Predicting economic and market trends has always been a challenge, with various methods available, each bearing its own advantages and disadvantages. A recent innovation in this area is the emergence of prediction markets—platforms where users can bet on the outcomes of future events and observe live probability estimates. While the future remains unpredictable and certainty is elusive, tracking estimated probabilities for significant macroeconomic events can provide an additional layer of analytical insight, especially when compared to estimates from traditional sources. This article marks the beginning of a series that will periodically assess predictions for a range of economic and financial expectations. The data presented here is sourced from Polymarket and Kalshi. Readers should remember the classic caveat: Caveat emptor! The predictions mentioned reflect specific snapshots in time (as of today). For the most current insights, please refer to the provided links.

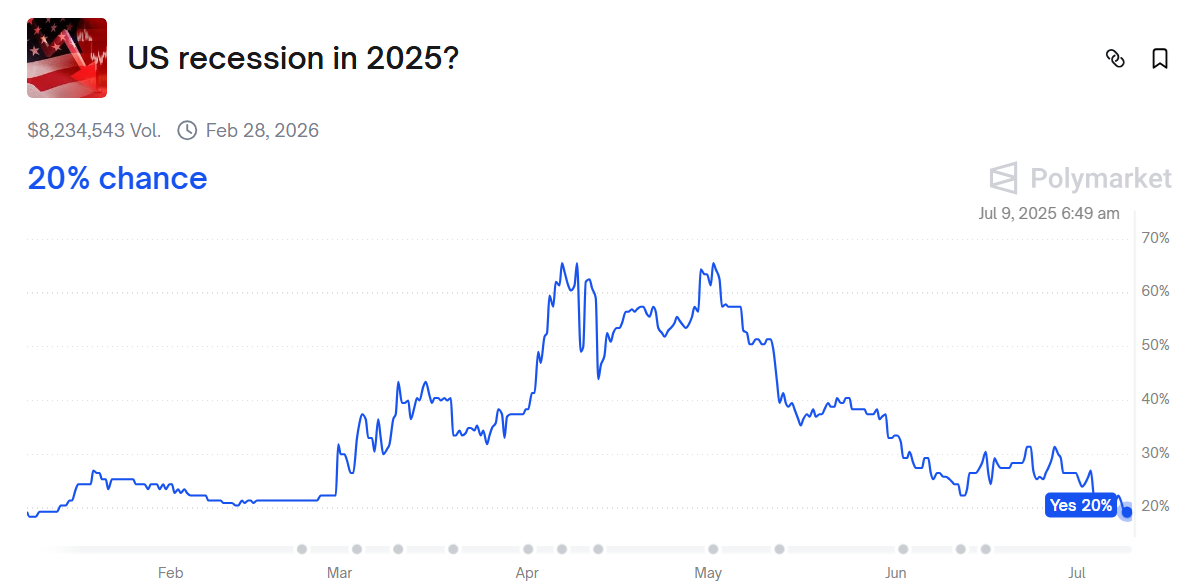

Is a US recession on the horizon for 2025?

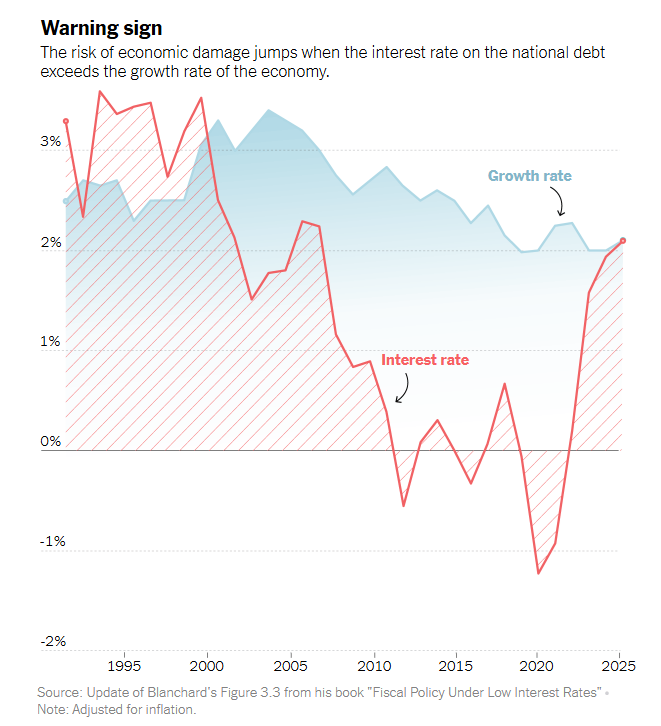

The recent dip in the US economic growth rate, now below the interest payments on the national debt, signals a potential concern, as noted by Jared Bernstein, a former chair of President Biden’s Council of Economic Advisers. “The interest rate we are paying on our national debt has surged,” he commented, attributing this rise partly to government spending during the pandemic and increased inflation. “This rate has escalated to match our growth rate, which could be a pivotal factor for the sustainability of our debt.”

