* President Biden is set to visit the eastern NATO flank following his trip to Poland.

* The U.S. may introduce new sanctions against China due to its economic backing of Russia.

* Russia has announced it will halt the last remaining arms control treaty with the U.S.

* Walmart has adopted a cautious stance regarding its economic forecast.

* Amazon has received FTC approval for its acquisition of One Medical health clinics.

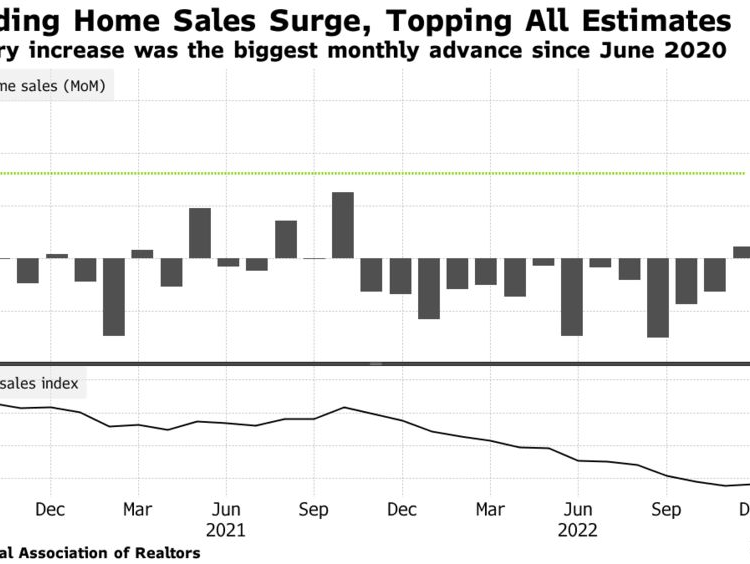

* Existing home sales in the U.S. have seen a decline for the twelfth consecutive month as of January.

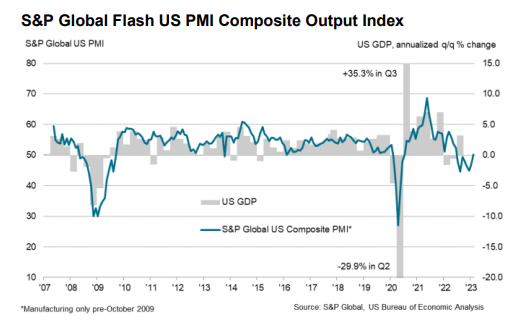

* U.S. business activity has shown signs of recovery in February according to PMI survey data:

The most straightforward opportunities have already been seized. This is evident from the recent performance of the S&P 500 Index, which has rebounded impressively since hitting its October low, registering a 14% increase as of February 17.

* A Supreme Court case might alter immunity standards for large tech firms’ social media platforms.

* China is leveraging its courts to challenge foreign intellectual property rights.

* The Fed’s main inflation metric is anticipated to show higher inflation in the upcoming update.

* Business activities in the Eurozone have experienced an acceleration in February.

* The UK private sector has shown growth in February after a six-month downturn.

* Analysts predict a decline in U.S. corporate earnings for the first and second quarters.

