Two weeks ago, I noted that U.S. stocks appeared overvalued, a conclusion reached through various metrics. However, as of yesterday’s close for the S&P 500 Index, equities have dropped significantly from their recent highs. Is this coincidence? Perhaps. A more pertinent question is whether this recent downturn marks the beginning of a prolonged decline or merely a typical market correction. Unfortunately, no one can say for sure—history tells us there are seldom clear answers. Still, we can examine the fundamentals to better assess the risks ahead.

* Is the potential reversal of Biden’s economic policies an investment risk?

* China lowers interest rates for the second time this week

* John Deere announces layoffs due to downturn in agriculture

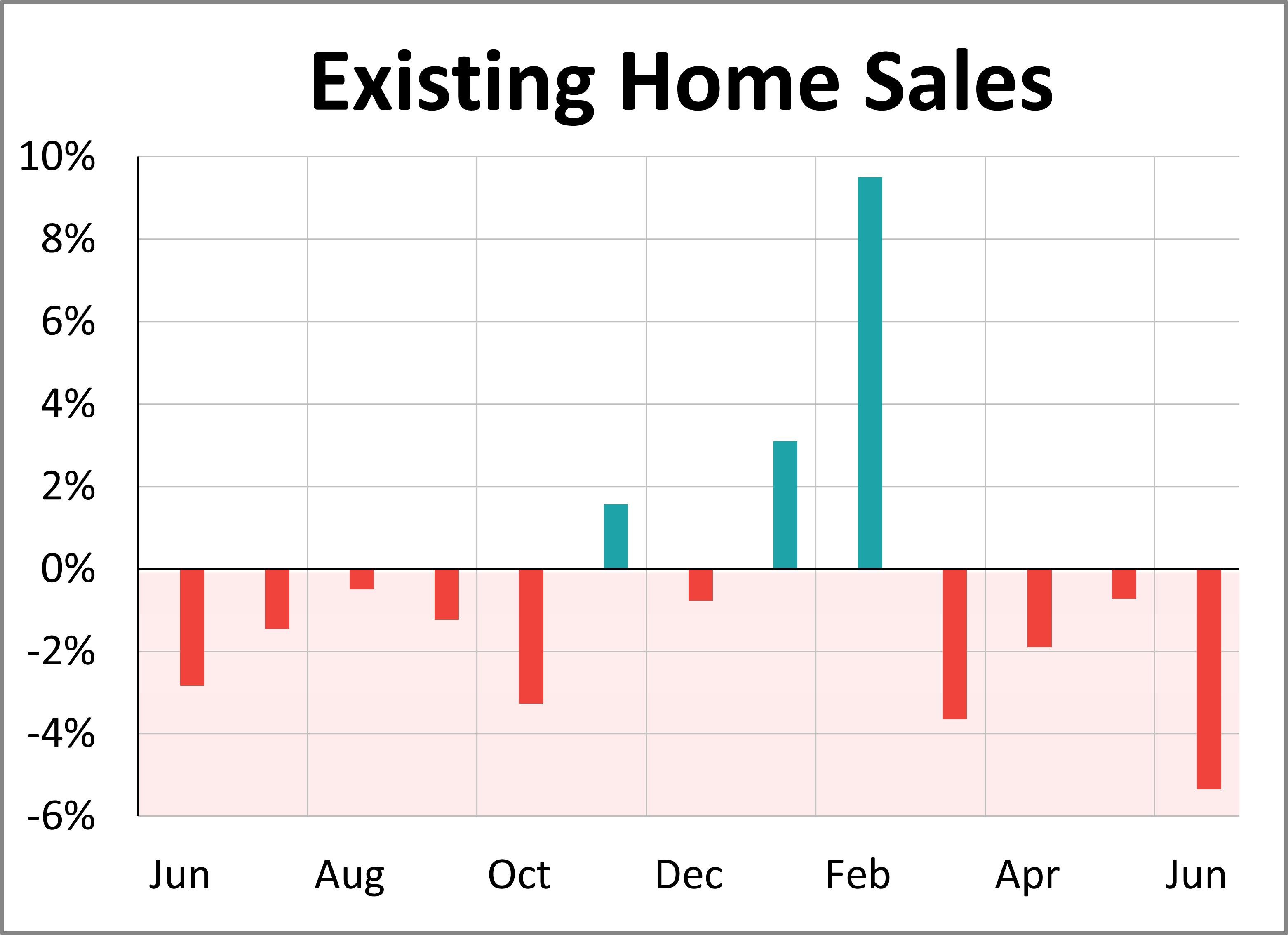

* New U.S. home sales plummeted to a seven-month low in June

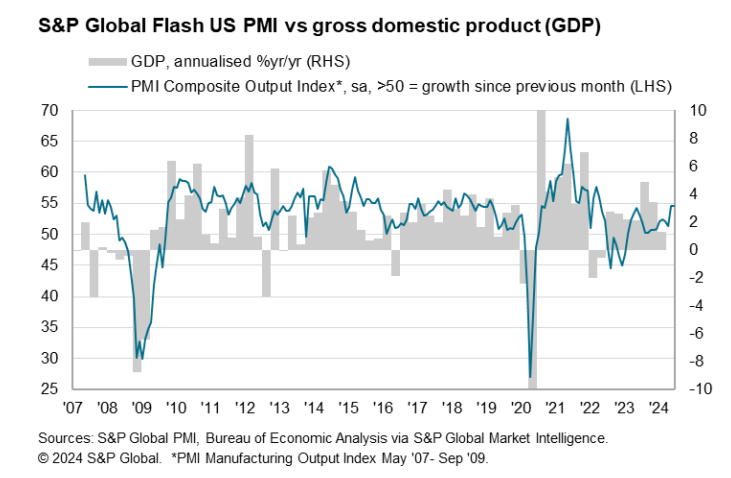

* Growth in U.S. business activity accelerates in July, driven by services:

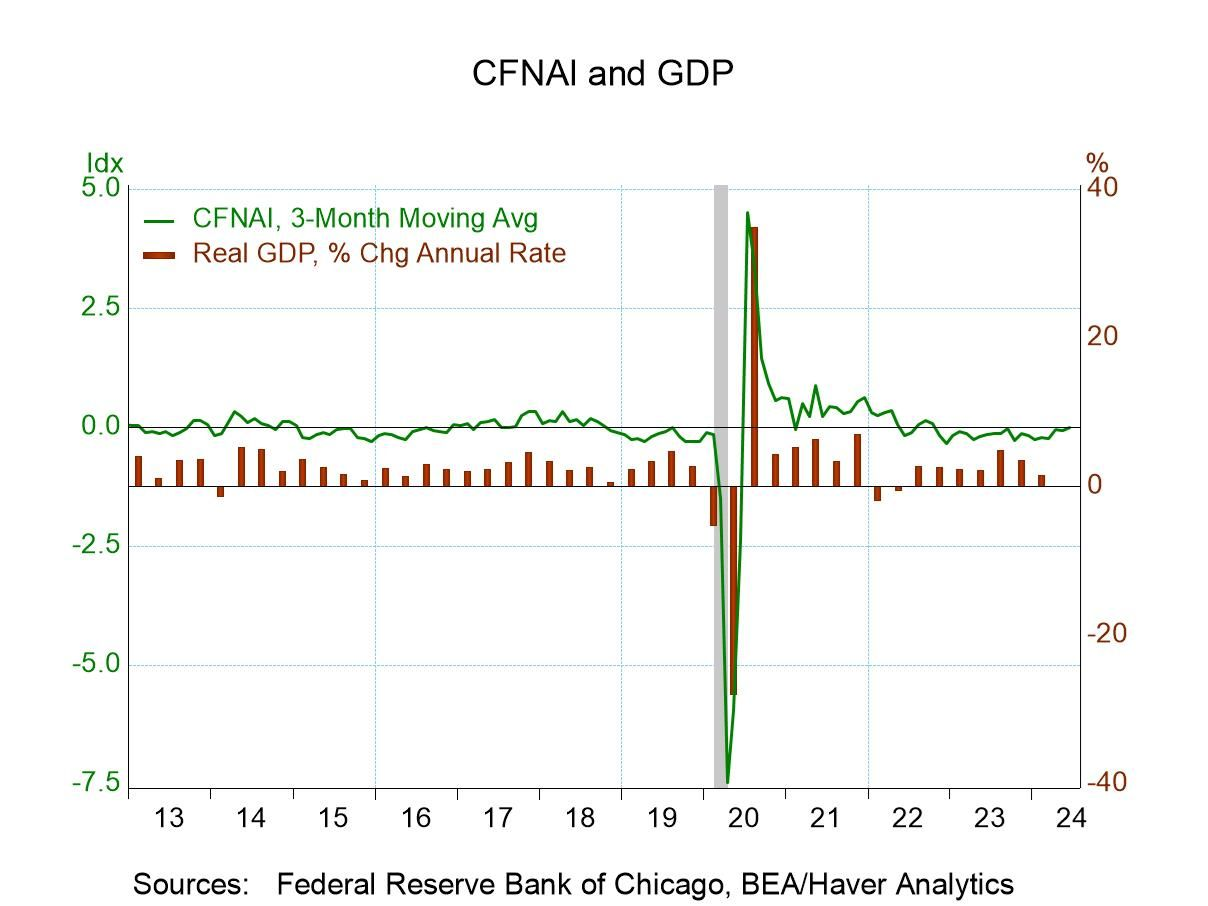

It’s a common human tendency to seek simple explanations regarding the business cycle. The belief that reliability and timeliness can be derived from a single indicator remains persistent; however, recent patterns reveal the flaws in this thinking, as highlighted by a commentary from Axios.