The US economy is anticipated to recover in the second quarter following a slight contraction in the first quarter. However, projections for this rebound have been adjusted downward based on median estimates from a series of nowcasts compiled by CapitalSpectator.com.

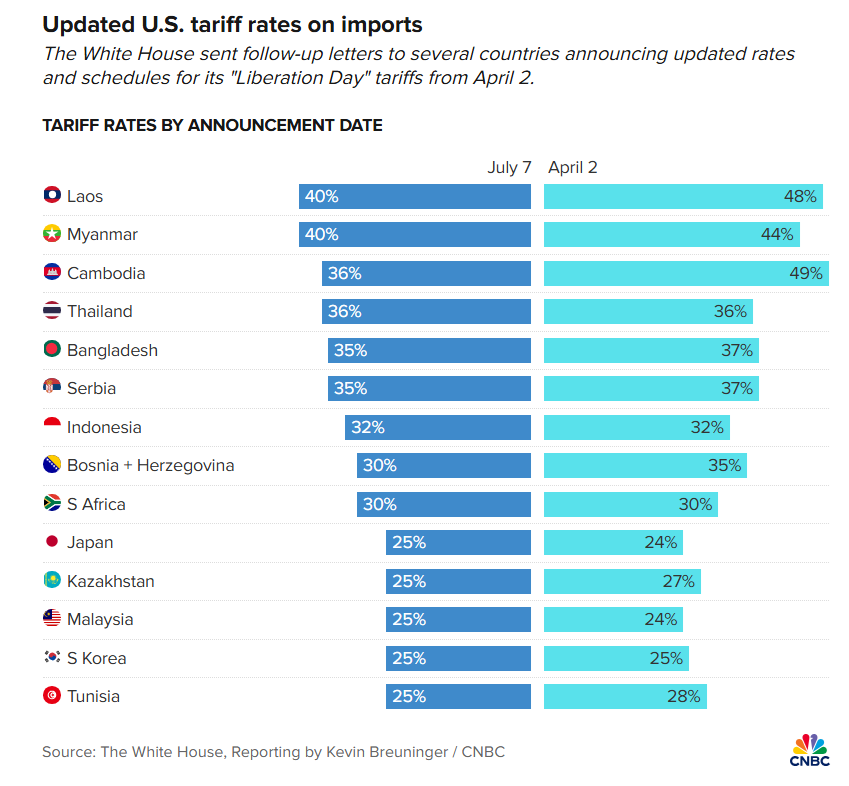

Trump announced new tariffs that will take effect on August 1. These tariffs will target imports from several of America’s major trading partners, notably Japan and South Korea, facing a 25% tariff, as stated in the President’s social media updates on Monday.

This week is expected to reveal early indicators regarding two distinct risk factors that could impact the bond market.

On one side, the fluctuating risk of tariffs poses a potential threat that may generate new economic challenges, which could, in turn, soften growth and lead investors to seek safe havens, potentially prompting the Federal Reserve to adopt a more accommodating policy. Conversely, tariffs could also raise inflation levels, compelling the Fed to maintain higher interest rates for an extended period or even raise rates further. Determining which influence will prevail is complicated due to multiple factors, including ongoing uncertainty about tariff changes and the potential economic implications linked with increased import costs.

