In recent times, various global issues have left analysts contemplating their potential impacts:

- NATO leaders express concerns regarding the unpredictable outcome of the Ukraine conflict.

- The US intelligence chief claims that Putin is gearing up for a prolonged struggle in Ukraine.

- Federal Reserve officials reflect on the slow response to soaring inflation.

- Household debt in the US surged in Q1, marking the largest single-quarter rise since 2006, according to reports.

- US gasoline prices have hit a record high.

- China’s consumer inflation reached a 5-month peak in April, rising by 2.1% reports indicate.

- The impending wheat harvest in China raises concerns for global food prices.

- Could oil stocks become the next big thing like FAANG?

- UST, a ‘stablecoin’ designed to hold a $1 value, has dropped significantly.

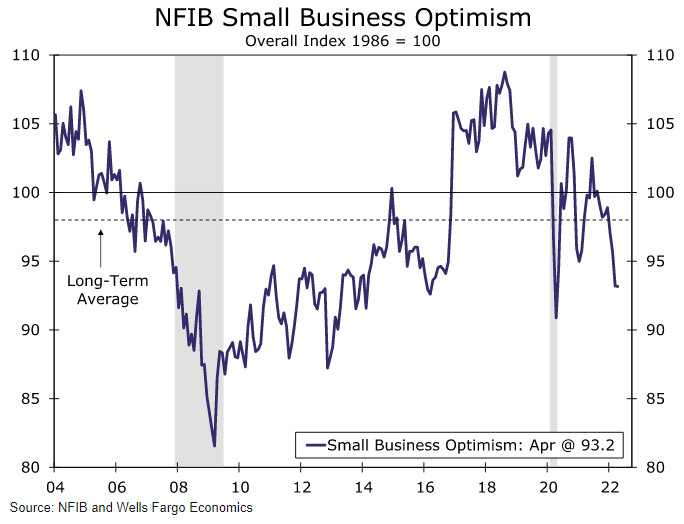

- Small business sentiment in the US for April remains below the long-term average.

There’s little refuge within the US equities market, especially when considering risk factors. Yet, value stocks have surprisingly fared well, showing only marginal losses this year. The pressing questions are: Will this trend continue? Can value stocks eventually regain their historical edge and surpass growth stocks with enhanced returns? Or is the historical advantage of value stocks fading into a continual cycle of underperformance?

Key updates highlight the current global economic landscape:

- President Biden implores Congress to expedite approval of a new aid package for Ukraine.

- Biden is concerned that Putin lacks a strategic exit plan for the war.

- Germany readies for an abrupt halt to Russian gas supplies.

- Government retirement funds are experiencing challenges this year, with expectations of further declines.

- Emerging market currencies are suffering due to rising interest rates and sluggish growth.

- The consumer inflation outlook in April has dropped from last month’s record high.

- Concerns grow that the US housing market may resemble a bubble or is heading in that direction.

- Bitcoin trades below $30,000 for the first time since last July.

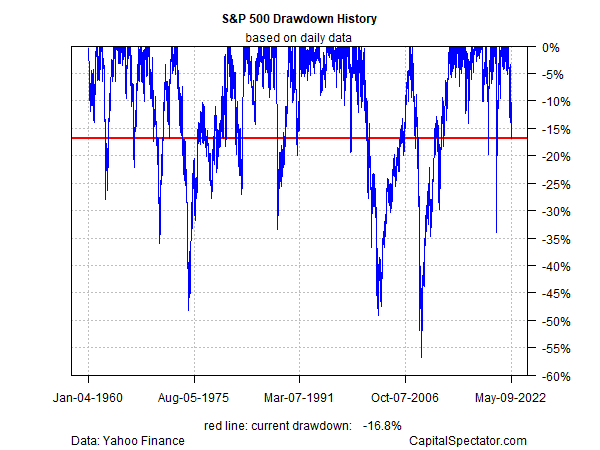

- The S&P 500 Index’s drawdown has plunged to -16.8%, marking its steepest decline in two years:

The recent week ending May 6 brought considerable turmoil to major asset classes, with commodities being a notable exception. Following a modest pullback in the latter half of April, raw materials rebounded in the first week of May amidst a broad market selloff, supported by data from a range of ETF proxies.

Key highlights from recent developments include:

- Putin asserts that the West instigated Russia’s invasion of Ukraine during his ‘Victory Day’ address.

- China’s exports faced a setback, with growth slowing to a two-year low in April.

- Ferdinand Marcos Jr. is projected to win the Philippines’ presidential election.

- In March 2022, US consumer debt levels rose significantly, primarily due to increased credit card spending.

- Increasing interest rates present a double-edged sword for banks.

- In the US, the strength of the dollar is resulting in winners and losers.

- Analysts suggest that the outlook for a soft US economic landing might be more favorable than earlier anticipated, according to analysis.

- The five-year US Treasury yield hit its highest level since 2008 in Monday trading.

- The US Dollar Index reached a new 20-year high in early trading:

● What You Don’t Know: AI’s Unseen Influence on Your Life and How to Take Back Control

Cortnie Abercrombie

Summary via publisher (Narrow Gauge Books)

This book reveals the hidden dynamics at play that label, track, and influence your life decisions, from employment to healthcare, highlighting the pressing need for awareness and understanding of these AI systems that pervade our everyday lives—shaping key areas of existence, relationships, and freedoms.

