In recent headlines, several noteworthy economic developments have emerged, impacting businesses and financial markets worldwide. Here are some key updates:

- * A massive IT outage has disrupted operations for companies globally.

- * The key U.S. mortgage rate has fallen to its lowest level since March, according to Freddie Mac.

- * The leading economic index in the U.S. dipped slightly in June.

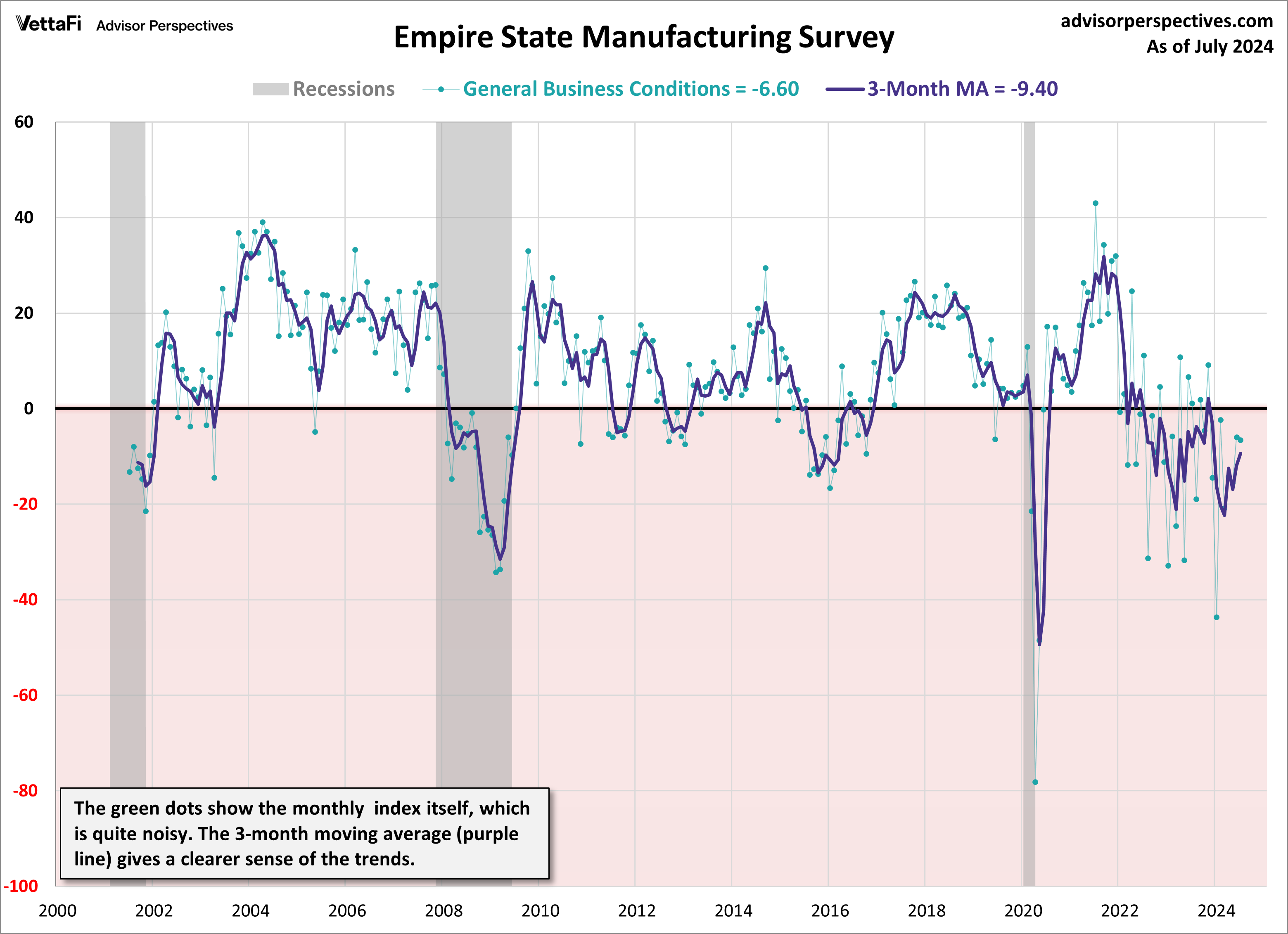

- * Manufacturing activity in the Philadelphia Fed region expanded in July.

