Rethinking the Stock-Bond Correlation

Thierry Roncalli (Amundi Asset Management & University of Evry)

February 2025

The correlation between stocks and bonds is a fundamental concept in finance, closely tied to the principles of asset management. However, grasping this relationship can be challenging. This presentation addresses several key questions: What is the inherent nature of the stock-bond correlation? Why might some investors prefer a positive correlation, while others favor a negative one? How does this correlation interplay with risk premium theory? What is the leverage effect in correlation? Under what circumstances does negative stock-bond correlation occur? Additionally, what are the implications for strategic asset allocation (SAA) and tactical asset allocation (TAA)?

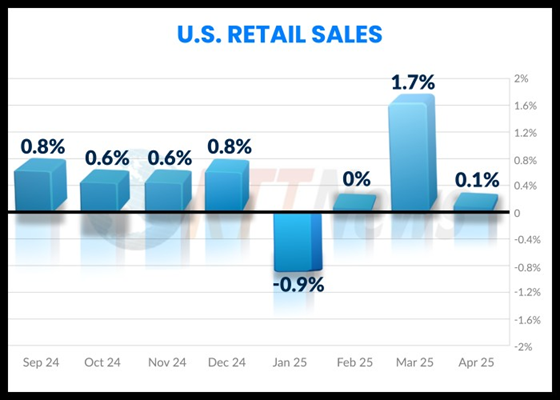

The growth of US retail sales showed only a slight increase in April, with a reported rise of 0.1% following a significant surge in March, which was largely attributed to rushed purchases made in anticipation of tariffs. Core sales, excluding volatile categories and a key component of the gross domestic product (GDP) calculation, experienced a decline of 0.2%. “We are beginning to see the immediate effects of tariffs on consumer spending,” stated Tuan Nguyen, a US economist at RSM US. “While we no longer expect a recession in the next year due to recent tariff reductions, the possibility of several quarters of slow growth has increased.”

In recent years, convincing investors of the benefits of global bond diversification has been challenging, but the scenario seems to be changing as we move through 2025. So far, fixed-income securities outside the US have significantly outperformed the investment-grade US bond benchmark, as evidenced by trends in ETFs up until May 14.

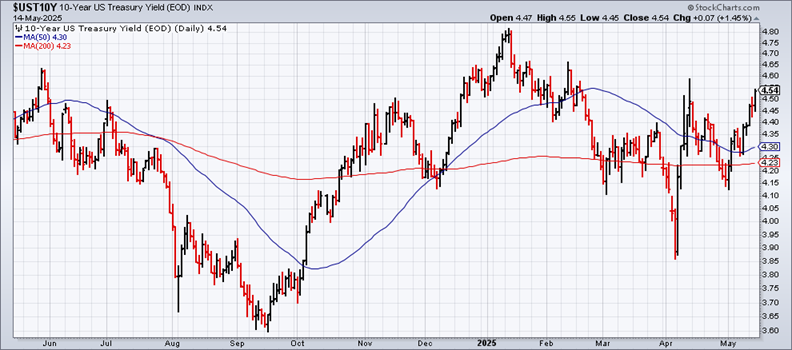

As per projections, the US federal deficit is set to rise by $3.8 trillion by 2034, amounting to roughly 1.1% of GDP, following the approval of a bill in the House Ways and Means Committee that passed on Wednesday. Simultaneously, the yield on the US 10-year Treasury bond climbed to 4.54% on the same day, marking its highest closing value in three months.

The yield on the US 10-year Treasury note remained stable throughout April, maintaining its market premium in relation to various “fair value” estimates. During the past month, the 10-year yield’s monthly average predominantly held steady at around 40 basis points above the average fair value suggested by three distinct models from CapitalSpectator.com.