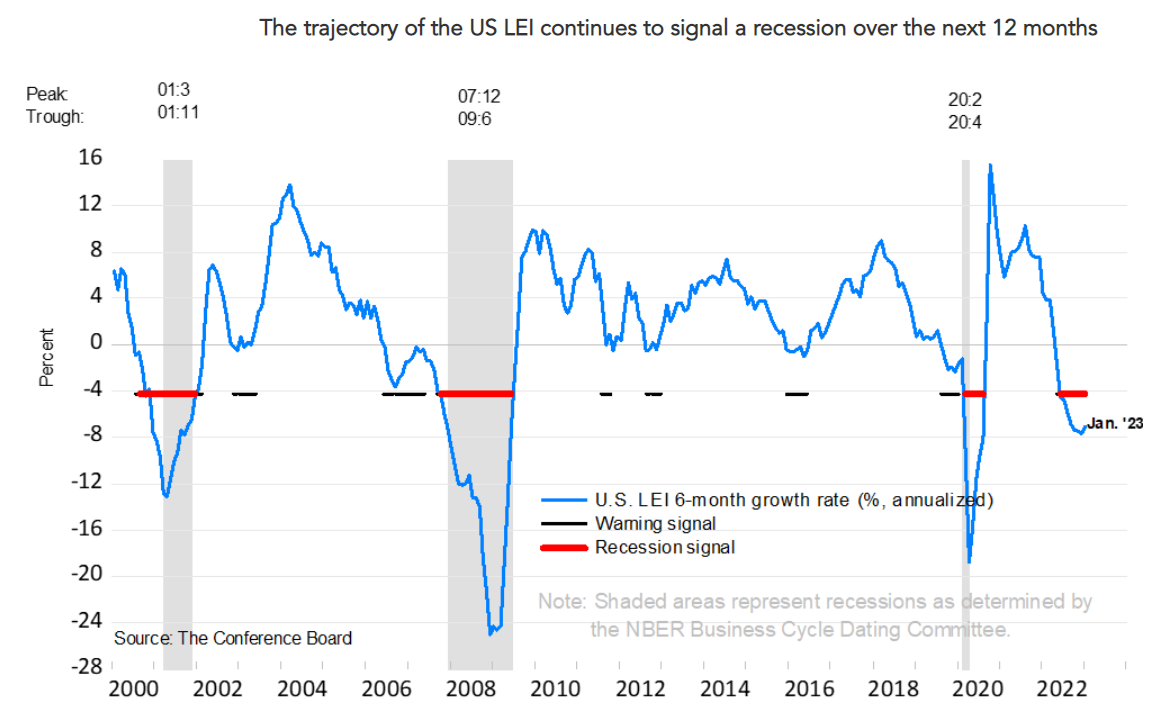

* The U.S. Leading Economic Index continues to indicate a high risk of recession, according to reports from the Conference Board:

“You cannot escape the responsibility of tomorrow by evading it today.”

– Abraham Lincoln

●

Deconstructing Credit Cycles

Steven Ricchiuto

Interview with author via Yahoo Finance

According to Steven Ricchiuto, U.S. chief economist at Mizuho Securities USA LLC in New York, financial markets are currently driven by excessive liquidity during a phase where both bond and equity markets are highly valued. “As awareness grows about the Fed’s prolonged higher rates, even if there’s a pause, the next step is likely to be a rate increase rather than a cut,” he stated.

Submergence = Drawdown Plus Recovery

Dane Rook (Stanford University), et al.

February 2023

While drawdowns and recoveries are often analyzed in isolation, doing so can distort an investor’s perception of risk. This is prevalent enough that a term for the combined occurrence of a drawdown and its recovery is lacking. We propose the term ‘submergence’ for these events and present a new risk metric to assist investors in evaluating such occurrences: submergence density. This metric overcomes the limitations of existing measures and provides flexibility for investors to incorporate their unique risk tolerances, thus enabling a personalized analysis. Moreover, submergence density provides an alternative method for risk-adjusting returns, presenting several advantages over traditional metrics like Sharpe ratios. We apply our new risk-adjustment methodology to key markets, demonstrating its potential for innovative diversification strategies and comparing them against other defenses against submergence risk. We conclude that submergence-based diversification is likely the optimal approach for managing drawdown threats for most investors.

* The Pentagon’s leading official on China is currently visiting Taiwan.

* U.S. mortgage rates have increased for the second consecutive week, with the average 30-year fixed rate reaching 6.32%.

* The U.S. consumer sector is showing indications of resilience.

* Is optimism in financial markets reinforcing the Fed’s hawkish stance on monetary policy?