* Several widely-watched recession indicators “are no longer effective”

* Trading volume exceeds $1 billion on the first day of ether ETFs

* The FTC initiates an investigation into rapidly changing ‘surveillance pricing’

* Eurozone business activity nearly comes to a standstill in July, according to PMI data

* U.S. existing home sales decline for the fourth consecutive month in June:

The U.S. is projected to report modest growth in the second quarter GDP figures, which will be released on Thursday, July 25. This forecast is based on the median estimate from various projections compiled by CapitalSpectator.com.

* Kamala Harris gathers sufficient delegates to become the Democratic Party nominee

* U.S. regulators identify weak risk management practices at more than half of major banks

* Cybersecurity startup Wiz rejects Google’s $23 billion buyout offer

* Ethereum ETFs approved by the SEC are set to begin trading

* Signs of stabilization in U.S. economic growth observed in June:

A review of major U.S. equity factors year-to-date indicates that large-cap growth remains in the lead, according to ETF prices through July 19. However, analysts suggest that last week may have marked a pivotal moment for the lagging factors.

* The U.S. presidential race tightens as VP Harris appears poised to take Biden’s place

* Stock market laggards have revived in recent days amid tech’s struggles

* The People’s Bank of China unexpectedly reduces the short-term policy rate

* A tight oil market is expected to ease in 2025, as predicted by Morgan Stanley

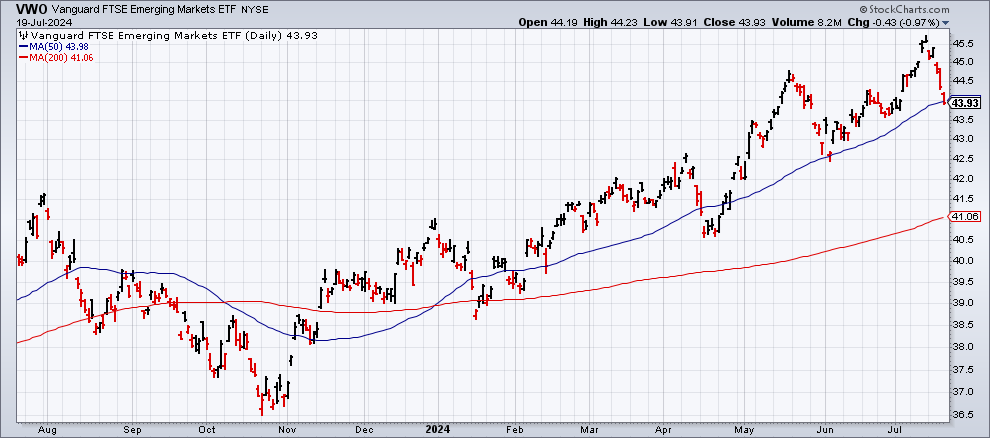

* Sovereign wealth funds are becoming optimistic about emerging markets, as highlighted by a recent survey:

● Tax Alpha Solutions: Effective Tax Management Strategies for High-Net-Worth Investors

● Tax Alpha Solutions: Effective Tax Management Strategies for High-Net-Worth Investors

Matthew Chancey

Essay by author via WealthManagement.com

The Internal Revenue Service recently announced its intention to significantly ramp up audits on high-net-worth taxpayers, large corporations, and intricate partnerships for the tax year 2026.

Audit rates are set to increase by more than 50% for those reporting over $10 million in total positive income (rising from an 11% coverage rate in 2019 to 16.5% in 2026). This announcement is likely to cause concern among affluent individuals.

However, it’s important to remember that an IRS audit primarily seeks documentation and is not an inherently accusatory process; it aims to verify how taxpayers arrived at their figures.

The Federal Reserve is widely anticipated to begin cutting interest rates at the upcoming FOMC meeting on September 18. However, discussions are now shifting toward the extent of those cuts. A significant factor will be how much the neutral rate of interest has changed, if at all, over recent years.

Conclusion

Overall, recent market fluctuations and economic indicators suggest a complex environment. As we anticipate future developments, it’s vital to stay informed and proactive in assessing existing risks and opportunities in the markets. With evolving circumstances, flexibility and understanding the broader picture remain key components for investors looking to navigate these turbulent times.