In 2024, utility stocks have emerged as the top performers among US equity sectors, particularly following the recent market sell-off, as indicated by a series of ETFs up to the close on August 6.

* Consumer spending will be a crucial indicator for assessing the risk of a US recession

* Markets anticipate that the Fed will mitigate recession risks through rate cuts

* The US trade deficit decreased in June, as exports surpassed imports

* US credit card debt continues to grow, reaching a new peak in Q2, as noted in a recent report

* The creator of the Sahm Rule does not advocate for an emergency rate cut

* The US stock market (S&P 500) has begun to recover some losses after a three-day sell-off:

According to current data, the US economic expansion appears to be ongoing. While there are valid concerns that this trend may reverse, such speculation remains unproven. The prevailing statistics clearly indicate that growth is still leading. Though this outlook isn’t assured, it remains the most likely scenario at this moment.

* Biden gathers the national security team amid concerns over a potential Iranian attack on Israel

* The US economy is beginning to show “pre-recessionary” signs, according to Krugman

* While speculation arises about an emergency rate cut from the Fed, analysts disagree on its likelihood, citing historical patterns

* The ISM Services Index rebounded in July, indicating a strengthening US sector

* Global economic growth moderated for the second month in July, as revealed by PMI survey data

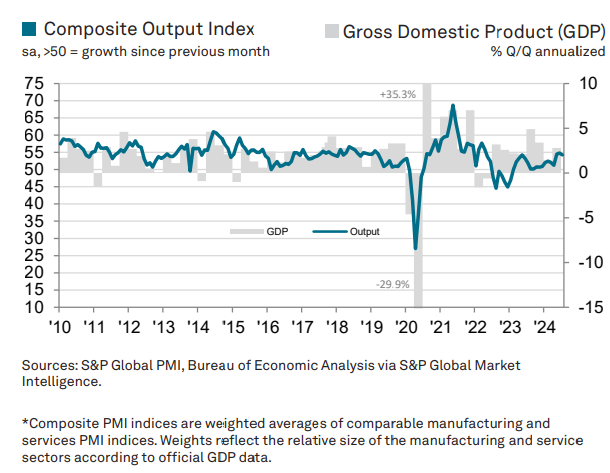

* US output grew “solidly” in July, as indicated by the Composite PMI Index, a proxy for GDP:

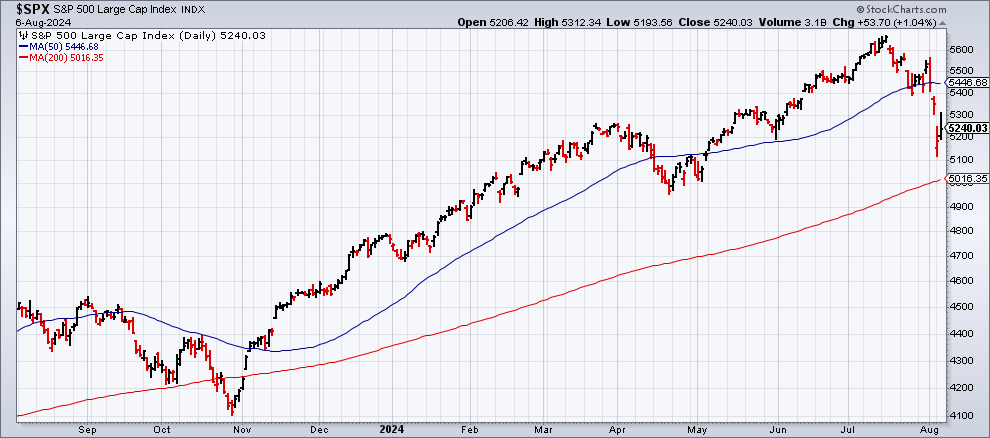

The recent market turmoil that affected global equities last week seems poised to extend into Monday. Triggered by disappointing news from the US job market, this shift in sentiment dampened enthusiasm for American stocks. Despite last week’s downturn, US equities are still outpacing other major asset classes substantially. However, this elevated performance suggests that they may currently be at risk of a period of “normalizing” performance levels.

* A sudden increase in unemployment raises concerns about a potential recession?

* An economist argues that the Fed has delayed necessary interest rate cuts

* China’s services sector expanded in July

* The Eurozone economy reportedly “stalled” in July, as per PMI survey data

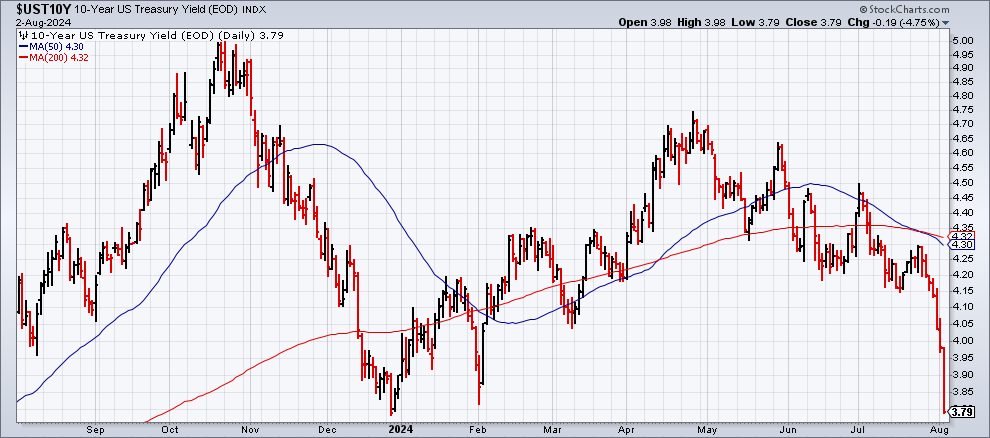

* The US 10-year yield experienced a sharp decline last week, closing at 3.79%—the lowest since December:

● Demography and the Making of the Modern World: Public Policies and Demographic Forces

● Demography and the Making of the Modern World: Public Policies and Demographic Forces

John Rennie Short

Summary via publisher (Agenda Publishing via Columbia U. Press)

John Rennie Short critically analyzes the impact of demographic changes from social and economic viewpoints, exploring their implications for public policy. He highlights how seemingly unrelated events, from the Arab Spring to migration from Africa to Europe and budgetary negotiations in the US, are influenced by demographic forces. Through the demographic transition model, the book examines the key demographic factors behind major social and economic issues and the public policies developed to address these challenges.

The total return outlook for the Global Market Index (GMI) has slightly decreased in July, marking its first downward adjustment in several months. The GMI’s long-term forecast now suggests an annualized performance of 7.0%, a minor drop from the previous projection, based on the average of three models (details below). The GMI serves as an unmanaged benchmark that encompasses all major asset classes (excluding cash) according to market weights, utilizing a variety of ETF proxies.

* US jobless claims rose to a yearly high

* Wage growth in the US for Q2 slowed, reaching its lowest rate in over three years

* Sales of light vehicles in the US saw a modest recovery in July

* US construction spending declined for a second consecutive month in June

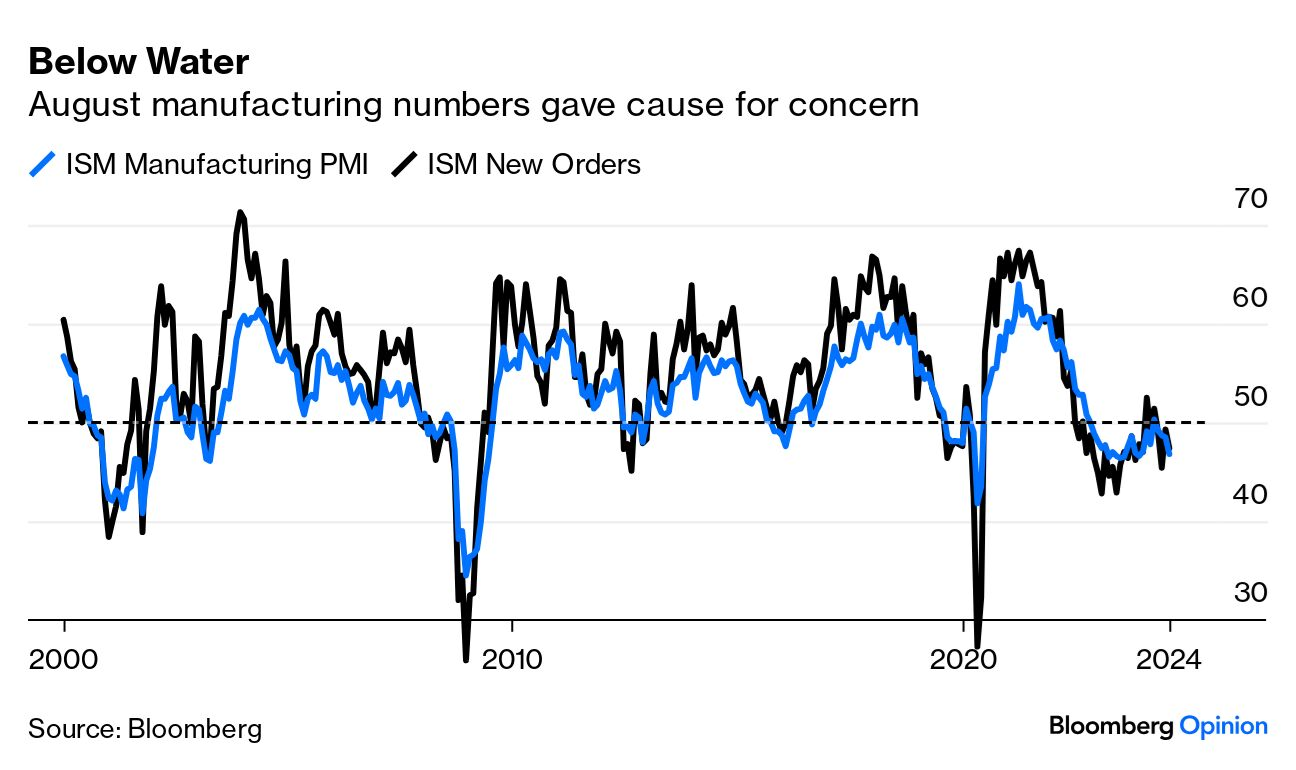

* The ISM Manufacturing Index dropped in July, indicating continuous contraction in the sector:

US real estate investment trusts led a significant rally across major asset classes in July, with commodities being the only exception, having experienced a decline last month. Overall, global markets displayed a robust increase, marking a positive start to the third quarter according to various ETF proxies.

This article provides insights into the current economic landscape, focusing on recent market movements and performance indicators. The discussions highlight trends in consumer behavior, Fed policies, and key economic metrics that shape the US economy.

In conclusion, while there are signals of potential economic shifts, the prevailing data indicates that growth continues to dominate the climate. How these trends unfold in the following months will be critical in determining the economic direction.