This week, investors are closely monitoring the interactions between the Federal Reserve and the bond market in light of Donald Trump’s recent request for lower interest rates. While the central bank is unlikely to make decisions based solely on presidential directives, Trump’s updated policy agenda will undoubtedly influence economic dynamics in some capacity.

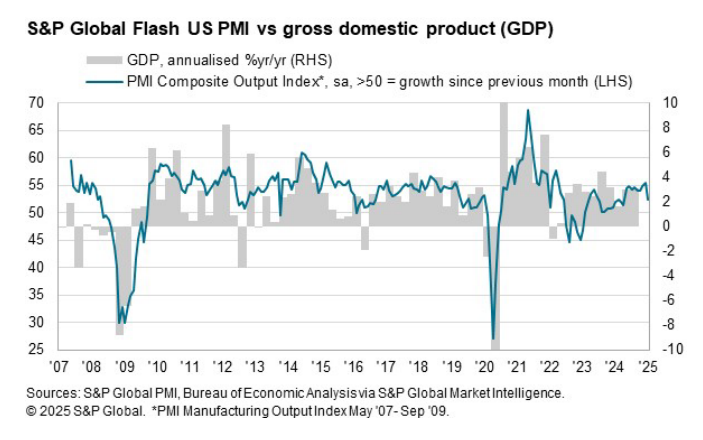

The US Composite Output Index, a survey-based GDP proxy, showed a slowdown in growth for January, according to S&P Global reports. The expansion of business activity declined from December’s 32-month peak to a more moderate pace. Chris Williamson, chief business economist at S&P Global Market Intelligence, noted, “While growth has decelerated slightly, ongoing confidence suggests this trend may be temporary. The increase in hiring driven by an improved business outlook is especially promising, with job creation at rates unseen in two-and-a-half years.”

● Gambling Man: The Secret Story of the World’s Greatest Disruptor, Masayoshi Son

● Gambling Man: The Secret Story of the World’s Greatest Disruptor, Masayoshi Son

Lionel Barber

Essay by author via Harvard Business Review

Masayoshi Son, the billionaire founder and CEO of SoftBank, is one of the most enigmatic figures in the business world. Both Japanese and Western media often portray him as a dreamer, financial innovator, and speculator—sometimes viewed with skepticism due to his history of taking significant risks. His life journey reads like a chronicle of pivotal events in modern business, spanning the rise of personal computing, the internet, the dot-com bubble, the emergence of China, the global financial crisis, and the dawn of artificial intelligence. As Simon Nixon aptly noted in his review of “Gambling Man,” “He appears to have interacted with everyone and attempted to acquire everything.”

During his first week as president, Donald Trump enacted a series of executive orders. Among them, his most ambitious declaration was the intention to direct the Federal Reserve to lower interest rates.

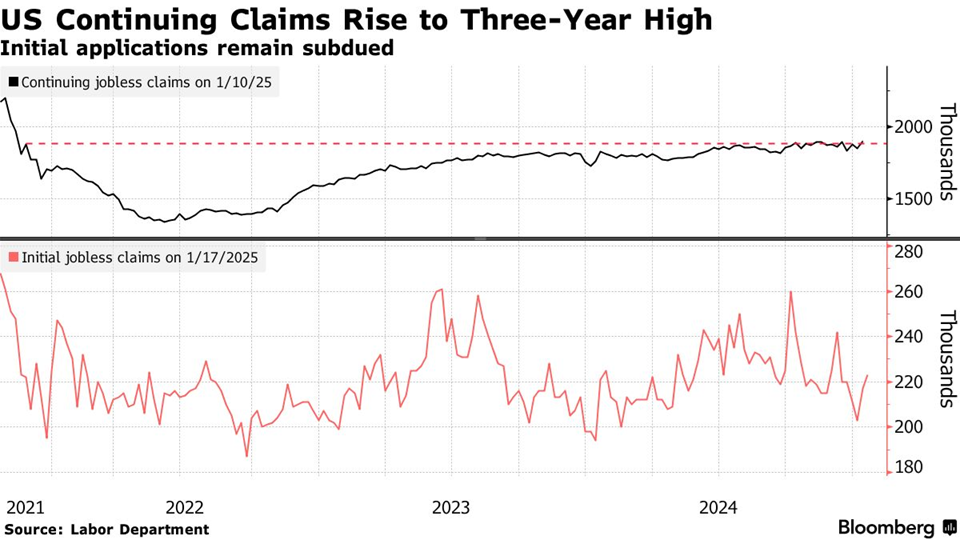

US jobless claims increased slightly last week, remaining low overall, indicating a robust hiring environment for the foreseeable future. However, continuing claims rose to their highest level in over three years, suggesting that a growing number of workers are finding it difficult to secure new employment.

