Fiscal Dominance and the Politicization of Money

The current discussions around monetary policy often center on technical aspects such as the desired levels of reserves, the role of fintech companies in the Federal Reserve, the nature of the accounts they hold, and the extent of the Fed’s independence. While these issues warrant attention, they pale in comparison to the primary concern influencing American monetary policy today: the fiscal needs of the federal government.

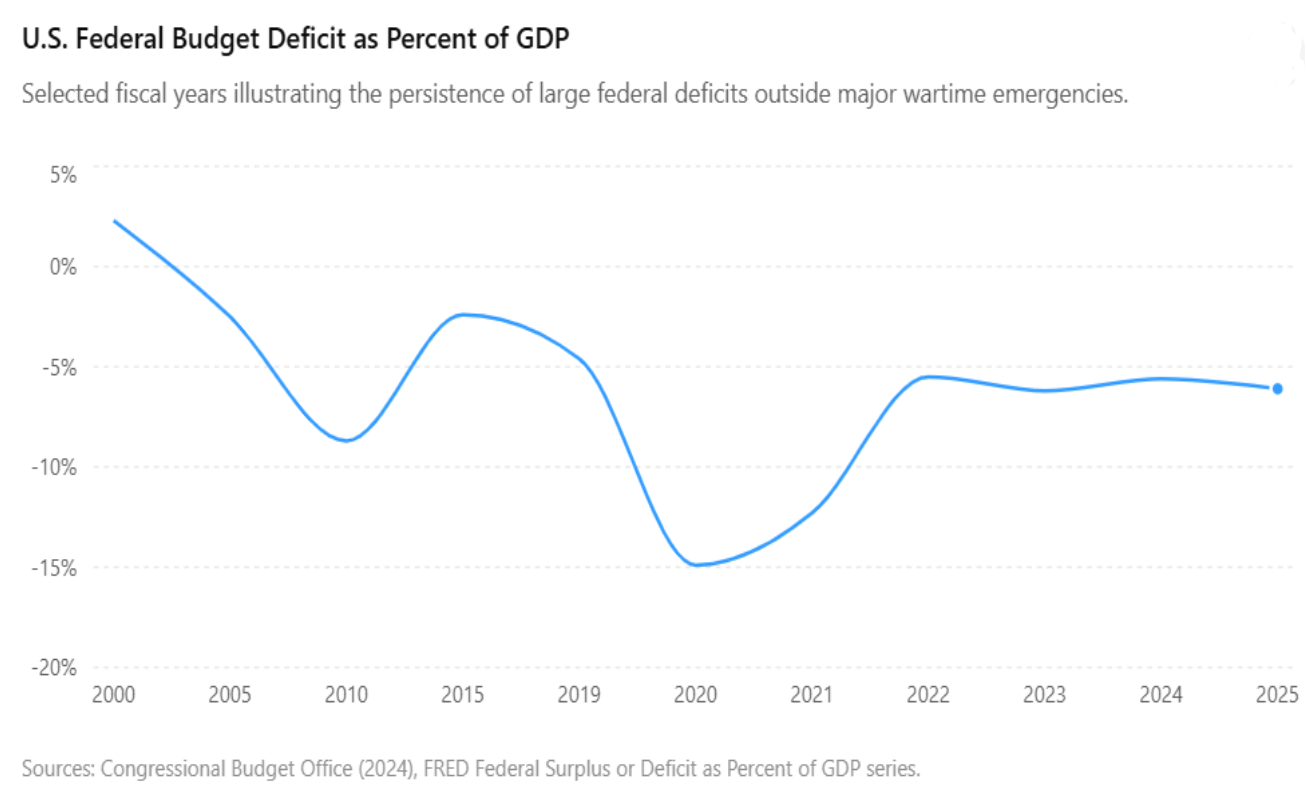

Currently, the U.S. government runs annual deficits that exceed five percent of GDP, a situation that persists even outside periods of war or crises.

