● Poor Charlie’s Almanack: The Essential Wit and Wisdom of Charles T. Munger (revised ed.)

● Poor Charlie’s Almanack: The Essential Wit and Wisdom of Charles T. Munger (revised ed.)

Edited by Peter D. Kaufman

Summary via publisher (Stripe Press)

“Spend each day trying to be a little wiser than you were when you woke up,” advised Charlie Munger in *Poor Charlie’s Almanack*. Originally released in 2005, this collection of 11 talks from the renowned vice-chairman of Berkshire Hathaway has become a cornerstone for investors and entrepreneurs alike. Munger’s insights, infused with his distinctive rhetorical style, draw from his vast knowledge of business, finance, history, philosophy, physics, and ethics, presenting a latticework of mental models that form the foundation of his logical approach to life and decision-making. This essential volume aims to inspire readers to go to sleep a bit wiser than they woke. The abridged edition includes a new foreword by Stripe cofounder and president John Collison.

<p>The US economy is expected to slow in the fourth quarter, yet recent analyses still lean toward a "soft landing" scenario. This outlook suggests that economic output will be robust enough to avoid a recession as defined by the NBER.</p>

<p> <a href="https://www.capitalspectator.com/soft-landing-is-still-plausible-for-us-q4-gdp-nowcasts-suggest/#more-21259" class="more-link">Continue reading <span class="meta-nav">→</span></a></p>

* Biden is poised to veto an anti-electric-vehicle bill.

* Crude oil prices are on track for a seventh consecutive weekly decline.

* The year 2023 is recorded as the least affordable year for homebuying, with 2024 potentially showing improvement.

* Apple plans to produce 25% of iPhones in India within a few years.

* Google launches the first phase of its Gemini AI project.

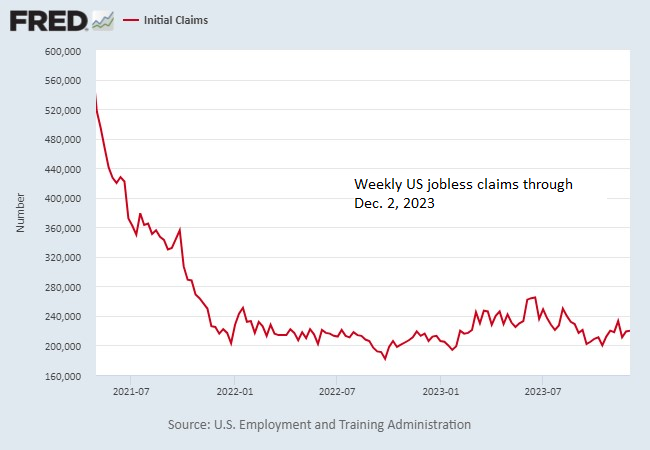

* US jobless claims creep up, yet remain low by historical standards:

<p>Over the past several weeks, the S&P 500 Index has shown strong performance, recovering all of the losses incurred during the summer and fall correction. Currently, the market is trading just below its peak from July. A decisive move above this level could indicate that US equities are positioned to break out from the trading range that has predominated for much of the last two years.</p>

<p> <a href="https://www.capitalspectator.com/is-the-us-stock-market-set-to-break-out-of-its-trading-range/#more-21251" class="more-link">Continue reading <span class="meta-nav">→</span></a></p>

* The House has voted to block Biden emission regulations that favor electric vehicles.

* The US 10-year Treasury yield drops to 4.1%, the lowest since early September.

* The German stock market hits a new record high.

* Moody’s downgrades the outlook for eight Chinese banks.

* China reports a rise in exports for the first time in seven months.

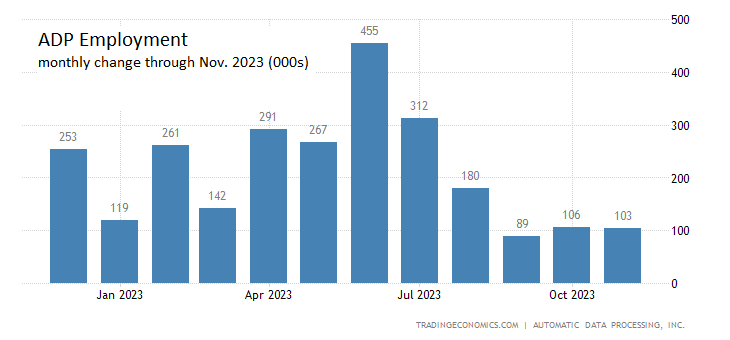

* Private sector jobs in the US increased less than anticipated in November, according to ADP.

