The residential property market has faced significant challenges this year, but recent gains in homebuilder stocks suggest a potential turnaround. However, a closer examination reveals that many uncertainties still loom regarding critical real estate factors, such as the future of mortgage rates and the overall economic landscape.

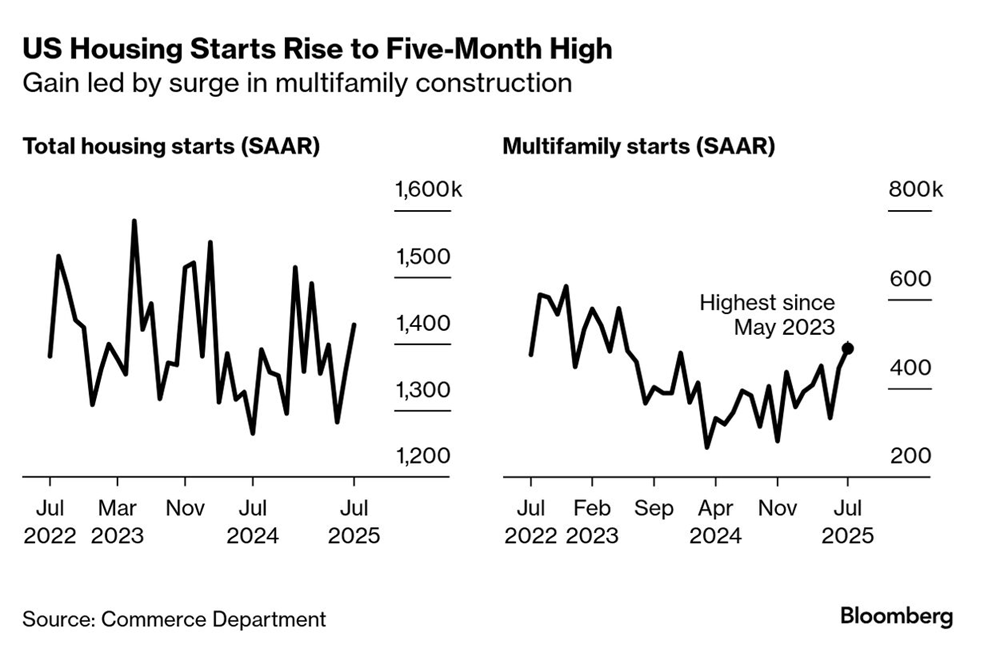

In July, US housing starts reached a five-month peak, primarily driven by multi-family unit construction. Nevertheless, newly issued housing permits plummeted to a five-year low, signaling that the forecast for residential construction remains grim.

Despite potential pitfalls, markets are climbing with a sense of optimism. Investors appear to be looking beyond risks such as tariffs that could disrupt the current bullish trajectory. An analysis of several ETFs tracking global risk appetite as of August 18 indicates that the overall sentiment remains strongly positive.

Sentiment among US home builders fell in August, hitting its lowest point since 2022, according to the latest survey from the National Association of Home Builders (NAHB). “Affordability remains the primary challenge in the housing sector, and potential buyers are holding off until mortgage rates decrease,” remarked NAHB Chairman Buddy Hughes.

As the Federal Reserve prepares for its annual conference in Jackson, Wyoming on August 21, discussions surrounding inflation are expected to take center stage. Although the latest price metrics show mixed results, several indicators raise concerns about whether cutting interest rates at next month’s policy meeting is the right move, despite being the prevailing sentiment recently.

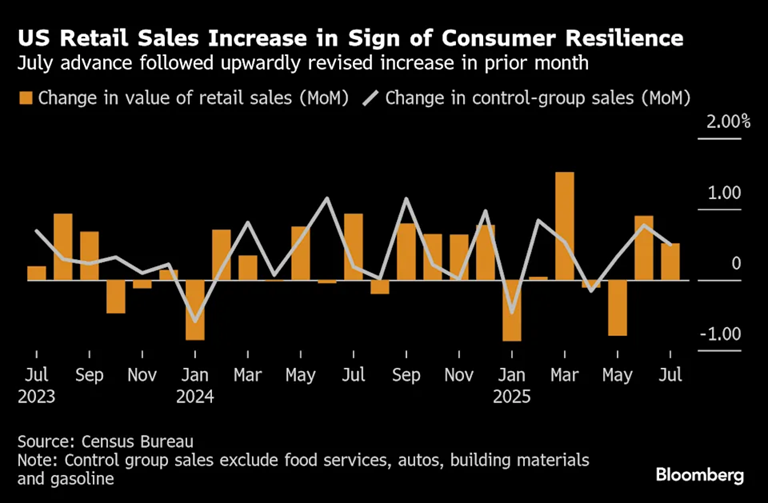

US retail sales increased for the second consecutive month in July, showcasing consumer strength. This uptick alleviated fears that consumer spending might be at risk due to inflation sparked by tariffs. “As long as consumer spending remains robust, companies will continue to retain workers, which could keep driving corporate profits and stock prices higher,” stated Chris Zaccarelli, Chief Investment Officer at Northlight Asset Management, in a recent commentary.

