fourth test this month.

- This week focuses on Q4 earnings: Will value and cyclical stocks outperform tech?

- US retail sales declined in December (adjusted), although unadjusted figures show a surge:

by Christopher Leonard

Excerpt via Politico

Between 2008 and 2014, the Federal Reserve printed more than $3.5 trillion in new bills, roughly three times the amount created in the Fed’s first 95 years. This rapid expansion of the money supply fueled asset demand in various markets, resulting in price surges. Notably, Hoenig was one Fed leader who consistently opposed this strategy, beginning in 2010, challenging then-chair Ben Bernanke’s widely praised rescue plans.

The Time-Varying Relation between Stock Returns and Monetary Variables

by David G. McMillan (University of Stirling)

November 2, 2021

While the relationship between stock returns and key monetary values—such as interest rates, inflation, and money supply growth—has been extensively analyzed, it lacks clarity. We argue that this relationship shifts over time, largely due to shocks. Notably, the correlation between stock returns and these variables undergoes significant changes. A previously negative relationship with bond yields and inflation can turn positive, while the opposite occurs for money supply growth. This change began with the burst of the dot-com bubble and worsened during the financial crisis. Predictive regressions also signal shifts in behavior, indicating that while typically, higher yields, inflation, and money growth reduce returns, these factors may support the market during stress. After the financial crisis, higher inflation and money growth consistently exhibited positive predictive power, altering perceptions of risk.

Several notable developments have occurred recently:

- The Supreme Court blocked Biden’s vaccine mandate for large companies.

- Russia declared that discussions on Ukraine have reached a ‘dead end’.

- A cyberattack has disrupted government websites in Ukraine.

- Omicron has led economists to revise the US growth outlook for Q1 down.

- Wall Street veteran known as “Dr. Doom” criticizes Fed policies regarding inflation.

- China’s trade surplus with the US increased for the second consecutive year in 2021.

- The IEA warns that a global surge in energy demand may lead to increased market volatility.

- US producer price inflation rose 9.7% last year, the highest rate since 2010.

- Weekly jobless claims increased last week to their highest level since November:

Is January trading in the US stock market indicative of trends for the entire year? If this is the case, sectors related to energy and high dividend yields will likely see favorable performance throughout 2022, thanks to their robust growth this month, as indicated by various ETFs.

Fed’s Lael Brainard is poised to inform Congress that maintaining focus on inflation reduction is imperative. Analysts advise seeking companies with strong pricing power to serve as an inflation hedge, as inflation trends are expected to persist. Furthermore, the US economy reportedly grew at a modest pace in the final weeks of 2021, according to the Fed’s Beige Book.

IEA attributes the worsening natural gas crisis in Europe to Russia, while reports indicate that grocery store shortages are surfacing again due to multiple factors. Firms are maintaining steady year-ahead inflation expectations of 3.4% on average for January. Analysts predict that the oil rally could extend into 2022, as US consumer inflation accelerated to 7% in December, the highest level in 40 years:

The US economy appears set for a notable rebound in the upcoming fourth-quarter GDP report, expected on January 27. However, anticipated macroeconomic challenges may temper growth momentum in early 2022.

Looking forward, the World Bank projects a slowdown in global economic growth for 2022 compared to last year, with several key highlights:

- Fed Chair Powell indicated to Senators that inflation poses a ‘severe threat’ to jobs.

- Signs suggest Omicron may be peaking in the US and UK.

- Powell also conveyed that the US economy no longer requires aggressive stimulus measures.

- Central banks are identified as the primary risk factor for the global economy in 2022.

- Russia continues to cause uncertainty regarding Ukraine, which seems to be part of their strategy.

- US consumers are seeing a return of debt-fueled spending trends.

- China’s inflation has moderated in December.

- In November, Eurozone industrial output increased despite ongoing supply chain issues.

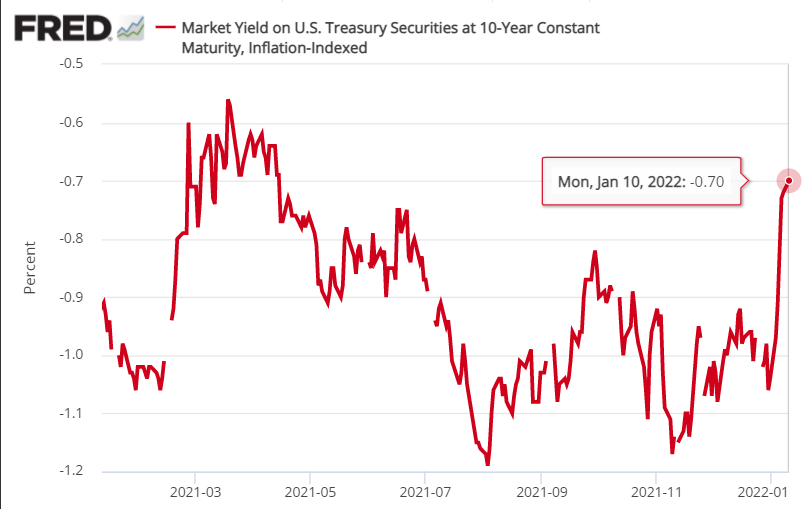

- The US real yield for 10-year inflation-indexed Treasuries has rose to a nine-month high:

Conclusion

As we navigate through these dynamic economic headlines, it’s evident that various sectors and trends are shaping market behaviors. Observing these developments can provide valuable insights for investors and analysts alike, as they prepare for potential market shifts in the near future.