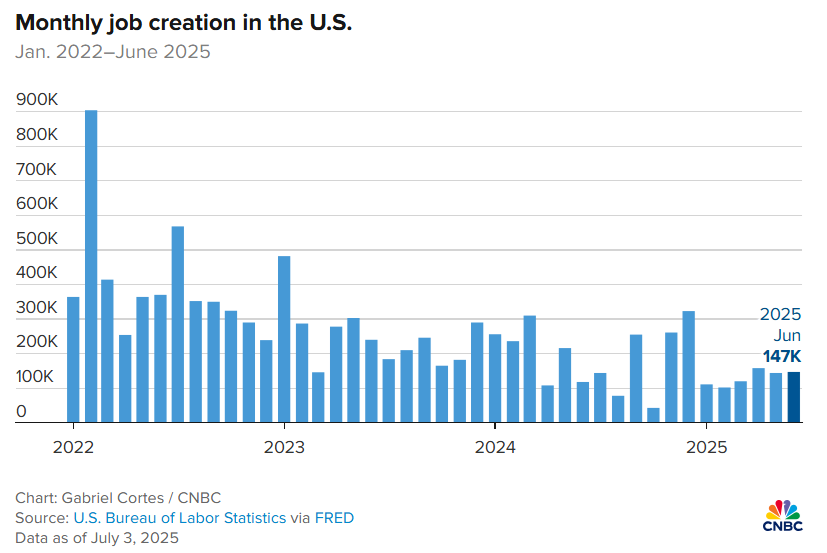

US payrolls outperformed expectations in June, with an increase of 147,000 jobs for the month. “This solid jobs report for June reinforces the resilience of the labor market and effectively rules out the possibility of a rate cut in July,” stated Jeff Schulze, head of economic and market strategy at ClearBridge Investments. For the past year, payrolls have displayed steady growth at approximately 1.15%.

As we move through the week, it is essential to acknowledge a significant truth: a lengthy July 4 holiday weekend should be celebrated as an undeniable right. Consequently, the Capital Spectator will pause operations until the standard schedule resumes on Monday, July 7. Wishing everyone a joyful Independence Day!

As we move through the week, it is essential to acknowledge a significant truth: a lengthy July 4 holiday weekend should be celebrated as an undeniable right. Consequently, the Capital Spectator will pause operations until the standard schedule resumes on Monday, July 7. Wishing everyone a joyful Independence Day!

The long-term expected total return for the Global Market Index (GMI) has experienced a slight uptick for the third consecutive month in June, rising to an annualized 7.3% from a previous estimate of 7.2% in the previous month. Despite this increase, the forecast remains moderately lower than GMI’s actual 10-year performance. This projection is derived from the average of three models (described below) for GMI, an unmanaged global benchmark that reflects a market-capitalization-weighted mix of the major asset classes (excluding cash).

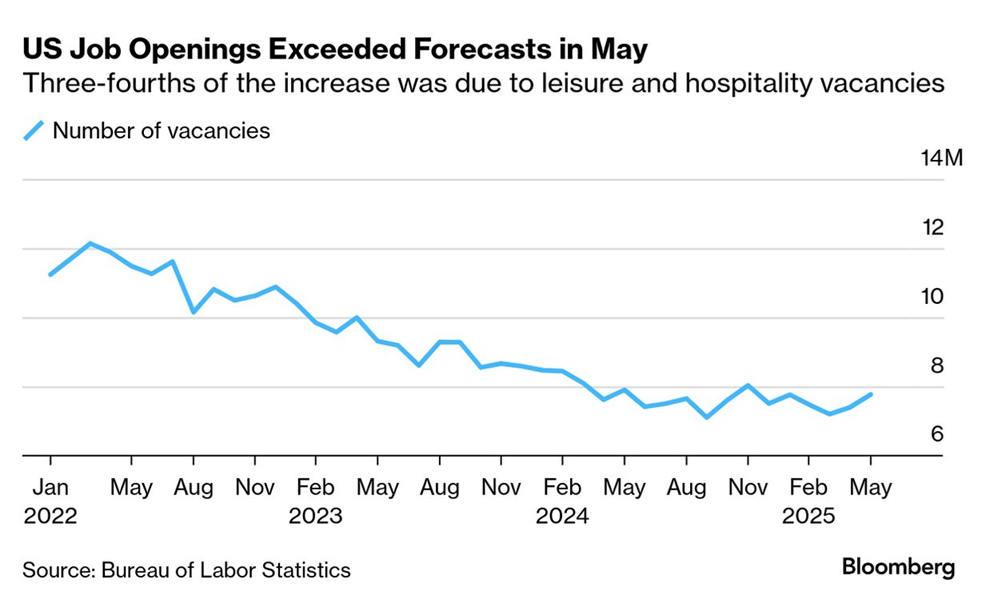

In May, US job openings climbed to the highest level since November 2024. This increase caught economists off guard, as they had anticipated a decline in openings. Despite this recent spike, “we suspect that the demand for new employees is still diminishing amid signs of consumer spending fatigue,” remarked Sarah House, a senior economist at Wells Fargo.

Emerging market stocks continued their upward trend in June, achieving the highest gains among major asset classes for the month, as indicated by various ETFs. A broad index of US equities also performed well, claiming a strong second position, as all primary global market categories enjoyed a rally throughout the month.