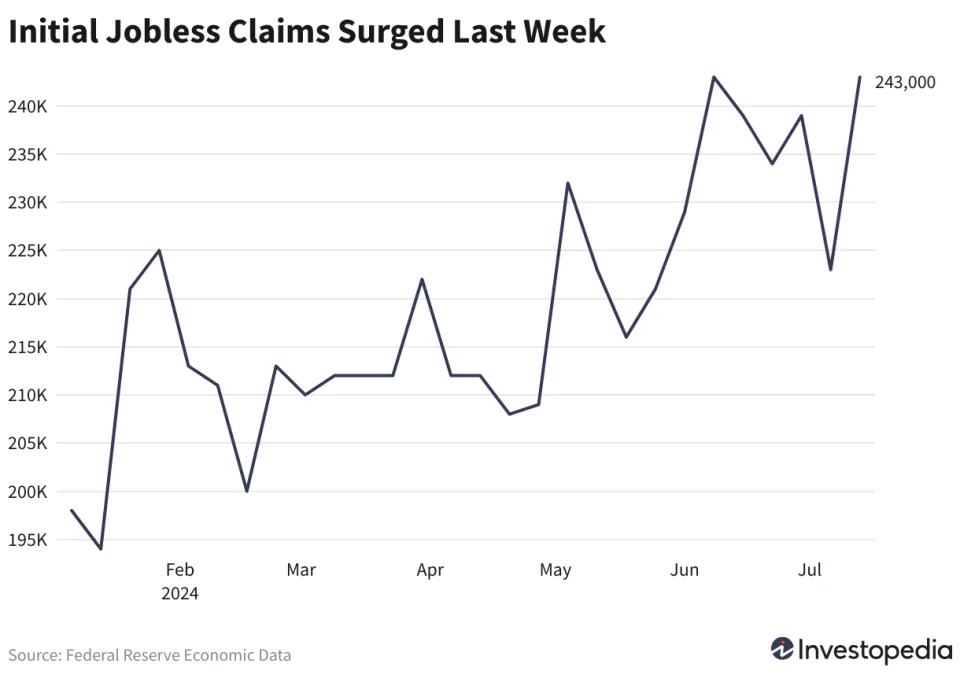

- * U.S. jobless claims increased last week, reaching the highest level recorded so far in 2024.

The Finance AI Challenge: An Evaluation of the Top Six Free Web-based AI Models

David Krause (Marquette University)

June 2024

This article assesses the performance of six free web-based AI models—ChatGPT, Gemini, Copilot, Claude, Perplexity, and Meta AI—specifically concerning finance-related tasks. With a structured methodology, we evaluated the models based on their ability to tackle factual, conceptual, and computational inquiries, as well as their skills in Python coding through a financial case study. Our results indicate that ChatGPT, Copilot, and Perplexity consistently delivered accurate, comprehensive, and well-structured responses. However, challenges like maintaining context, ensuring factual accuracy, and mitigating biases remain significant. This study highlights the necessity for future research to improve domain adaptation, explainability, and ethical considerations to promote the responsible use of AI in finance.

* Fed Governor Waller states that the central bank is ‘getting closer’ to an interest rate cut.

* The U.S. Q2 GDP nowcast has been revised up to +2.7%, compared to 1.4% in Q1, via the GDPNow model.

* The Federal Reserve’s Beige Book indicates that the economy is slowing.

* U.S. industrial production rose more than anticipated in June.