● The Price of Money: A Guide to the Past, Present, and Future of the Natural Rate of Interest

● The Price of Money: A Guide to the Past, Present, and Future of the Natural Rate of Interest

Edited by Jamie Rush, et al.

Summary via publisher (Oxford U. Press)

This accessible guide explores the natural rate of interest—why it is on the rise and its implications for the global economy and financial markets. While many assume that central banks dictate interest rates, the reality is that decisions made by the Federal Reserve, European Central Bank, and other institutions are largely influenced by the natural rate. This rate balances the supply of savings against investment demand, maintaining low inflation and high employment. Recognizing its growing importance can reshape our understanding of monetary policy and economic dynamics.

Partisan Bias in Professional Macroeconomic Forecasts

Benjamin S. Kay (Federal Reserve), et al.

June 2025

This research utilizes a novel dataset linking forecasters from the Wall Street Journal Economic Forecasting Survey to their political affiliations, revealing a partisan bias in GDP growth predictions. Forecasts made by Republican-affiliated analysts tend to project growth rates that are 0.3-0.4 percentage points higher when Republicans occupy the presidency, compared to their Democratic counterparts. Interestingly, Republican forecasters also exhibit lower accuracy under Republican presidents, suggesting that political optimism can skew predictive performance. This pattern appears specific to GDP forecasts and does not extend to metrics like inflation or interest rates. The research posits that differing political views significantly influence growth projections, particularly given the uncertainty associated with GDP data.

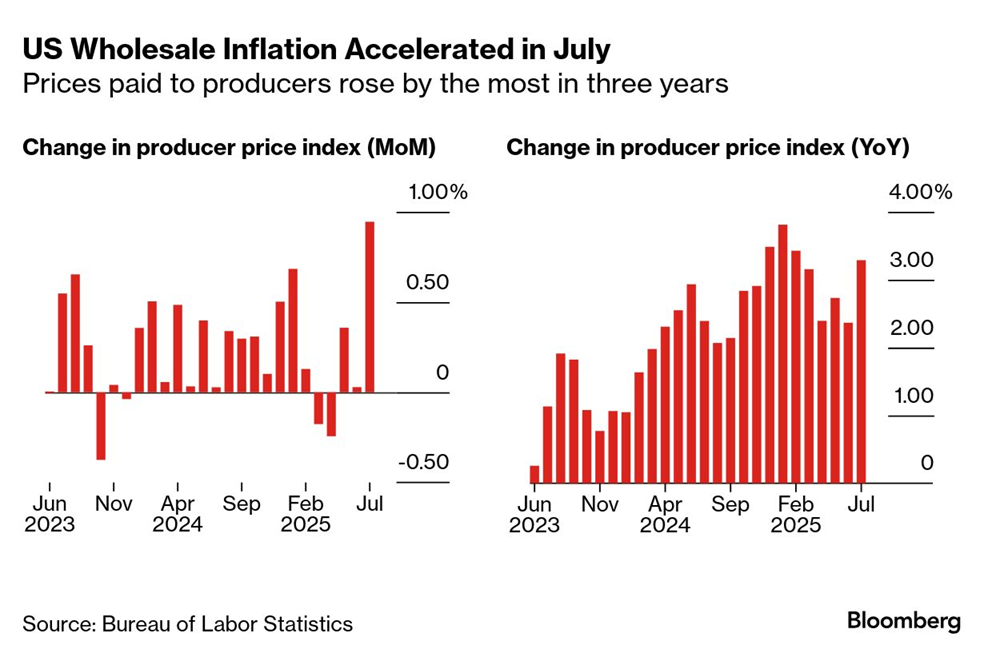

US wholesale inflation accelerated in July, marking the sharpest increase in three years. This surge indicates that producers are facing rising costs faster than consumers. The takeaway? Importers appear to be absorbing the cost of tariffs at present, rather than passing them on to their customers. “It’s only a matter of time before these increased tariffs translate into higher consumer prices,” noted Christopher Rupkey, chief economist at fwdbonds.

This year’s momentum factor remains strong. Throughout 2025, this risk factor has consistently outpaced the broader stock market based on a variety of ETFs leading up to August 13. The recent resurgence in high-beta stocks has further propelled this factor, making it one of the top performers this year.

In summary, while the trends in the residential property market and the broader economy show flickers of positivity, significant uncertainties remain. As we continue to monitor key indicators such as housing starts, builder sentiment, and inflation, it is crucial to maintain vigilance in navigating this evolving landscape.