As the global financial landscape shifts, several key events and trends are drawing attention:

- * Fed Chair Powell is set to deliver a critical speech on Friday at the Jackson Hole summit.

- * A surge in consumer confidence is central to understanding China’s economic deceleration.

- * Six nations, including Saudi Arabia and Iran, have been invited to join the BRICS group.

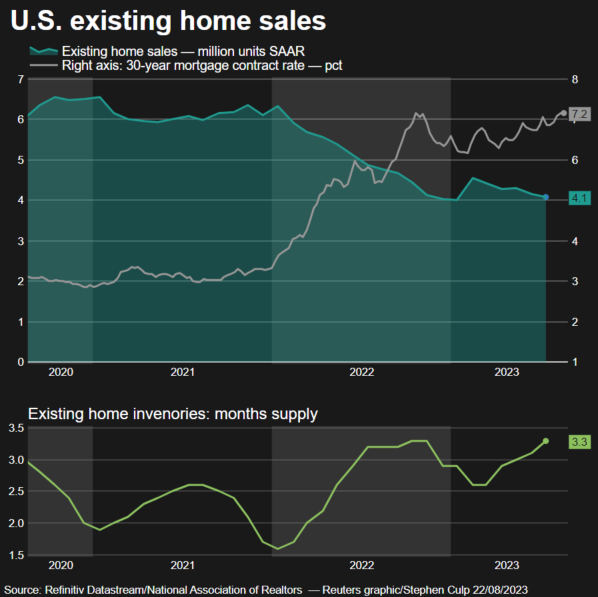

- * New US home sales climbed to a 17-month peak in July.

- * Nvidia’s earnings have surged as demand for its AI-enabled chips spikes.

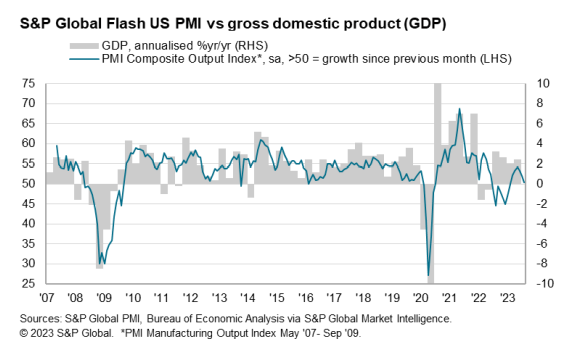

- * August saw a significant slowdown in US business activity, as shown by PMI survey data.

The diversity of equity risk premiums is immense, making it impossible to cover them all in a single article. This wide array presents both a challenge and an opportunity. From a challenge perspective, one must consider how differing modeling approaches can lead to unpredictable stock market forecasts when compared to a “risk-free” rate proxy. While this inconsistency poses problems, aggregating multiple forecasts and using the median value can serve as a valuable strategy—transforming uncertainty into actionable insights.

* Stronger US economic growth necessitates higher interest rates, asserts former St. Louis Fed president.

* The debate over ‘higher-for-longer’ interest rates is expected to dominate discussions at the Fed’s Jackson Hole meeting.

* The eurozone is experiencing a deeper contraction according to August’s Composite PMI survey.

* The BRICS summit is highlighting the topic of de-dollarization, though some analysts deem it a ‘fantasy’, as noted in their commentary.

* The Richmond Fed Manufacturing Index shows that activity continues to be sluggish this August.

* US existing home sales declined again in July as prices rise compared to last year.

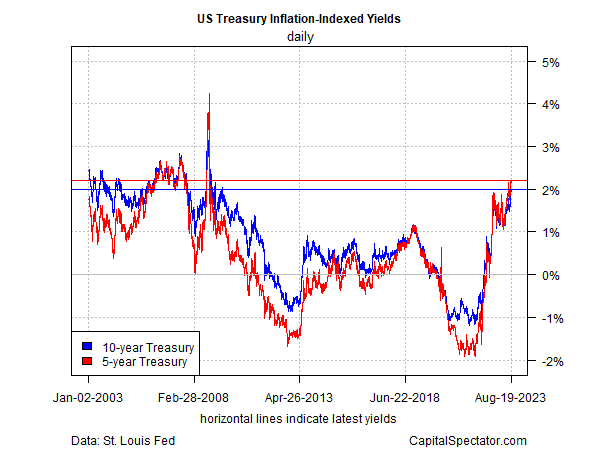

The current climate allows investors to secure real (inflation-adjusted) returns through inflation-protected Treasuries (TIPS), reminiscent of the period following the financial crisis cleanup. The current yields for 5- and 10-year TIPS have returned to previous highs, indicating significant economic and market implications. Below is a brief overview of the recent shifts in inflation-adjusted rates, alongside perspectives from leading analysts.