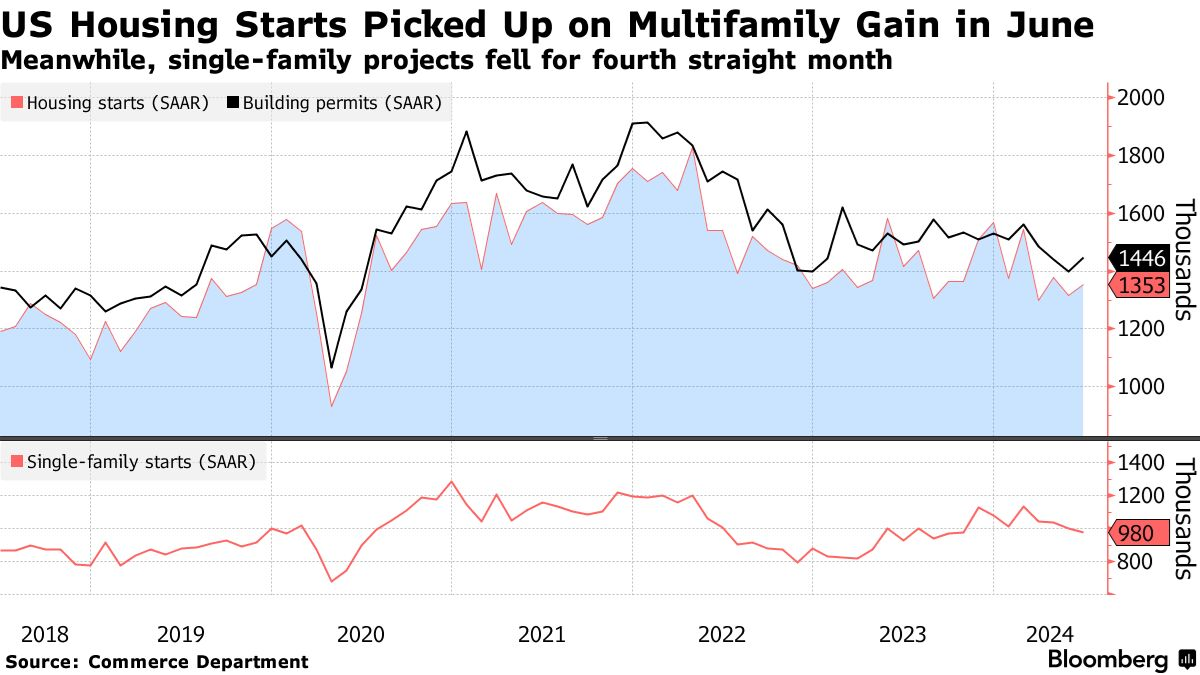

* U.S. housing starts increased in June but remain close to a two-year low.

The second-quarter GDP report indicates that U.S. economic activity is expected to remain sluggish. The current forecast suggests that growth will mirror the modest increase observed in the first quarter, according to the latest nowcast compiled by CapitalSpectator.com.

* The IMF has downgraded its growth forecast for the U.S. in 2024.

* A new phase for the U.S. dollar may emerge under a Trump-Vance administration.

* Trump has stated he would allow Fed Chair Powell to complete his term if elected.

* U.S. builder sentiment declined in July, reaching the lowest level since December.