<p>Many economists predicted the US would be in a recession by now, but those forecasts have not materialized, as economic output remains positive. In fact, third-quarter GDP surged, challenging notions of an imminent downturn. Rather than reevaluating their stance, recession forecasters have merely adjusted their timelines for the anticipated downturn.</p>

<p> <a href="https://www.capitalspectator.com/despite-us-resilience-recessionistas-still-expect-trouble/#more-21243" class="more-link">Continue reading <span class="meta-nav">→</span></a></p>

* OPEC+ may implement further oil production cuts, says Russia.

* The US will collaborate with other nations to expedite nuclear fusion as a viable energy source.

* Water consumption in technology is rising due to the increasing demand for AI.

* Despite market gains, tax-efficient ETFs are likely to have minimal distributions in 2023.

* The Global Composite PMI, a proxy for GDP, suggests weak growth for November.

* The US ISM Services Index increased in November, indicating moderate growth.

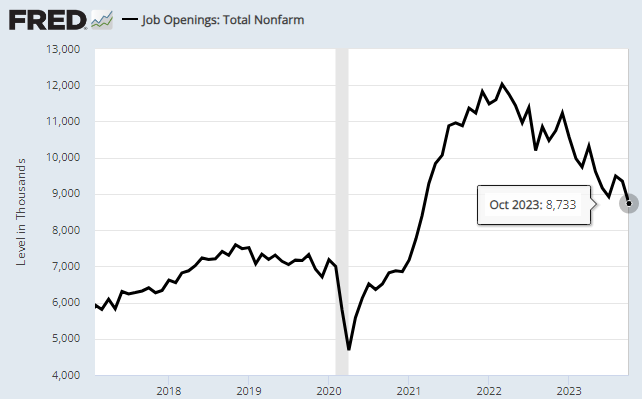

* Job openings in the US dipped in October to their lowest since March 2021:

<p>This year has presented a mixed performance across different equity risk factors. Numerous types of large-cap stocks have stood out as the top performers, as indicated by a selection of ETF proxies through Monday’s close (Dec. 4). While small-cap stocks are on course to lag significantly, the recent resurgence in this segment has led to optimistic predictions that these assets may outperform in the upcoming year.</p>

<p> <a href="https://www.capitalspectator.com/us-large-cap-stocks-remain-2023s-equity-factor-leaders/#more-21234" class="more-link">Continue reading <span class="meta-nav">→</span></a></p>

* A critical part of global trade is jeopardized by attacks on vessels in the Red Sea.

* Moody’s has downgraded China’s credit rating to negative due to growing debt concerns.

* China’s Services PMI climbed to a three-month high in November.

* The Eurozone Composite PMI has contracted for the sixth consecutive month in November.

* Uber shares increased following the announcement that the company will join the S&P 500.

* The fight against inflation presents a significant challenge for renewable energy.

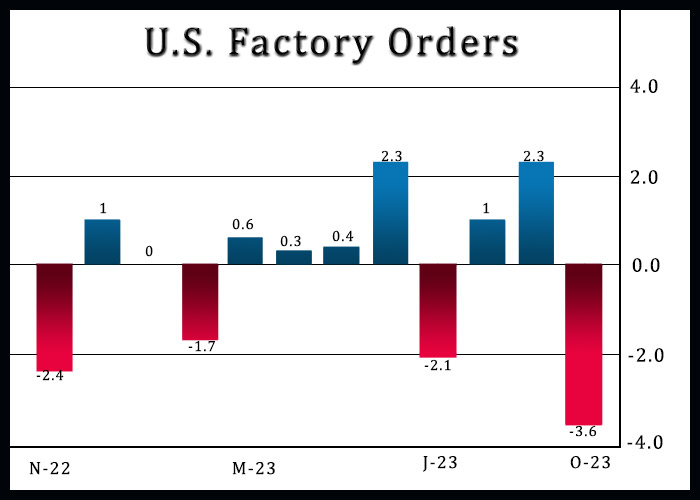

* US factory orders fell significantly in October:

The expected return for the Global Market Index (GMI) remained stable in November. The latest revised long-term forecast for this benchmark—a market-value-weighted portfolio encompassing all the major asset classes (except cash) through a selection of ETF proxies—continues to project a relatively high 6.9% ex ante annualized total-return performance, consistent with the estimate from last month.