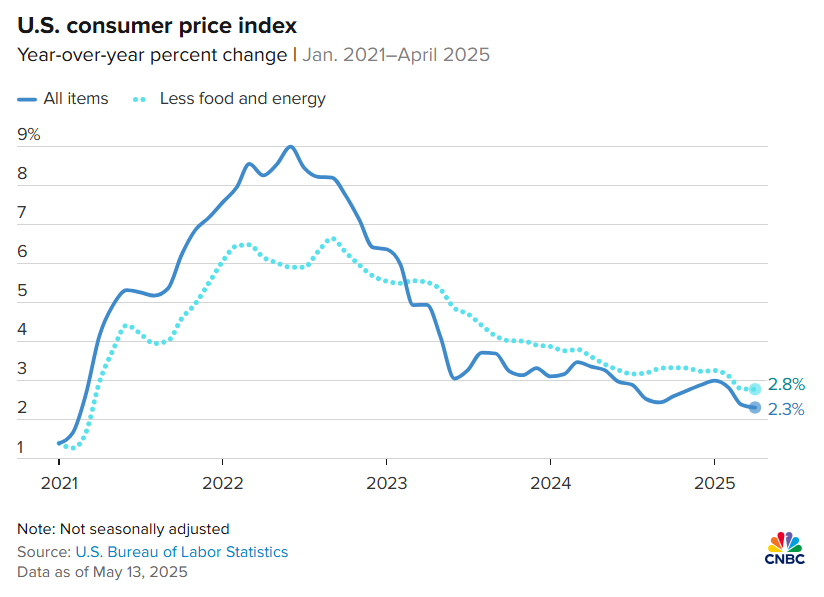

In April, consumer inflation in the US decreased to an annual rate of 2.3%, the lowest level in four years. “This is positive news concerning inflation, especially as we anticipate inflationary pressures from imminent tariffs,” commented Robert Frick, corporate economist at Navy Federal Credit Union. “Although non-tariffed goods are still on their way, some importers may have currently absorbed their tariff costs.”

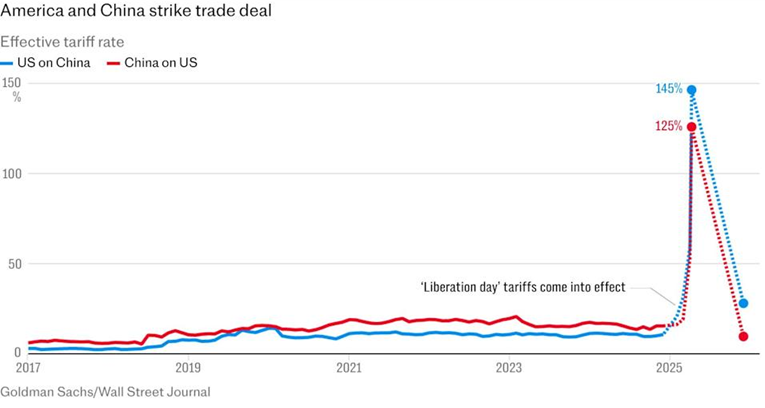

The recent announcement detailing US and China’s commitment to significantly reduce tariffs and continue negotiations triggered a substantial rally in global equities. Market sentiments suggest that advancements in trade talks may lower recession risks both domestically and internationally. However, US stocks are trailing behind other major asset classes so far this year, despite having recouped many of their recent losses.

The recent truce on tariffs between the US and China appears to alleviate recession risks, as evidenced by the notable surge in global equity markets following the announcement. Analysts observe that this 90-day pause can potentially help stave off recession. “Continued de-escalation and progress during this relief period will allow markets to gain some breathing room concerning recessionary pressures,” analysts at Barclays noted prior to the US-China announcement. Mark Williams from Capital Economics commented, “The new status quo isn’t far from our prevailing assumption for tariffs, suggesting that the US economy is likely to avoid recession.”

The Capital Spectator team is currently on the road, leading to a temporary pause in our usual activities. We will resume regular updates on Tuesday, May 13. Wishing everyone safe travels!

The Capital Spectator team is currently on the road, leading to a temporary pause in our usual activities. We will resume regular updates on Tuesday, May 13. Wishing everyone safe travels!

● Our Dollar, Your Problem: An Insider’s View of Seven Turbulent Decades of Global Finance, and the Road Ahead

● Our Dollar, Your Problem: An Insider’s View of Seven Turbulent Decades of Global Finance, and the Road Ahead

Kenneth Rogoff

Essay by the author via The Economist

To paraphrase a well-known adage: it’s not only the unknown that can lead to trouble, but also misconceptions about what we believe to be true. This sentiment perfectly captures the flawed reasoning that has caused significant disruption to the global economy due to the actions of President Donald Trump and trade advisor Peter Navarro. While the dollar will likely retain its status as a dominant global currency for the foreseeable future, it is expected to lose some ground. Anticipate the yuan and euro to increasingly challenge the dollar in mainstream trade, while cryptocurrencies may take a similar role in the informal economy, which constitutes about one fifth of global GDP. A reduced market share could lead to higher interest rates on long-term dollar debt and diminished effectiveness of US financial sanctions, among other consequences.