* Wholesale prices in the U.S. have re-accelerated in January, presenting new inflationary concerns.

* The Philly Fed Manufacturing Index experienced a significant drop in February.

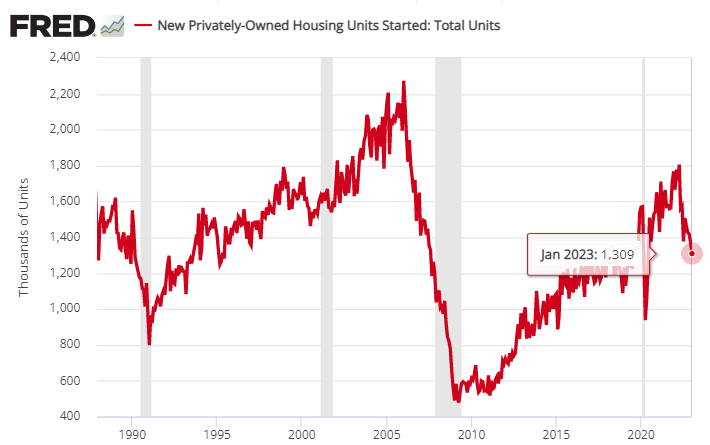

* U.S. housing starts decreased in January, hitting the lowest level since the onset of the pandemic:

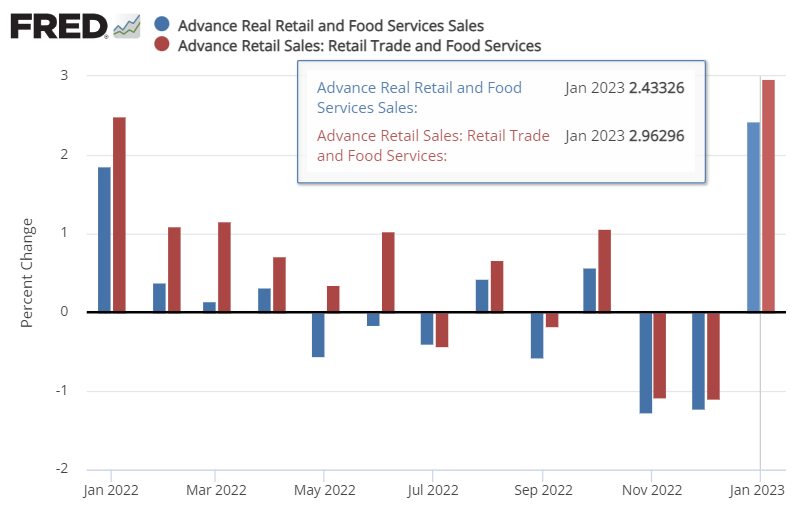

Economists anticipated a considerable rebound in U.S. retail spending for January, but the actual results exceeded even the most positive forecasts. Although a single month can be an anomaly, it currently appears that the Federal Reserve’s efforts to control inflation by slowing economic activity may not be as effective as hoped.

* David Malpass, the troubled World Bank president, will step down early.

* Homebuilder sentiment in the U.S. rebounds sharply in February.

* The Q1 GDP nowcast for the U.S. has been revised upwards to +2.4%, according to the Atlanta Fed’s GDPNow model.

* The U.S. budget deficit is projected to deepen to 6.9% of GDP by 2033, as per CBO estimates.

* The CBO warns that the U.S. might default by July if the debt ceiling dispute is not resolved, as reported WSJ.

* The NY Fed Manufacturing Index has rebounded in February, although it remains in negative territory.

* U.S. industrial production stayed flat in January, but was up 0.8% compared to the previous year.

* Retail sales in the U.S. have surged in January, both in nominal and inflation-adjusted terms:

U.S. consumer inflation is easing, though not as much as expected in January. The recent update suggests that the Federal Reserve may view this as a signal indicating that inflationary pressures are not diminishing quickly enough, potentially strengthening the case for maintaining higher interest rates for an extended period.