As recession fears mount, expectations for the US economy are increasingly turbulent, prompting a need for a reevaluation of financial conditions. In times of rising macro risks, early indicators can surface that signal shifting financial climates. With the Federal Reserve set on an aggressive strategy to raise interest rates to combat inflation, it is crucial to monitor these evolving financial conditions.

Recent developments have sparked significant discussions across various sectors:

- A leaked Supreme Court draft opinion indicates a potential revision of established precedents.

- Global economic growth dropped to a 22-month low in April, as reported by a PMI survey.

- World food prices declined slightly in April following record highs.

- Analysts believe that slowing growth in China and rising global rates present significant challenges, according to reports.

- Several blue-chip CEOs predict a considerable recession looming in Europe, highlighting concerns.

- The German 10-year yield has risen to its highest level since 2014.

- Argentina’s central bank prohibited cryptocurrency transactions in domestic banks.

- Globalization remains crucial for major US corporations.

- US worker productivity declined at the sharpest rate since 1947.

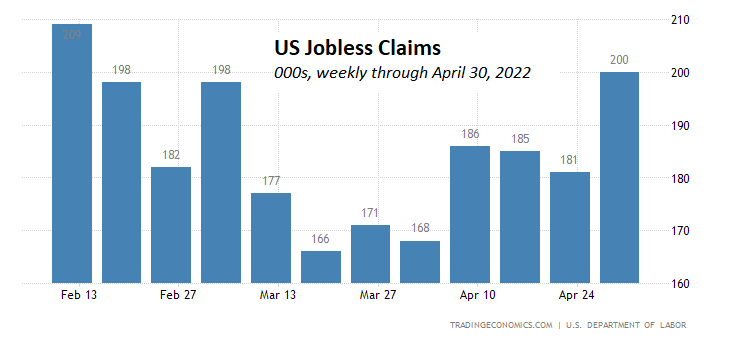

- US jobless claims have increased to their highest level since February:

As anticipated, the Federal Reserve has raised its policy rate by 50 basis points, now ranging from 0.75% to 1.0%, indicating its commitment to combating inflation. However, substantial challenges remain ahead, and the Fed is still playing catch-up as inflation remains consistently high. The crucial question remains: Will the Fed see a relief as inflation begins to stabilize?

Looking ahead, analysts are voicing concerns about potential risks of further escalations in the Russia-Ukraine conflict:

- The US 10-year Treasury yield has retreated from the 3.0% mark after the Fed’s rate hike.

- Rate increases in the US are expected to impact foreign economies adversely.

- A declining US jobless rate might complicate the Fed’s approach to managing inflation.

- A surge in energy prices propelled oil giant Shell’s quarterly profits to a 14-year peak.

- European firms are reconsidering their investments in China.

- China’s economic contraction deepened in April according to PMI data.

- German factory orders fell for the second consecutive month, marking the most significant drop in five months.

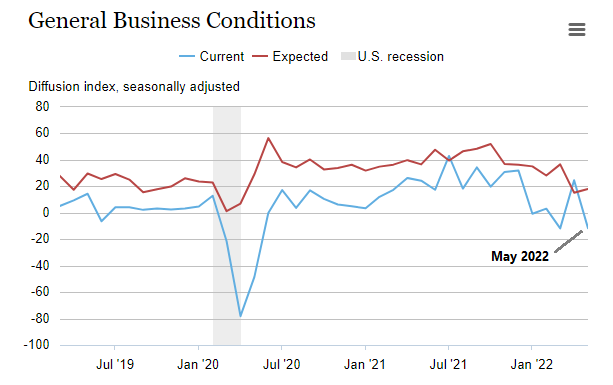

- The US ISM Services Index declined in April, though it still indicates solid growth.

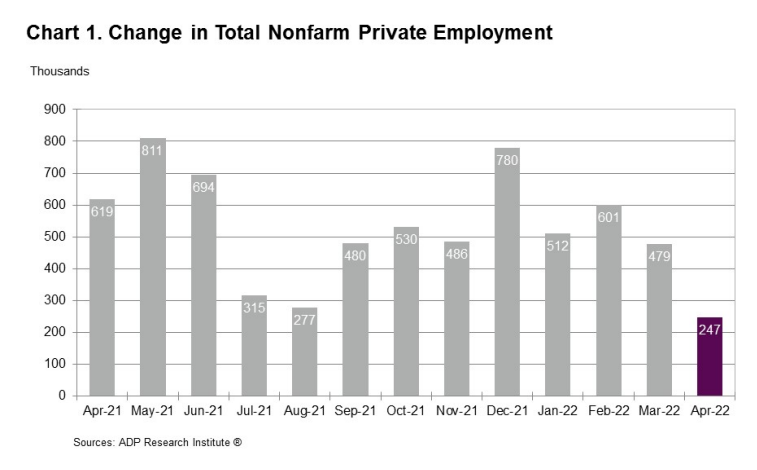

- Hiring at US companies slowed more than expected in April: