In a remarkable turn of events, Syrian rebel forces succeeded in overthrowing dictator Bashar al-Assad over the weekend, who is said to have fled to Russia. This unexpected shift of power shocked many, but analysts agree that its consequences will resonate throughout the region and potentially beyond.

The overthrow of Syria’s president sets the stage for a precarious future for the nation and raises new concerns for the Middle East and beyond. This regime change has significantly reshaped the geopolitical landscape, affecting key players such as Russia, Israel, Turkey, and the United States among others. “The abrupt fall of the Assad regime signals a substantial and transformative shift in geopolitics,” observes SpecialEurasia, a consultancy. “The swift military advances by the Syrian opposition, led by Hayat Tahrir al-Sham (HTS), have drastically changed the political and military landscape in the region.” Qutaiba Idlbi, a senior fellow at the Atlantic Council, advises: “The fall of the Assad regime offers a chance to tackle enduring challenges in Syria and the broader region. However, if not managed prudently, it could result in additional instability.”

Can you believe a year has flown by? It’s time for our annual recap of notable titles featured in CapitalSpectator.com’s weekly Book Bits column. This time, we revisit ten must-read books from the past year that stood out for various reasons. We’ll cover five today and the rest next week. Happy reading!

● Slow Burn: The Hidden Costs of a Warming World

Robert Jisung Park

Review via International Monetary Fund

As climate change accelerates, anxiety about its impacts is escalating as well. A United Nations survey indicates that two-thirds of the global population perceives climate change as a serious emergency. Alongside fears of catastrophic tipping points, the world is already experiencing slower, gradual effects. In “Slow Burn,” environmental economist R. Jisung Park examines these repercussions, highlighting issues ranging from increasing inequality to declining productivity and economic performance.

Limits to Diversification: Passive Investing and Market Risk

Lily H. Fang (INSEAD), et al.

September 2024

This study reveals that as the prevalence of passive investing grows, so too do the correlations among stocks and overall market volatility, which limits the advantages of diversification. The degree to which a stock is owned by passive funds (such as index mutual funds and ETFs) is a positive predictor of its beta, correlation, and covariance with other stocks, but not its unique volatility. During crises, stocks heavily held by passive funds contribute more to market risk than before the crisis. The phenomenon of correlated trading among passive funds exacerbates these issues, heightened by implicit indexing for performance benchmarking.

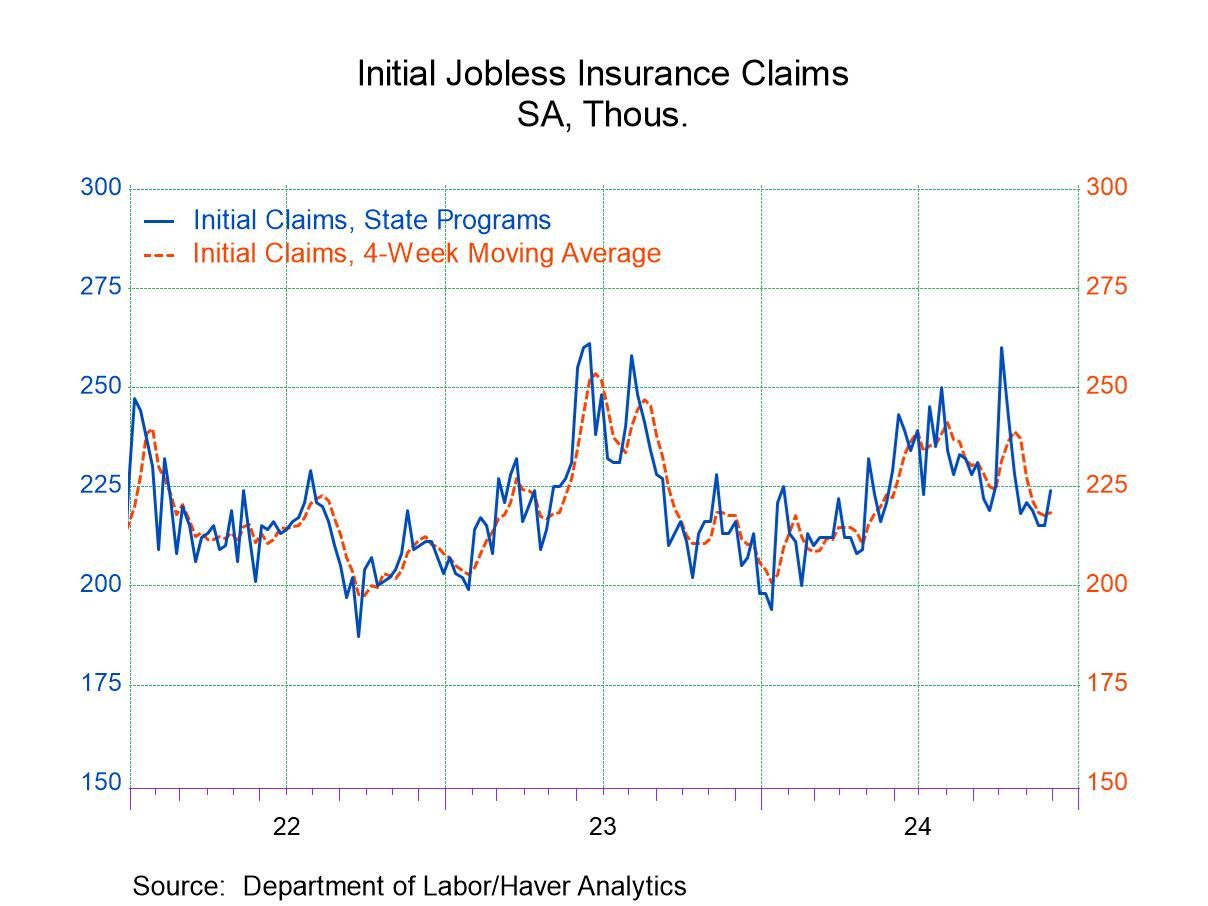

US jobless claims increased to a six-week high last week, yet remain close to historic lows, indicating that the labor market’s outlook remains relatively positive. Unemployment benefit applications rose to 224,000 on a seasonally adjusted basis, the highest number since mid-October.

The winning streak continues. That sums up the performance of several ETFs targeting major US equity factor risk premiums throughout much of this year. As we approach the final stretch of 2024, momentum and large-cap growth factors are achieving considerable success compared to their peers, based on trading data from the close on December 4.

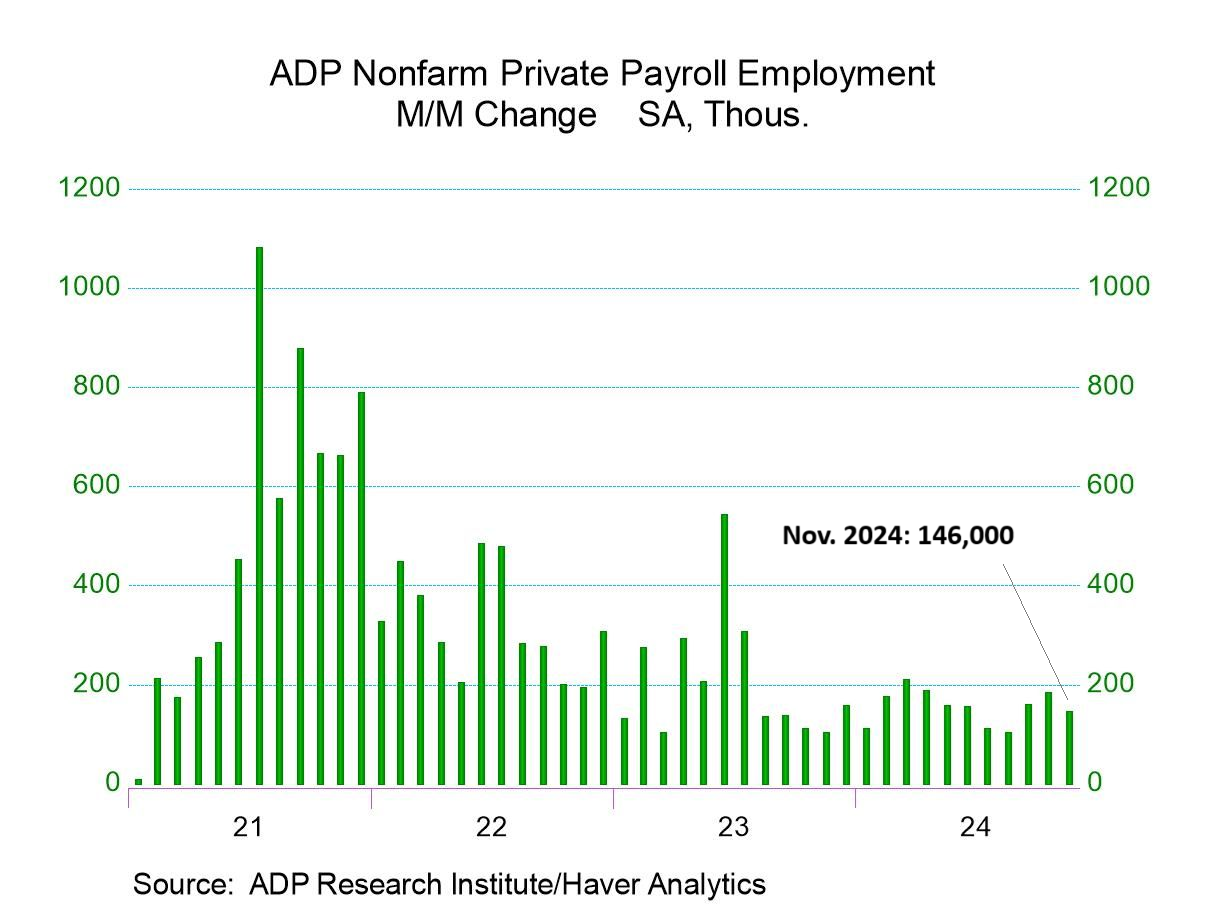

US nonfarm private sector payrolls increased by 146,000 in November, a decrease from a gain of 184,000 in the previous month, according to the ADP Employment Report. “While growth this month was solid, performance varied across industries,” says Nela Richardson, chief economist at ADP. “Manufacturing showed the weakest performance we’ve seen since spring. The financial services and leisure and hospitality sectors also remained soft.”