To finance these deficits, the government requires a continuous mobilization of substantial financial resources. Under such circumstances, it becomes unrealistic to expect monetary policy to remain insulated from fiscal policy. The increasing politicization and centralization of monetary policy over recent decades is a manifestation of fiscal dominance: monetary policy is increasingly subservient to the state’s borrowing needs.

Historically, central banks were not primarily established to stabilize prices or manage economic fluctuations. Instead, they arose as instruments for public finance. As Vera Smith noted, the government’s intervention in banking was largely driven by the necessity of monetary control for effective state financing. The Federal Reserve, similar to its predecessor, the Bank of England, serves chiefly as a mechanism that allows governments to access credit markets and maintain liquidity for funding public expenditures.

This relationship between fiscal deficits, financial markets, and capital formation becomes clearer when we consider that financial markets are not just abstract entities of liquidity. Instead, they represent claims on tangible wealth. The effectiveness and complexity of these markets rely on accumulated savings being directed toward productive investments. Unfortunately, a growing portion of American savings is not facilitating productive investment but instead financing the government’s current consumption.

When savings are invested in entrepreneurial ventures, infrastructure, technological advancements, or capital goods, society’s productive potential expands. This leads to the creation of new wealth, exceeding what the current production structure can generate. Conversely, when savings are directed to consistent federal deficits, they are consumed rather than invested. Treasury securities may maintain financial liquidity and political favor, but they fundamentally represent claims on future taxation rather than on newly generated productive wealth.

This phenomenon contributes to inflationary pressures as well as long-term stagnation. Financial markets may seem robust and liquid, yet beneath this façade, the foundation of productive capital is deteriorating.

The concept of “false rights,” introduced by Jacques Rueff, is particularly pertinent here. It refers to circumstances where the political system generates claims on wealth without creating any corresponding wealth. Monetary expansion and deficit financing permit governments to access existing resources while masking the detrimental transfer from producers and savers to public consumption.

In this context, hoping for a non-political monetary order is fruitless as long as fiscal irresponsibility prevails. As long as the federal government relies on unprecedented levels of borrowing, monetary institutions will inevitably be compelled to manage public debt. While the Federal Reserve may assert its independence, its operational autonomy becomes increasingly tenuous when public financial stability depends on low interest rates, ample liquidity, and orderly Treasury markets.

I am not questioning the genuine commitment of recently appointed Chairman Warsh to the Fed’s independence or sound monetary policy. My focus is instead on the limitations he, and his predecessor, face in their operations.

It is worth noting that not all governmental monetary powers are inherently illegitimate. As I have previously argued elsewhere, there are both economic and moral reasons for a sovereign political society to retain control over money and finance. National defense requirements entail exceptional circumstances where governments may need prompt resource access beyond typical taxation methods. In true emergencies, a fiscal proviso exists where political communities may temporarily subordinate monetary regulations to survival needs.

However, rules designed for emergencies should not evolve into the standard operational protocols of governance. As Ayn Rand noted, moral principles for ordinary human life should not derive from the conditions faced by survivors after a shipwreck. The same principle applies to monetary institutions. Extraordinary powers justified in wartime should not become enduring aspects of peacetime governance or our constitution once the crisis has elapsed.

Ideally, the United States should restore the constitutional distinction between fiscal and monetary powers established at the nation’s founding. Back then, Congress held the power of the purse and was tasked with public finance, while monetary institutions were expected to facilitate commerce and ensure stable currency, not to perpetually fund structural deficits. Re-establishing this separation would mitigate the politicization of money and enhance both democratic accountability and economic stability.

Nevertheless, such a restoration is contingent on fiscal discipline. Monetary reform without accompanying fiscal responsibility is mere illusion. As long as the federal government continues to consume an ever-growing portion of the nation’s liquid savings to support current consumption, monetary policy will invariably remain subordinate to fiscal necessities.

The journey toward a more balanced monetary order should not begin with technical discussions about reserve systems or Fed governance, but with re-establishing fiscal discipline in the American republic.

—

Leonidas Zelmanovitz is a Senior Fellow at Liberty Fund and a part-time instructor at Hillsdale College.