* Will the resilient US economy slow or halt the recent decline in inflation?

* The risk of a financial crisis in China appears limited for the US.

* Why are bond yields rising again? Here are four potential reasons.

* Following Moody’s lead, S&P has downgraded five banks amid challenging conditions.

* Charles Schwab joins other firms on Wall Street by announcing layoffs.

* Goldman Sachs indicates an increasing risk of a US government shutdown, stating it’s more likely than not this year.

* Real US Treasury yields continue to hover around 14-year highs:

Recent trends in investment have seen a decline across all the major asset classes, signaling a sustained risk-averse sentiment in the market. Investors are currently grappling with the uncertainty of whether this most recent downturn is merely a fluctuation or signifies the end of the rally in risk assets that began in late 2022 and reached its peak last month.

* Has the era of low US interest rates come to an end?

* Natural gas prices are rising amid potential supply disruptions in Australia.

* Analysts suggest that China’s economic model is faltering, and its 40-year growth period may be nearing its conclusion.

* China has reduced its one-year prime loan rate while keeping the five-year rate unchanged.

* Tensions regarding U.S.-China relations appear to be escalating, as relations are set to further devolve.

* Russia and China are poised to further advance their interests at this week’s developing-world summit.

* The US Dollar Index has risen for the fifth consecutive week as the fallout from China’s real estate woes continues to spread.

● The Problem of Twelve: When a Few Financial Institutions Control Everything

John Coates

Summary via publisher (Columbia Global Reports)

The term “problem of twelve” describes a situation where a limited number of institutions exert disproportionate influence over national economics and politics. The major index funds—Vanguard, State Street, Fidelity, and BlackRock—collectively control more than twenty percent of the votes within S&P 500 companies, indicating an unprecedented concentration of power in America. Furthermore, the rise of large private equity firms, including Apollo, Blackstone, Carlyle, and KKR, which have amassed approximately $2.7 trillion in assets, is eroding the credibility and accountability of American capitalism by acquiring public companies and taking them private, thus evading transparency and oversight. This dramatic shift in the economic landscape over recent decades is a significant matter that warrants our attention, as highlighted by Harvard law professor John Coates.

Expanding the Fama-French Factor Model with the Industry Beta

Anatoly B. Schmidt (NYU Tandon School of Engineering)

August 2023

The news-based stock pricing model (NBSPM) has recently outperformed the momentum-enhanced five-factor Fama-French model (FF5M) for key holdings from major US equity sector ETFs, as evidenced both in-sample (Schmidt 2023) and out-of-sample (Schmidt 2022). In this study, the addition of industry beta—determined by returns from relevant sector ETFs—improves the accuracy of FF5M, leading to a new model (FF5MI). This model generally shows better in-sample performance compared to NBSPM when assessing mean squared error, though not necessarily for mean absolute error. Out-of-sample testing indicates that FF5MI is consistently outperformed by NBSPM. This suggests that the industry beta notably influences stock prices, while FF5M factors may lead to an over-fitted model.

* Markets are beginning to comprehend that interest rates may remain elevated for a prolonged period.

* The US Leading Economic Index for July continues to indicate significant recession risks.

* The Philly Fed Manufacturing Index shows signs of recovery in August.

* Chinese property developer Evergrande has filed for bankruptcy in the US.

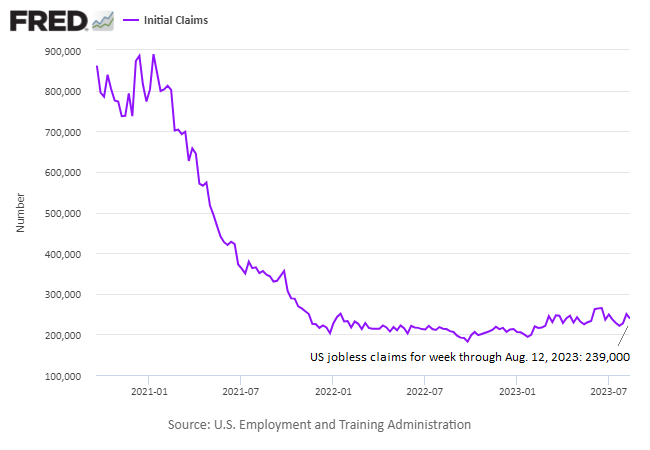

* Recent statistics show that US jobless claims have declined, reflecting resilience in the labor market.