The Factor Multiverse: The Role of Interest Rates in Factor Discovery

Jules H. van Binsbergen (University of Pennsylvania), et al.

September 2022

This study delves into how the decline in interest rates has influenced the identification of asset pricing anomalies. We analyze 153 known anomalies alongside 1,395 potential but undiscovered anomalies. Our findings suggest that without the decline in interest rates, the current asset pricing literature would likely focus on a different set of anomalies. As interest rates continue to remain steady rather than decline, a reassessment of relevant anomalies is necessary. We apply a duration-based adjustment method for interest rates to categorize anomalies as false positives, false negatives, or those resilient against fluctuating interest rates. Our findings reveal that the factor discovery process is particularly sensitive to the economic conditions of this specific timeframe.

* President Biden indicates that the risk of nuclear war is at its highest since the Cuban Missile Crisis in 1962.

* IMF chief cautions about escalating recession risks in the global economy.

* Federal Reserve officials continue advocating for higher interest rates.

* A potential debt crisis is developing in emerging markets.

* Economist Paul Krugman suggests that the US economy may be “rolling over,” writes about this issue.

* World currency reserves are decreasing at an unprecedented rate.

* Signs of a new Covid surge may be on the horizon.

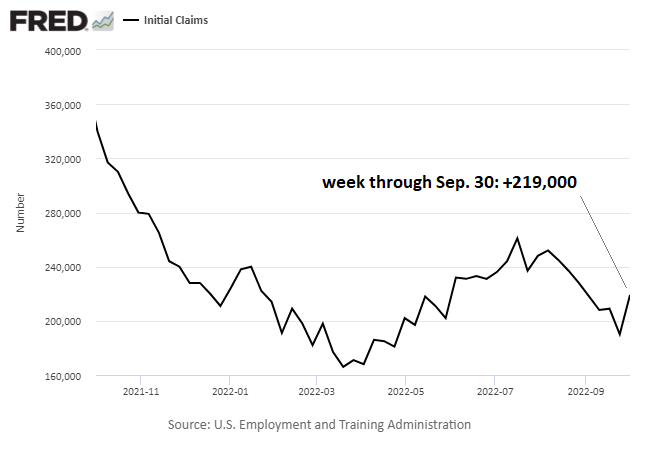

* US jobless claims have risen to a 5-week high, yet remain historically low:

When might the Federal Reserve halt its interest rate hikes and loosen its policy? The answer is uncertain, even for the Fed, largely due to the unpredictable nature of inflation. However, there are numerous options to interpret emerging signals. Let’s explore insights from some familiar analysts.

* North Korea continues to launch missiles while the US redeploys its carrier.

* OPEC+ approves significant reductions in oil production to stabilize prices.

* Global economic activity declined for the second consecutive month in September.

* A sharp slowdown in global trade is predicted by the WTO according to forecasts.

* US hiring surged in September, as per data from ADP.

* Developing nations relying on Chinese loans may encounter obstacles as growth diminishes.

* The US Services PMI indicates a decline in business activity for the third month in September, yet…

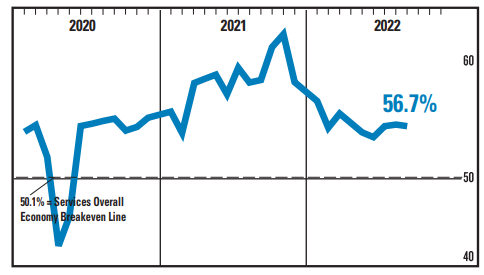

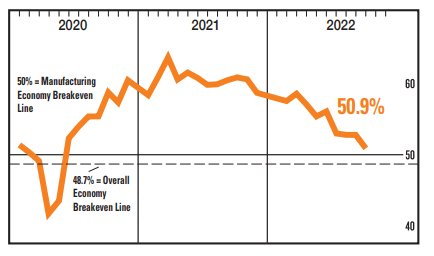

* The ISM Services Index dropped in September but continues to reflect strong growth:

The slowdown in US economic growth has not yet crossed the threshold into a recession, but forecasts indicate that the expansion may stall as soon as November, according to recent projections from a report on proprietary indicators published in The US Business Cycle Risk Report.

* The White House attempts to persuade Saudi Arabia against reducing oil production.

* OPEC+ seems poised for significant cuts in its oil output targets.

* President Putin officially annexes regions in Ukraine.

* The US national debt has exceeded $31 trillion for the first time.

* Reasons why the Fed might not be quick to ease its rate hikes.

* An economist warns that an unprecedented global deflationary cycle has commenced.

* US factory orders remained flat in August.

* China faces significant challenges that may impede its economic growth.

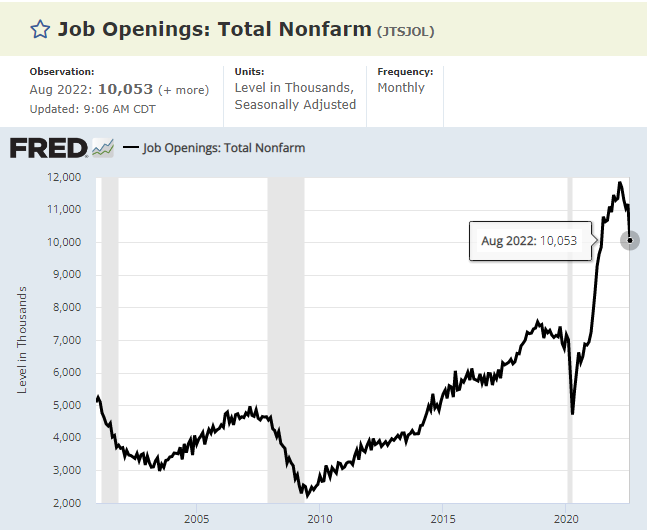

* US job openings declined sharply in August, hitting a 13-month low:

The long-term expected returns for risk assets appear increasingly compelling following substantial downturns in global markets, based on assessments from multiple models utilized by CapitalSpectator.com.

* North Korea launches a missile over Japan, escalating tensions.

* A United Nations agency urges the Fed and other central banks to pause rate hikes.

* Experts suggest that pipeline sabotage serves as a warning to the West from Putin, analysis indicates.

* Oil prices may rise to $100 per barrel as OPEC+ considers cuts in production.

* Global manufacturing contracted in September, according to PMI survey results.

* Construction spending in the US declined in August, marking its most significant drop in over a year and a half.

* The US Manufacturing PMI in September indicates “renewed expansion”; however…

* The US ISM Manufacturing Index is nearing the no-growth threshold in September:

In September, the major asset classes endured another series of significant monthly losses, as revealed by various proxy ETFs. Once again, no asset class was spared—except for cash. The overall trend continues to reflect a pattern of declining values, similar to that of August.

* Brazil’s contentious presidential election advances to a second round.

* UK Prime Minister Truss reverses her stance on tax cuts after market upheaval.

* OPEC+ weighs production cuts following a slump in oil prices.

* Ukraine continues reclaiming territory.

* Some Federal Reserve officials are beginning to question the policy of rate hikes.

* The global natural gas market is expected to remain tight in 2023, as per IEA predictions.

* Concerns about Credit Suisse’s financial health result in a sharp decline in its share prices.

* Investors are rediscovering the benefits of Treasury bills as interest rates rise.

* Consumer spending in the US showed a rebound in August.

* The yield on the US 10-year Treasury rose for the ninth consecutive week through Friday: