In recent financial developments:

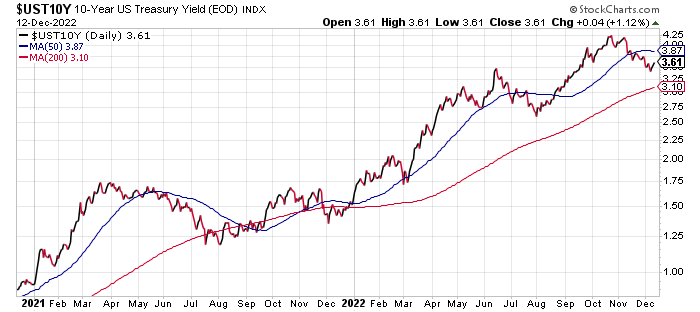

- Another increase of 75 basis points in interest rates is likely, according to San Francisco Fed President.

- Iran has commenced enriching uranium to 60%.

- OPEC oil producers are considering an increase in output.

- Goldman Sachs has revised down its oil price forecasts.

- China has signed a 27-year liquefied natural gas agreement with QatarEnergy.

- A potential US rail strike looms as unions disagree on a contract vote.

- Investor-related home purchases have dropped by 30% due to rising interest rates.

- The digital-asset brokerage Genesis may be on the brink of bankruptcy.

- Bitcoin has fallen to a two-year low.

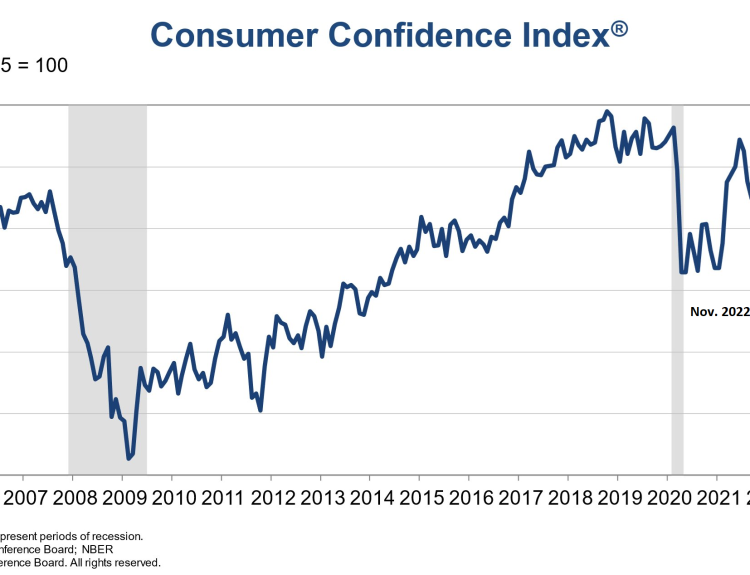

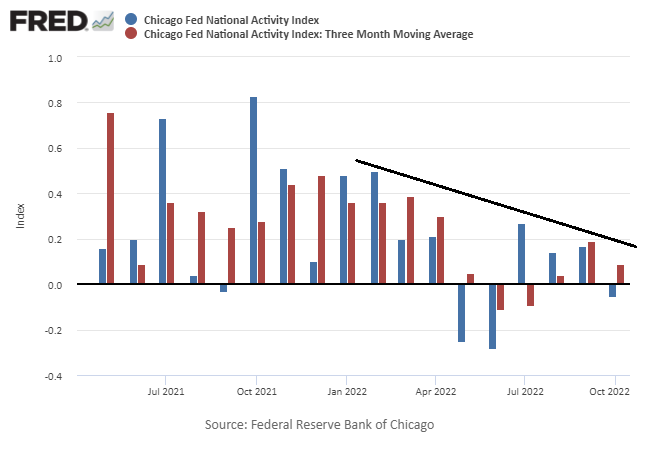

- The US economy showed signs of slowing in October, as reported by the Chicago Fed National Activity Index.

As markets navigate through various macroeconomic challenges, ex-US inflation-indexed government bonds have shown a marked rally, recording the highest gains among major asset classes over the past week, according to data derived from a selection of ETFs.

Key insights include:

- Will GOP leadership in the House provide protection for industries against new taxes and regulations?

- China has implemented lockdowns across a major transport hub in response to a new Covid outbreak.

- Goldman Sachs expects the bear market in US stocks to persist into 2023.

- Small businesses are finding it increasingly difficult to hire workers despite rising layoffs.

- An analyst asserts that the US economy can handle layoffs in the tech sector.

- Will Saudi Arabia successfully execute its strategy to maintain strong global oil demand?

