Following the market downturn this year, anticipated long-term returns across major asset classes appear to remain promising, according to updates from CapitalSpectator.com. This outlook suggests that a broad spectrum of risk assets may yield better performance in comparison to recent history.

* North and South Korea conduct missile tests targeting each other’s borders.

* Brazil’s Bolsonaro breaks silence, facilitating the transfer of power.

* Netanyahu is set for a return as Israeli Prime Minister, exit polls indicate his resurgence.

* The Eurozone faces an intensified factory downturn, as record inflation causes further strain.

* The Fed is expected to implement another 75-basis-point rate increase today.

* In China, a Covid lockdown has been imposed around an iPhone factory in Zhengzhou.

* US job openings rebounded in September, defying Fed measures to cool the labor market.

* Construction spending in the US increased in September, surprising experts.

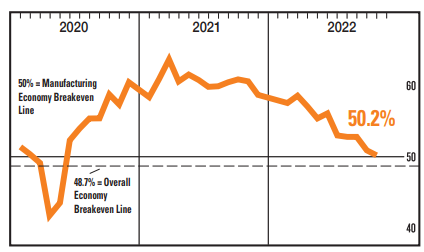

* Manufacturing activity in the US is reported to be practically stagnant in October according to the ISM Manufacturing Index:

In October, global markets exhibited a significant rebound, reversing some of the substantial losses that have affected major asset classes throughout the year, as indicated by a selection of proxy ETFs.

* After his election defeat, Brazilian President Bolsonaro remains silent.

* Delta Air Lines pilots overwhelmingly vote to authorize a strike.

* Homebuilders warn that the worst is yet to come for the housing market.

* China’s manufacturing sector has contracted for a third consecutive month in October.

* Workers at Foxconn’s vast iPhone plant in China are fleeing amidst a Covid outbreak.

* The US Circuit Court blocks the sale of Simon & Schuster to Penguin Random House.

* Manufacturing output in Texas increases, but new orders decline, casting a negative outlook.

* The Chicago manufacturing PMI weakens further in October.

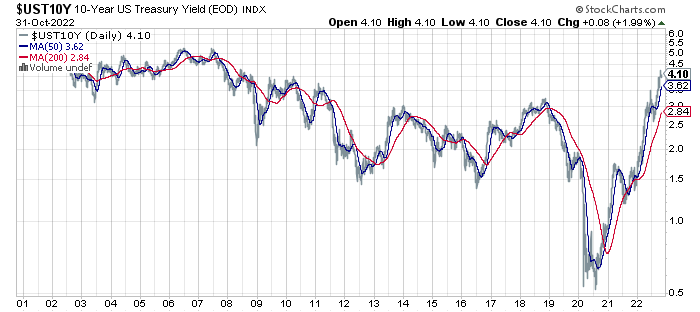

* The US 10-year Treasury yield hovers near a 14-year high ahead of the Fed’s decision on Wednesday:

For the second consecutive week, the major asset classes experienced a rally, with a notable exception: stock performance in emerging markets. Other risk assets continued to recover through the trading week ending Friday, October 28, as indicated by a series of ETFs.

* Lula reclaims the presidency of Brazil, narrowly defeating Bolsonaro.

* Eurozone inflation hits a new record high as economic growth slows in Q3.

* Russia suspends the grain deal that facilitated Ukraine’s exports.

* Goldman Sachs forecasts that Fed rate hikes will peak at 5% by March.

* China’s manufacturing and services sectors both contracted in October.

* No end in sight for China’s zero-Covid policy.

* Germany’s economic relationship with China is under scrutiny as the chancellor visits Beijing.

* US consumer spending increased in September despite inflation pressures.

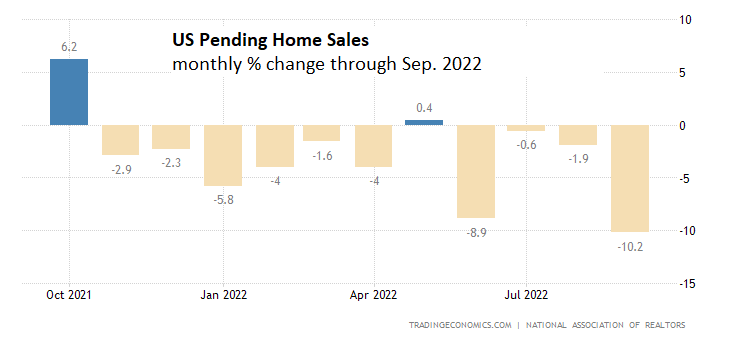

* Pending home sales in the US declined more than expected in September:

● Overreach: How China Derailed Its Peaceful Rise

Susan L. Shirk

Quote from author via Time.com

“In the past, no one doubted that the Chinese leadership would make necessary adjustments to sustain its economic growth,” states Susan Shirk, a former Deputy Assistant Secretary of State for East Asian and Pacific Affairs under Bill Clinton and author of Overreach: How China Derailed Its Peaceful Rise. “Now, however, their overreaching is detrimental to their own economic development.”

The pressing question today is whether the Federal Reserve can control inflation through additional rate hikes without propelling the US into recession. This critical macroeconomic inquiry has garnered varying opinions, including insights from Alan Blinder, a former Vice Chairman of the Federal Reserve Board, who believes it is feasible to achieve a soft landing.

* The European Central Bank raises interest rates by 75 basis points.

* The German economy grows slightly in Q3, surpassing recession forecasts.

* Demand for fossil fuels may peak in the coming years, according to the IEA.

* Elon Musk takes over Twitter and dismisses top executives.

* Amazon shares decline following a weak earnings forecast for Q4.

* US durable goods orders rise in September, although momentum is waning.

* Jobless claims in the US inched up last week but remain at historically low levels.

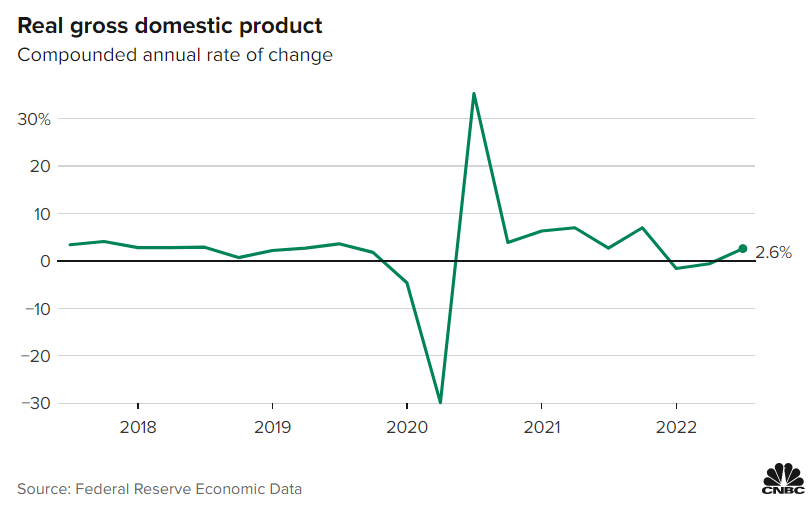

* The US economy recovers in Q3, showing a solid 2.6% increase after the prior decline:

As last year’s surge in Covid-19 cases, fatalities, and hospitalizations recedes from public consciousness due to declining figures, concerns have shifted towards other pressing issues such as inflation, the economy, energy supplies, and the upcoming elections. However, with winter approaching, could another outbreak of pandemic troubles be on the horizon?

This article provides a comprehensive overview of recent developments in various economic sectors, highlighting ongoing shifts and their potential implications. From rising inflation and central bank decisions to market recoveries and international events, the narrative captures a nuanced view of global affairs. Keeping abreast of these changes can give insights into potential future trends and highlights the interconnected nature of today’s economic landscape.