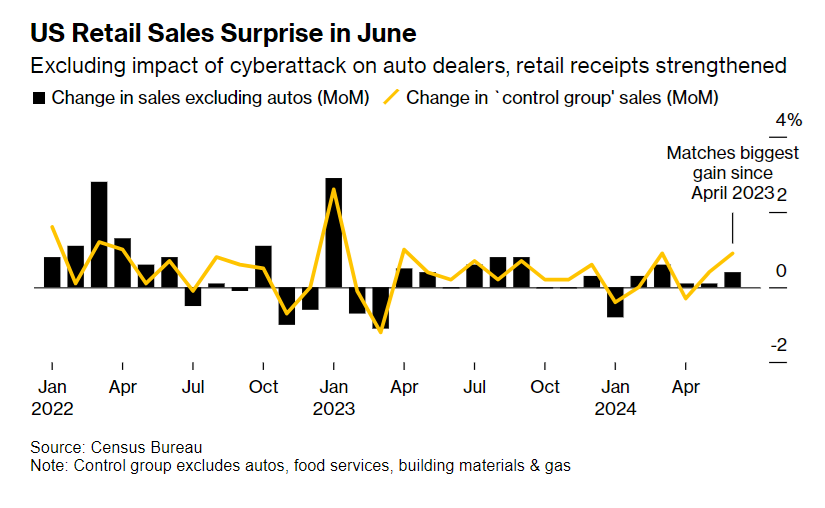

* Retail spending in the U.S. was flat in June, but…

* Excluding autos, retail sales rose by 0.4%, marking the largest increase since April.

If the S&P 500 maintains its current level until December 31, 2024, it will still be recorded as delivering a robust year, demonstrating an 18.1% rise as of July 15. However, some Wall Street firms anticipate even better performance ahead.

* Recent inflation statistics ‘add some confidence’ for potential rate cuts, according to Powell.

* President Biden is expected to advocate for a 5% cap on rent increases.

* Wall Street anticipates the approval of Ethereum ETFs, as further developments unfold.

* Demand for security continues to support government bonds, despite deteriorating government finances.

* The NY Fed manufacturing activity index has continued to decline in July.

This situation is familiar. Markets anticipate high probabilities for interest rate cuts by the Federal Reserve, only to face the opposite outcome later. Is this situation different? That’s the current gamble.

* How might Trumponomics affect the U.S. economy?

* China’s economy slowed in Q2 to its weakest annual growth in five quarters.

* Higher interest rates impacted earnings at major banks.

* Exploring the source of portfolio alpha? Behavioral risk plays a vital role.

* Kuwait has reported the discovery of a large oil field, enhancing reserves by 3.2 billion barrels.

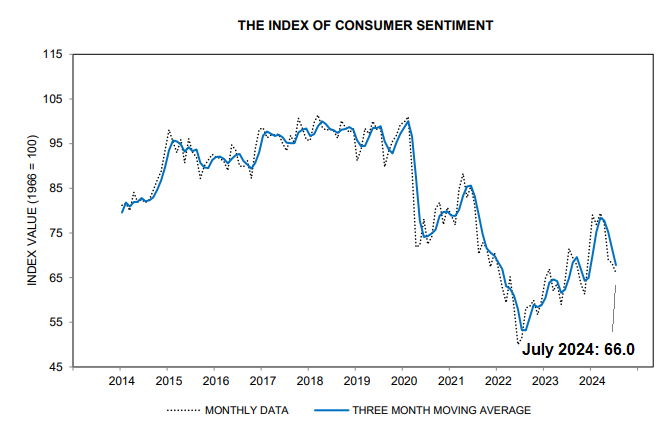

* U.S. consumer sentiment declined for the second consecutive month in July, reaching an eight-month low.

● Shocks, Crises, and False Alarms: Assessing True Macroeconomic Risks

● Shocks, Crises, and False Alarms: Assessing True Macroeconomic Risks

Philipp Carlsson-Szlezak and Paul Swartz

Excerpt via Harvard Business Review

In 2022, predictions of widespread defaults in emerging markets followed rising U.S. interest rates, yet these defaults did not occur. Additionally, a narrative in both 2022 and 2023 characterized an imminent recession as “inevitable.” Nevertheless, the resilient U.S. economy not only refuted these dire forecasts but also achieved significant growth.

For executives and investors, such volatility results in both financial and organizational costs. For instance, automakers who curtailed semiconductor orders in 2020 due to an expected prolonged recession missed out on significant sales during a robust recovery. Leaders who overreact to false alarms risk losing organizational trust through abrupt shifts in strategy, operations, and communication. Thus, making accurate macroeconomic assessments is crucial.

In summary, recent economic updates illustrate a complex landscape for businesses and investors alike. While some indicators show a slowdown, others suggest potential opportunities for growth and recovery. Staying informed on these developments will be crucial for navigating the evolving economic environment.