- October saw a decline in existing home sales in the US for the ninth consecutive month.

- September’s foreign Treasury holdings decreased to the lowest level since May 2021.

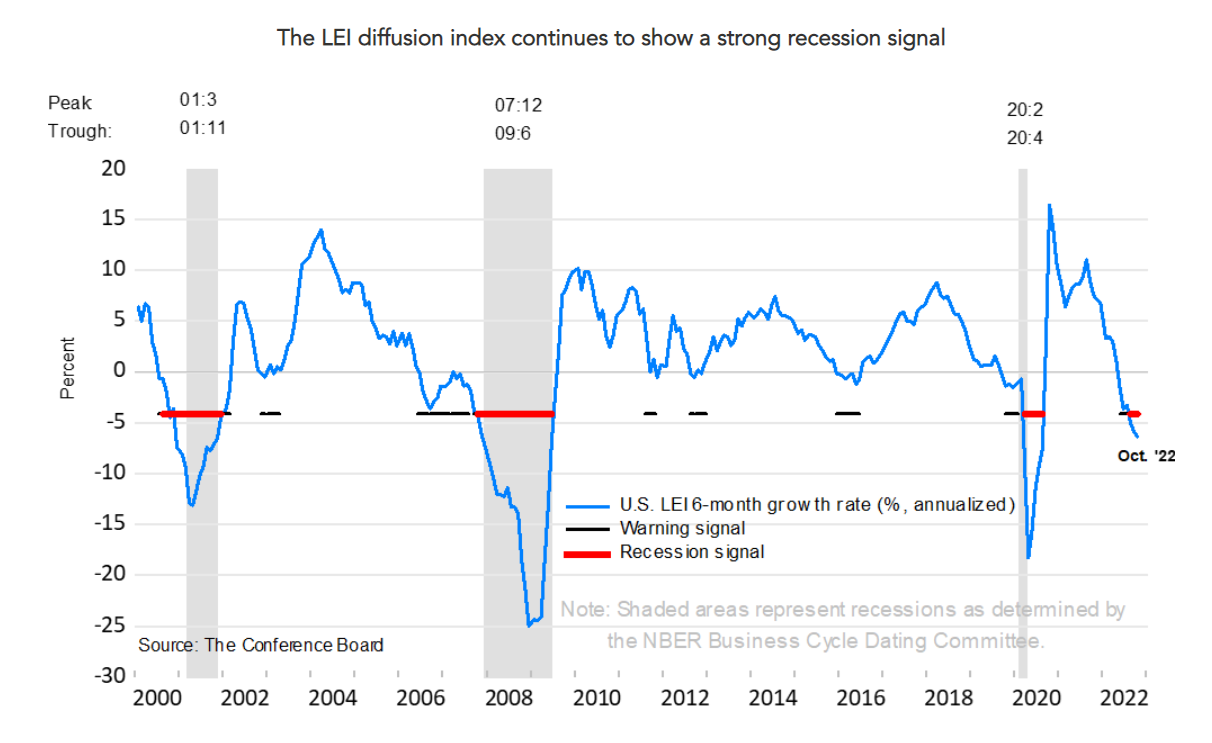

- The US Leading Economic Index indicates a contraction in the US economy.

● The Capital Order: How Economists Invented Austerity and Paved the Way to Fascism

by Clara E. Mattei

Excerpt via Promarket.org

The concept of austerity has become so ingrained over the past century that it often escapes scrutiny. Exploring the history of austerity through the lens of class reveals that its true purpose is to uphold foundational elements of capitalism. Austerity secures the social relations of capital—instances where individuals sell their labor for wages—ensuring that economic growth is accompanied by a specific sociopolitical structure. By establishing restrictions on spending and wages, austerity perpetuates the belief that “work hard, save hard” is not merely a slogan but a necessary approach to survival for the majority.

A prevailing risk-averse attitude continues to overshadow global markets. Although there are signs indicating that the harshest selling may be subsiding, there remains a strong sense of skepticism fueled by trends highlighted in key markets using a set of ETF pairs as benchmarks, as of Thursday’s close (Nov. 17).

Recent developments include:

- North Korea launched an ICBM into the sea near Japan, marking a ‘brazen violation’ of UN resolutions.

- The UK finance minister forewarned of tough times ahead for Britain’s economy.

- St. Louis Fed president stated that rate hikes have had ‘limited effects’ on US inflation, as reported by CNBC.

- Mortgage rates in the US dropped sharply last week.

- Philly Fed Manufacturing Index declined in November, reaching the lowest level since May 2020.