Are we experiencing a calm before a storm in the bond market? Recent weeks have seen a temporary pause in the sharp rise of Treasury yields that has characterized earlier trading. This cautious tranquility may very well be a prelude to forthcoming news and data that will provide clarity on this uncertain period.

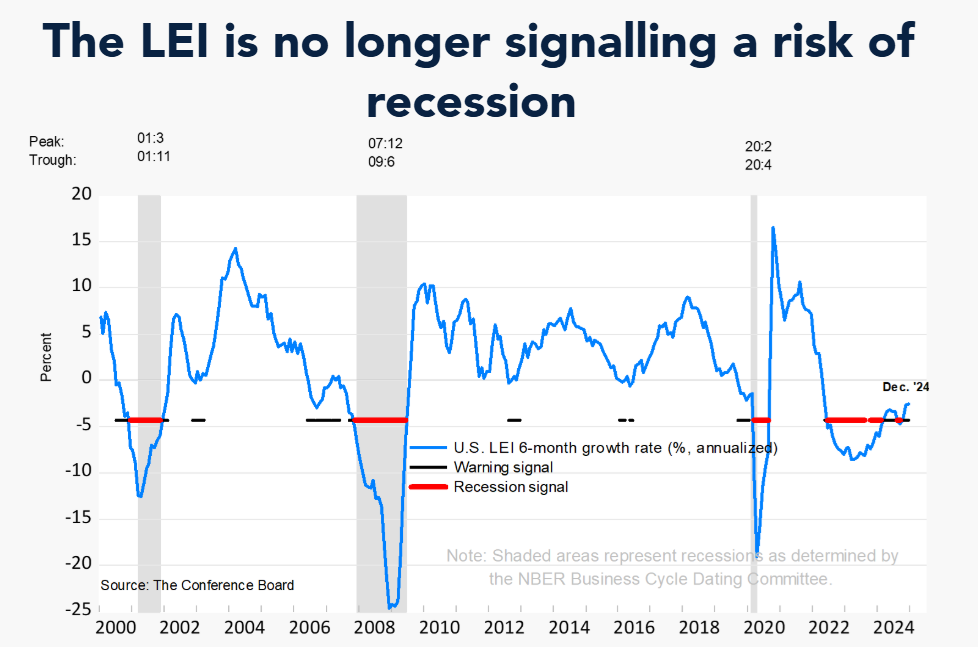

The US Leading Economic Index showed a slight decline in December, though the growth rates for the next 6 and 12 months appear less negative, suggesting fewer challenges for the US economy ahead, as reported by the Conference Board. Despite this decline, robust growth momentum is anticipated to begin the year, with a projection of a 2.3% increase in US real GDP for 2025.

Could this be the era of commodities? Recent trading activity in early 2025 paints a compelling picture for various ETFs that track major asset classes, with preliminary results indicating that commodities are gaining a significant advantage early in the year.

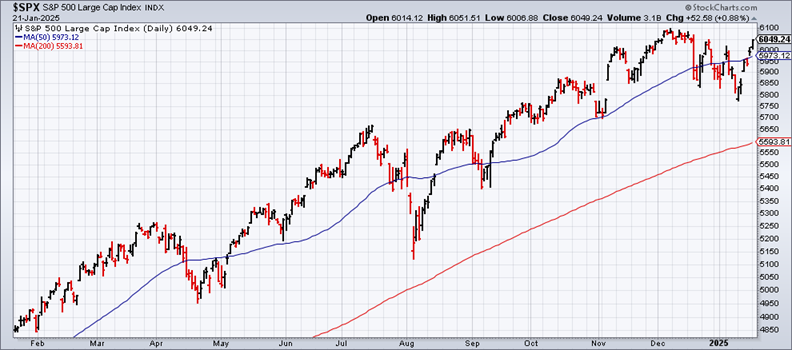

US equities saw an uptick for a second consecutive day, bringing the S&P 500 Index closer to its record high achieved in December. “The tariff-related announcements from President Trump’s Inauguration Day were less severe than anticipated,” stated Alec Phillips, chief US political economist at Goldman Sachs, in a note to clients. Jamie Cox, managing partner at Harris Financial Group, commented that the market “appears to have moved past its tariff-induced fears.”

On his first day as president, Donald Trump introduced an array of bold ideas aimed at overhauling economic policies. His proposals are as audacious as they are controversial, with many debating their potential impact on US priorities.