The prospects for fourth-quarter GDP growth suggest a gradual expansion, but a revised nowcast from the Atlanta Fed indicates a chance for stronger performance.

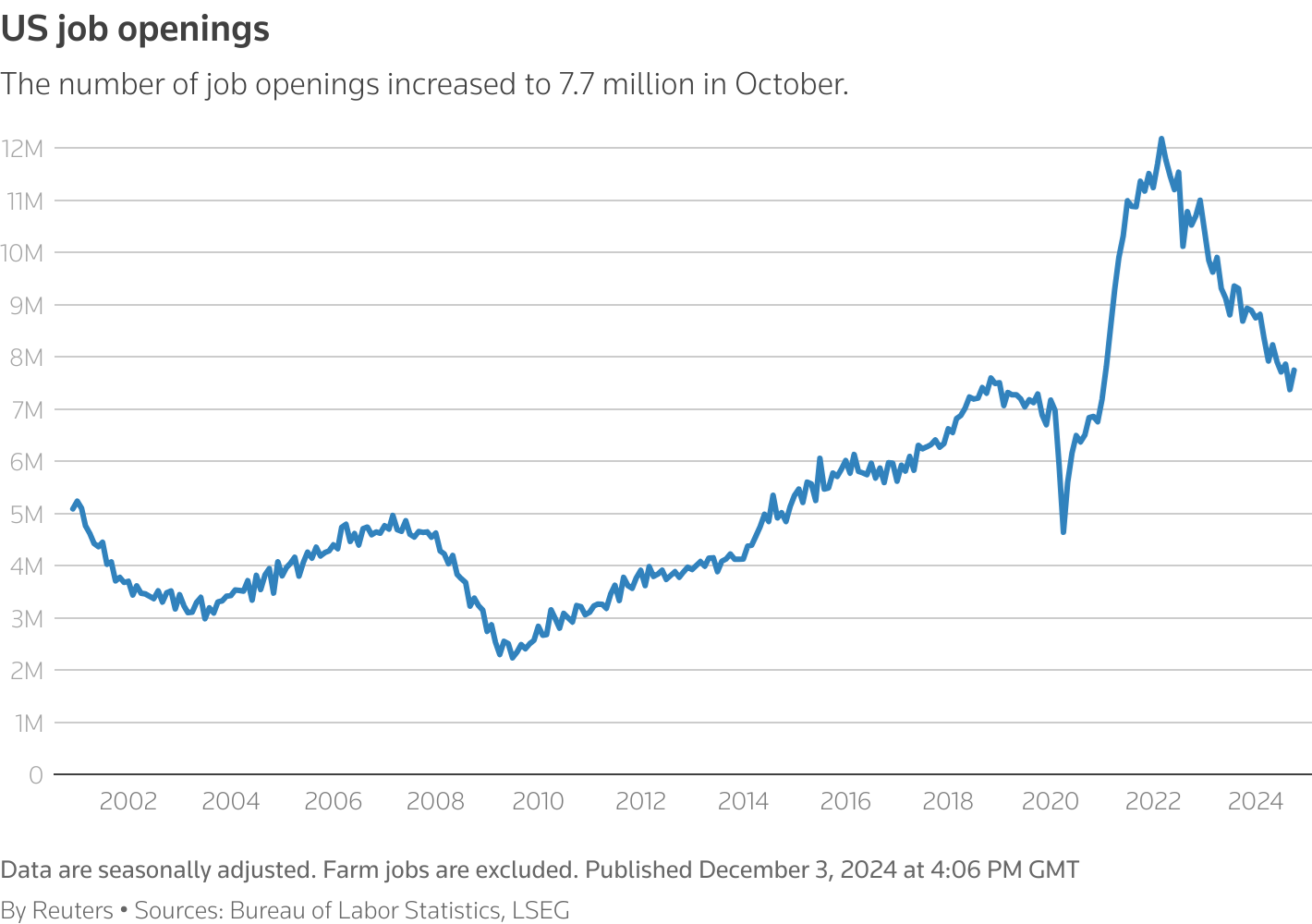

Job openings in the US rose in October, rebounding from a drop in September that had seen new openings hit a three-year low. Although the current level remains significantly below the peak observed in April 2022, it still exceeds the pre-pandemic maximum. “This report suggests continued resilience and does not indicate major concerns regarding the economy,” comments Oren Klachkin, an economist at Nationwide. “Given the current restrictive policies, the Fed might proceed with another rate cut before contemplating a pause next year.”

The long-term performance projections for the Global Market Index (GMI) continued to rise in November, signaling a complete recovery from the recent downturn in ex ante data. This latest estimate also represents the highest return outlook we have seen in recent times, slightly exceeding the forecast from the previous month.