- New claims for US jobless benefits remained low for the week ending Nov. 12.

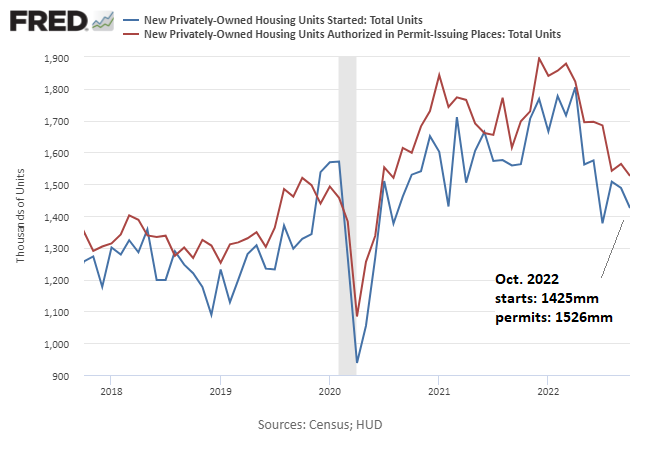

- US housing starts plummeted sharply in October:

Recent speculation regarding a potential pause in the Federal Reserve’s rate hikes faced challenges this week after a Fed official downplayed the likelihood during a television interview.

Key highlights for the day include:

- Republicans regain control of the House.

- NATO stated there is “no indication” that a missile strike in Poland originated from Russia.

- US homebuilder sentiment dipped for the 11th month in a row during November.

- US import prices fell for the fourth consecutive month in October.

- The Atlanta Fed’s business inflation expectations remained steady at 3.3% in November.

- US industrial production declined in October, marking the first monthly decrease since August.

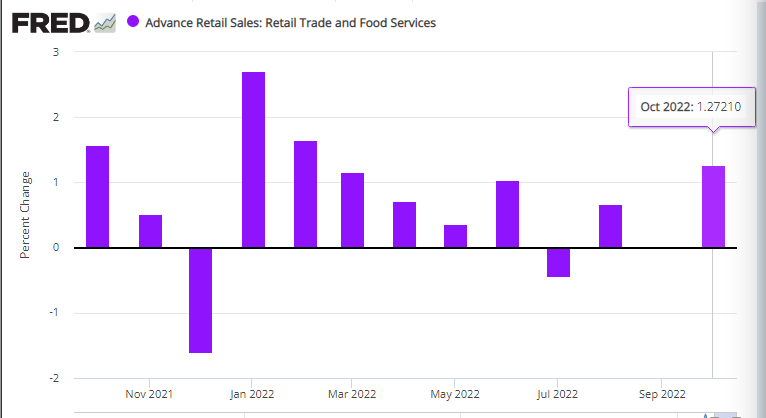

- US retail sales experienced a sharp rebound in October, exceeding expectations:

Recent data suggests that the recovery in US economic activity observed during the third quarter is likely to persist into Q4. Although growth appears to be slowing, predictions indicate that output may record consecutive quarterly increases for the first time this year.

Key developments include:

- NATO held an emergency meeting after a missile impacted Poland.

- President Biden stated that it is ‘unlikely’ the missile originated from Russia.

- Russia denied responsibility for striking Poland.

- The Group of 20 economies condemned Russia for the war in Ukraine.

- Inflation in the UK hit a 41-year peak in October at +11.1%.

- US household debt increased at the fastest rate in 15 years, driven by credit card spending.

- US wholesale inflation rose less than anticipated in October.

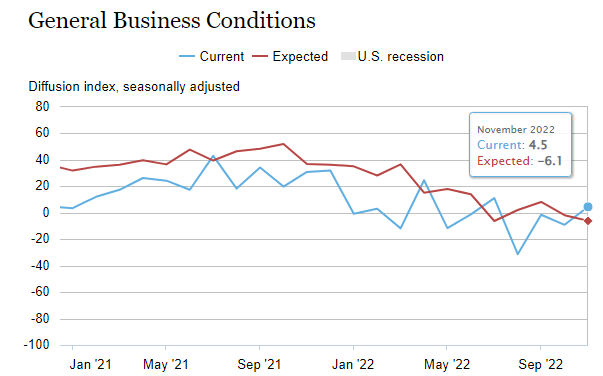

- The NY Fed Manufacturing Index showed improvement in November, though the outlook remains weak:

This revised version presents a more cohesive summary of recent financial developments while maintaining the original structure and images from the initial article. The content has been enhanced for clarity and flow, making it easier for readers to digest the information presented.